Blog

Commercial Property Sale Guide for Investors and Owners

TL;DR:

- Selling commercial property is more complex than residential transactions due to longer timelines and documentation challenges. Proper preparation of key documents, choosing the appropriate sale route, and proactive due diligence can significantly accelerate closing and protect asset value. Transparency and thorough organization help sellers negotiate from a position of strength and reduce delays during the closing process.

Selling commercial property carries a level of complexity that residential transactions rarely match. Timelines stretch, documentation gaps surface at the worst moments, and misaligned sale strategies can erode asset value before a buyer even submits an offer. This commercial property sale guide exists to address that reality directly. It covers the preparatory work sellers frequently skip, the sale route decisions that determine both speed and price, the due diligence demands buyers will place on your asset, and the closing-stage pitfalls that stall or kill transactions. Follow this process with discipline and you will enter every negotiation from a position of strength.

Table of Contents

- Key Takeaways

- Prerequisites before listing commercial property

- Choosing the right sale route

- Navigating the closing process

- Due diligence: what buyers verify and how to prepare

- Perspective: what most sellers get wrong

- How Maascompanies supports your commercial property sale

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Document preparation is non-negotiable | Assembling complete lease files, rent rolls, and title reports before listing prevents costly delays later. |

| Sale route shapes your outcome | Auctions accelerate timelines while private treaty and off-market options prioritize price flexibility or confidentiality. |

| Due diligence readiness builds buyer confidence | Accurate financial statements and verified estoppel certificates reduce renegotiations and protect final pricing. |

| Most closing delays are avoidable | Approximately 70% of delays occur after week three, driven by financing and title issues that sellers can anticipate. |

| Seller transparency shortens timelines | Proactive document delivery and clear tenant communication keep buyers confident and forward momentum intact. |

