Blog

Role of Brokers in Auctions: A Guide for Investors

TL;DR:

- Auction brokers are licensed intermediaries who facilitate restricted auction access, execute bids, and manage transactions from valuation to settlement. They ensure legal compliance, provide disciplined bid execution, and handle process coordination, especially in complex or regulated sales. Proper broker selection, licensing verification, and understanding agency relationships are critical for successful asset liquidation or acquisition outcomes.

Auction brokers are licensed intermediaries who enable buyers to participate in restricted auctions, execute bids with professional discipline, and manage the full transaction lifecycle from asset valuation through settlement. The role of brokers in auctions extends well beyond simple bid placement. For investment professionals and business leaders managing asset liquidation or acquisition, brokers provide legal access, compliance assurance, and structured process management that directly affects recovery outcomes. Understanding how brokers function across different auction types, and which broker category fits your transaction, is a prerequisite for effective capital deployment in any regulated sale environment.

How do brokers overcome licensing and access barriers in auctions?

Many high-value auction markets restrict direct participation to licensed account holders. Dealer-only vehicle auctions, bankruptcy sale hearings, and certain industrial equipment auctions all require credentials that most corporate buyers and investment professionals do not hold. Brokers provide access to dealer-only inventory by routing bids and completing transactions through their licensed accounts, keeping buyers legally compliant throughout the process.

This compliance function is often underestimated. When brokers bridge licensing restrictions, their value includes routing transactions through licensed accounts and ensuring legal transaction completion, not merely marketing or bidding support. A corporate buyer acquiring surplus manufacturing equipment at a regulated industrial auction faces the same gating problem as a first-time vehicle buyer at a dealer-only sale. Without a licensed broker, neither can participate at all.

International buyers face an additional layer of complexity. Foreign entities acquiring U.S. industrial assets through auction must satisfy domestic licensing, tax identification, and proof-of-funds requirements before a bid is accepted. Experienced brokers in auctions handle this documentation as a standard part of their service, preventing disqualification before the auction opens.

Key access barriers brokers resolve on behalf of buyers include:

- Dealer license requirements at vehicle, equipment, and specialty asset auctions

- Qualified bidder eligibility in bankruptcy and court-supervised sales, including deposits and definitive agreements

- Proof-of-funds documentation required by bid procedures orders before participation is granted

- International buyer compliance covering tax identification, entity verification, and domestic transaction routing

Pro Tip: Confirm your broker holds active licenses in the specific auction jurisdiction before engaging. A broker licensed in one state may not satisfy eligibility requirements for a federally supervised bankruptcy sale in another.

What are the operational roles and responsibilities of brokers during auctions?