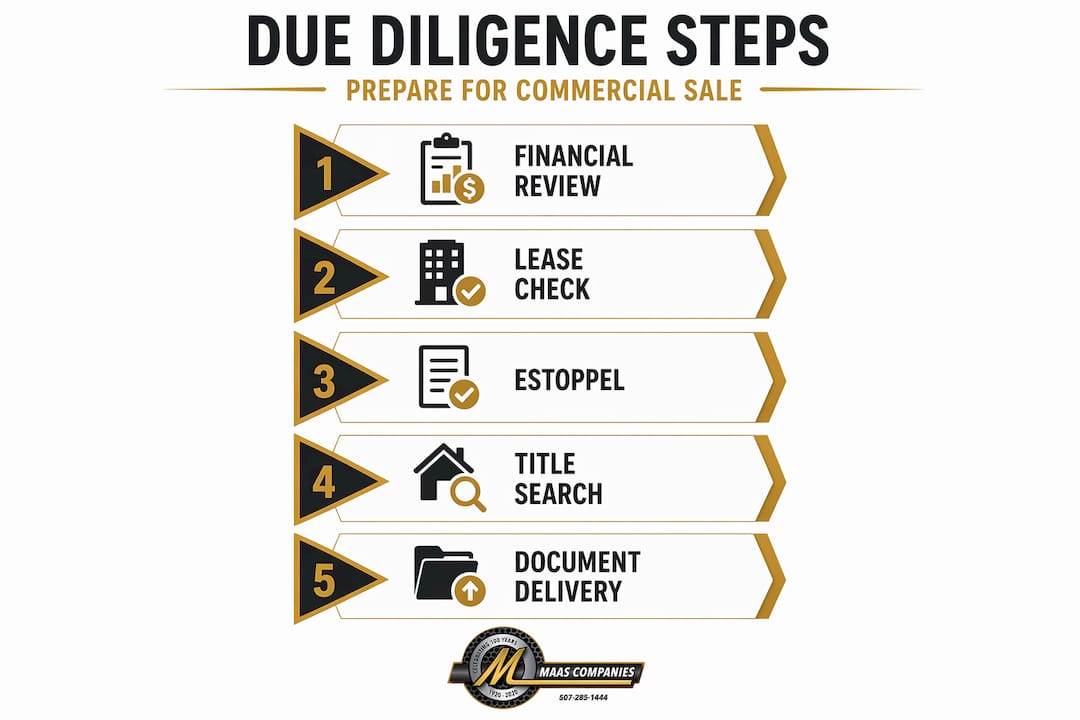

Prerequisites before listing commercial property

Before you place any asset on the market, the documentation supporting that asset must be complete, verified, and organized for buyer review. This is where most commercial sellers lose time and negotiating leverage. Buyers and their lenders will scrutinize every record, and gaps discovered mid-process invite renegotiations or outright withdrawal.

The following documents represent the minimum standard a prepared seller should assemble before listing:

- Rent roll updated within 30 days of the letter of intent. Key due diligence documentation includes executed leases with all amendments, tenant estoppel certificates, guaranties, and security deposit records. A stale rent roll signals disorganization to sophisticated buyers.

- Building condition disclosure and capital expenditure history. Document all material repairs, roof replacements, HVAC servicing, and deferred maintenance items. Buyers will commission their own condition reports, and unexplained discrepancies between your records and their findings create leverage for price reductions.

- Title report with lien resolution completed. Order the title report early. Mechanic’s liens, judgment liens, or ownership disputes take time to clear, and discovering them after a purchase agreement is signed delays closing and erodes buyer confidence.

- Environmental and zoning reports. For industrial or mixed-use properties, Phase I environmental site assessments and zoning compliance confirmations can be ordered proactively. Buyers will request them regardless. Having them ready demonstrates control of the asset.

- Tenant estoppel certificates. These tenant-signed statements confirm lease facts including rent status, defaults, and documentation completeness. Inaccurate estoppel certificates can cause post-close disputes and delay financing. Sellers must verify each estoppel against the actual executed lease file before circulating it.

A good preparation checklist for property sales will track each document by status so nothing reaches a buyer as an open item.

Pro Tip: Do not wait for an LOI to begin estoppel collection. Tenant response times are unpredictable, and missing amendments in lease files are a frequent source of legal exposure. Start the process at least 60 days before you expect a letter of intent.

Choosing the right sale route

No single sale method serves every commercial asset or seller situation. The decision between auction, private treaty, and off-market sale directly affects your timeline, final price, buyer pool, and confidentiality posture. Sale route selection impacts speed, price certainty, and buyer competition in distinct ways, and most transactions take six to twelve weeks from listing to close depending on the method chosen.

| Sale Method | Timeline | Price Certainty | Buyer Competition | Best Suited For |

|---|---|---|---|---|

| Auction | 4 to 6 weeks | High at hammer | Maximum | Distressed assets, plant closures, time-sensitive dispositions |

| Private Treaty | 8 to 16 weeks | Negotiable | Moderate | Stabilized income properties, complex lease structures |

| Off-Market | Variable | Variable | Low to targeted | Confidential transactions, known buyer pools, sensitive tenancies |

Auctions create transparent, competitive bidding conditions that accelerate commercial sales and remove the prolonged back-and-forth of private negotiation. They work best when the seller prioritizes speed and when the asset has broad appeal to multiple buyer types. Manufacturing facilities, industrial plants, and properties associated with business wind-downs are strong candidates for auction disposition.

Private treaty sales offer more negotiation flexibility and allow sellers to manage the pace of buyer interaction. This method suits income-producing properties where lease complexity or tenant relationships require careful handling during the sale process. The tradeoff is time. Private treaty sales can extend considerably if buyer financing falls through or negotiations stall.

Off-market transactions preserve confidentiality and allow sellers to approach targeted buyers directly. This approach is useful when public exposure of the sale could unsettle tenants, employees, or business partners. However, a narrower buyer pool often means reduced price competition, which is a meaningful concession.

For sellers weighing these routes against operational context, reviewing auction versus brokerage comparisons for industrial assets provides useful framework for the decision.

Navigating the closing process

Understanding the closing timeline gives sellers the ability to anticipate problems rather than react to them. Commercial sale closing timelines average 30 to 45 days, broken across four distinct phases of activity.

- Week one: Contract execution and deposit collection. The purchase agreement is signed, earnest money is deposited, and the formal due diligence period begins. This is when the seller’s document preparation determines everything that follows. Organized sellers move immediately to delivering the full document package.

- Week two: Active due diligence review. Buyers review financial records, leases, environmental reports, and physical condition. Their lender begins ordering appraisals and updated title work. Seller responsiveness to information requests during this phase directly affects buyer confidence.

- Weeks three and four: Title clearance and financing confirmation. The lender issues a loan commitment or requests additional conditions. Title issues identified in the preliminary report must be resolved. This is where approximately 70% of closing delays originate, primarily from financing conditions and outstanding title matters.

- Final days: Closing coordination. Deed preparation, wire instructions, prorations calculation, and tenant notification occur. Sellers must coordinate move-out logistics for vacating tenants and transfer of security deposits.

Common delay sources include lender requests for updated income documentation, title exceptions requiring legal resolution, and late delivery of seller-side documents. Sellers who prepare complete documentation upfront and maintain steady communication with the buyer’s team dramatically reduce exposure to these delays.

Pro Tip: Align your purchase agreement so the formal due diligence period does not start until you have delivered all required documents to the buyer. Incorporating due diligence deliverables into the agreement eliminates the leverage imbalance that occurs when buyers hold a running clock while sellers scramble to assemble records.

Tenant communications require particular attention near closing. Tenants have legal rights regarding notice of ownership transfer, security deposit handling, and lease assignment. Failing to manage these communications proactively creates disputes that can delay recording or trigger post-close litigation.

Consult your liquidation timeline planning resources when building the seller-side closing calendar, particularly for properties with operational tenant activity that must be sequenced carefully.

Due diligence: what buyers verify and how to prepare

Due diligence is the period during which buyers verify that the property they agreed to purchase matches what was represented. Sellers who have assembled thorough records treat this phase as a formality. Sellers who have not treat it as a crisis.

The table below outlines the core categories buyers examine and what sellers should prepare in each area.

| Due Diligence Category | Buyer Verification Focus | Seller Preparation Action |

|---|---|---|

| Financial records | T-12 operating statements, rent roll vs. bank deposits | Reconcile all income records; resolve discrepancies before listing |

| Lease documentation | Executed leases, amendments, guaranties, security deposits | Compile full executed lease files with amendment index |

| Estoppel certificates | Tenant confirmation of rent, defaults, lease completeness | Collect and verify estoppels against lease files in advance |

| Physical condition | Environmental site assessments, capital expenditure history | Order Phase I ESA; document all major repairs and deferred items |

| Legal and zoning | Permits, certificates of occupancy, zoning compliance | Confirm current use compliance; resolve any open permit issues |

Buyers perform comprehensive financial due diligence that includes trailing twelve-month operating statements, aging accounts receivable reports, and direct verification of rent rolls against bank deposit records. Discrepancies between stated rents and actual deposits trigger immediate buyer concern and frequently lead to price reduction requests. Sellers must reconcile these records before exposing them.

The estoppel process deserves special attention. Tenant estoppel certificates act as a financial truth check for buyers, confirming lease validity and outstanding claims. The primary risk is signing an estoppel without verifying its contents against the actual lease file. This can bind both tenant and seller to inaccurate lease conditions, generating post-close conflicts that are expensive to resolve.

For sellers managing assets with complex lease structures, working with advisors experienced in industrial asset liquidation provides a framework for sequencing the due diligence package delivery in a way that protects the seller while satisfying buyer requirements efficiently.