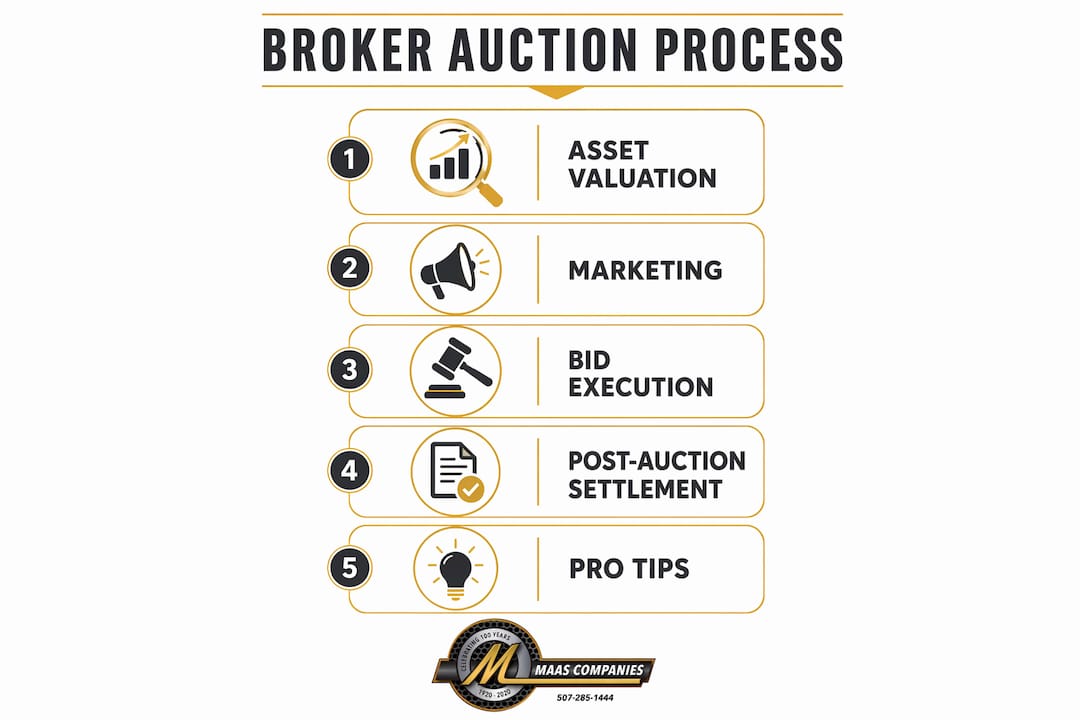

Auction broker responsibilities span the entire transaction, not just the bidding window. The full scope covers four distinct phases: pre-auction preparation, auction-day execution, post-auction settlement, and dispute resolution.

Pre-auction preparation

Before a single bid is placed, brokers conduct or coordinate asset valuation, catalog creation, marketing to qualified buyer pools, and eligibility documentation. Auction houses manage end-to-end processes including valuation, contract agreement, cataloging, marketing, auction execution, and settlement within 30–35 days post-auction. Brokers operating within this framework carry responsibility for accuracy in asset descriptions and for reaching the right buyer audience before the sale date.

Auction-day execution

Bid execution under live auction pressure is where broker involvement produces measurable results. About 25–30% of auction buyers freeze under live bidding pressure. Brokers remove emotional response from the equation and execute bids reliably, improving outcomes for buyers who would otherwise overbid, hesitate, or miss critical bid windows. Buyer agents also capture over 95% of auction signals versus 60–70% for first-time bidders, a gap that directly affects whether a buyer wins at the right price or loses to a more disciplined competitor.

Post-auction settlement

Settlement is where many acquisition teams encounter unexpected friction. The standard settlement process follows this sequence:

- Invoice generation by the auction house to the winning bidder, typically within 24–48 hours of the sale

- Funds collection from the buyer, including buyer’s premium and any applicable taxes or fees

- Commission deduction by the broker from gross proceeds, per the agreed fee structure

- Net proceeds distribution to the seller, completing the transaction cycle

Net proceeds distribution typically occurs 30–35 days post-payment clearance. Acquisition teams must plan insurance, logistics, and capital availability aligned with these settlement flows. Failing to account for this timeline creates working capital gaps that can disrupt post-acquisition operations.

Pro Tip: Build the 30–35 day settlement window into your working capital model before the auction date. Surprises at settlement are almost always a planning failure, not a broker failure.

The table below summarizes typical broker fee structures by auction type:

| Auction type | Typical broker fee structure | Paid by |

|---|---|---|

| Industrial equipment auction | 5–15% buyer’s premium | Buyer |

| Business sale (broker-listed) | 8–12% success fee on sale price | Seller |

| Controlled auction (investment banker) | Monthly retainer plus tiered success fee | Seller |

| Bankruptcy/court-supervised sale | Fixed fee plus percentage of proceeds | Seller or estate |

Business brokers vs. investment bankers: which fits your auction?

The distinction between business brokers and investment bankers in auction contexts is not a matter of prestige. It is a matter of deal size, process structure, and the competitive tension each type can generate.