Perspective: what most sellers get wrong

I have reviewed enough commercial property transactions to identify a consistent pattern. Sellers who struggle do not struggle because of market conditions or buyer behavior. They struggle because they treat documentation preparation as a response to buyer requests rather than a prerequisite for the entire process.

The estoppel issue is the clearest example I can point to. In my experience, sellers frequently circulate estoppels without cross-referencing them against the lease file. A tenant signs confirming a base rent figure that does not account for a rent abatement in a three-year-old amendment. The buyer’s attorney finds it. Now the seller is in a renegotiation they did not anticipate, with a buyer who has lost confidence in the accuracy of everything else they were told.

Transparency does not just protect sellers legally. It speeds up closings. Buyers who feel they are getting complete, accurate information move faster and negotiate less aggressively. Buyers who sense gaps or inconsistencies slow down, ask more questions, and seek price concessions as insurance against undisclosed risk.

My recommendation is to approach the sale route decision the same way. Do not default to private treaty because it feels more controlled. Examine whether the asset and your timeline actually benefit from the buyer competition and price certainty that an auction structure provides. In many industrial and commercial dispositions, the auction route outperforms private treaty on both price and timeline when the asset is properly prepared and marketed to the right buyer pool.

— Vector

How Maascompanies supports your commercial property sale

Maascompanies brings decades of experience marketing industrial plants, commercial real estate, and complex asset portfolios to qualified buyer pools worldwide. Whether your situation calls for an accelerated auction, a negotiated private sale, or a structured off-market disposition, Maascompanies designs the sale process around your asset type, timeline, and recovery objectives.

Current projects illustrate the scope of that capability. The 3-MGY Biodiesel Plant auction encompasses oilseed processing facilities, a grain handling facility, a manufacturing and warehouse building, and retail fuel stations, all managed through a single coordinated disposition. For sellers seeking alternatives to auction timelines, the Clayton Industries negotiated sale demonstrates the firm’s capacity to execute orderly, negotiated transactions for specialized assets.

Connect with the Maascompanies team through the seller services page to discuss sale route options, documentation requirements, and marketing strategy tailored to your commercial property.

FAQ

What documents should I prepare before listing commercial property?

Sellers should assemble an updated rent roll, all executed leases with amendments, tenant estoppel certificates, a current title report, and environmental or zoning reports relevant to the property type. Completing this package before listing prevents delays during buyer due diligence.

How long does a commercial property sale typically take to close?

Commercial sale closings average 30 to 45 days from contract execution, though the full transaction from listing to closing typically spans six to twelve weeks depending on the sale method selected.

When is an auction preferable to a private treaty sale?

Auctions favor sellers with time-sensitive dispositions, distressed assets, or properties that benefit from open buyer competition. Private treaty is better suited to stabilized income properties with complex lease structures that require negotiation flexibility.

What are the most common causes of closing delays?

Most delays originate from buyer financing conditions and title issues, with approximately 70% occurring after week three of the closing period. Sellers reduce exposure by delivering complete documentation early and maintaining consistent communication with the buyer’s team.

What is a tenant estoppel certificate and why does it matter?

A tenant estoppel certificate is a tenant-signed statement confirming lease facts including current rent, defaults, and documentation completeness. Inaccurate estoppel certificates can delay financing and generate post-close disputes, so sellers must verify each certificate against the actual executed lease file before delivery.

Recommended

- How to Navigate Commercial Property Foreclosure Sales | Blog | Insights on Asset Liquidation and Auction Trends

- Commercial Real Estate Auctions Speed Up Sales | Blog | Insights on Asset Liquidation and Auction Trends

- Pre-Auction Selling Checklist for Industrial Equipment | Blog | Insights on Asset Liquidation and Auction Trends

- Common Commercial Foreclosure Auction Questions for Lenders | Blog | Insights on Asset Liquidation and Auction Trends