Business brokers focus on smaller transactions, typically below $5 million in enterprise value. Their primary activities are listing, marketing, and facilitating buyer introductions. They operate sequentially, presenting the asset to one or a few buyers at a time. This approach works for straightforward asset sales but does not generate the competitive dynamics that maximize recovery in complex or high-value transactions.

Investment bankers run controlled auctions with up to 150 vetted buyers, structured timelines, and letter-of-intent deadlines that force buyers to compete simultaneously. This simultaneous competitive pressure is the core economic mechanism that drives prices above bilateral negotiation outcomes. Investment bankers charge monthly retainers plus tiered success fees, reflecting the depth of process management they provide.

The table below clarifies when each broker type is appropriate:

| Criteria | Business broker | Investment banker |

|---|---|---|

| Typical deal size | Below $5 million | $5 million and above |

| Buyer pool size | Small, sequential | 60–150 vetted buyers simultaneously |

| Fee structure | Success fee only | Retainer plus tiered success fee |

| Process structure | Listing and marketing | Controlled auction with LOI deadlines |

| Best for | Single-asset or small business sales | Plant closures, restructurings, complex asset portfolios |

The core economic value of brokers in auctions lies in generating competitive tension by presenting opportunities simultaneously to many vetted buyers under controlled conditions. A business broker listing an asset sequentially cannot replicate this effect. For transactions involving industrial plant closures, multi-site equipment portfolios, or distressed business sales, the investment banker’s controlled auction process is the appropriate structure.

What legal and agency considerations affect broker roles in auctions?

Agency representation in auctions is frequently misunderstood, and the misunderstanding creates real legal and financial risk for buyers. The most common misconception is that paying a buyer’s premium creates an agency relationship between the buyer and the auctioneer or broker. It does not.

Buyer’s premium payment does not equate to broker or auctioneer agency. Representation is governed by contracts, disclosures, and fiduciary duties. Agency depends on who retained the auctioneer or broker, the contractual terms in place, and to whom fiduciary duties are formally owed.

Buyers who assume they are represented because they paid a premium have no contractual protection if a dispute arises. The broker’s fiduciary duty runs to the party who hired them, which in most auction structures is the seller. Buyers who want formal representation must retain their own broker under a separate written agreement.

Key legal considerations for buyers and sellers include:

- Confirm agency in writing before the auction opens. Verbal assurances of representation are not enforceable.

- Review all disclosure documents provided by the auctioneer or broker. Most jurisdictions require written disclosure of agency relationships.

- Identify who retained the broker. If the seller retained the auctioneer, the auctioneer’s fiduciary duty runs to the seller, regardless of who pays the premium.

- Understand dual agency risks. In some transactions, a broker may represent both buyer and seller. This requires explicit written consent from both parties and carries inherent conflict-of-interest risk.

“To avoid legal and fiduciary pitfalls, buyer-side teams must proactively confirm who retains the auctioneer or broker and clarify agency relationships in writing, rather than assuming representation based on fee payment or interactions.” — Mike Brandly, Auctioneer Blog

Pre-auction eligibility gating is a related risk area. Failure in eligibility gating is a common acquisition failure point in court-supervised or regulated auctions. Brokers who specialize in bankruptcy and restructuring sales manage deposit submissions, proof-of-funds packages, and qualified bidder documentation as standard deliverables, protecting their clients from disqualification before the sale hearing begins.

Key Takeaways

Brokers in auctions deliver their greatest value when they combine licensing compliance, disciplined bid execution, and structured process management across the full transaction lifecycle.

| Point | Details |

|---|---|

| Licensing and access | Brokers provide legal entry to dealer-only and regulated auctions that buyers cannot access directly. |

| Bid execution discipline | Brokers capture over 95% of auction signals, compared to 60–70% for first-time bidders, improving outcomes. |

| Settlement planning | Net proceeds distribution takes 30–35 days post-payment; build this into working capital planning. |

| Broker type selection | Use investment bankers for complex or high-value transactions; business brokers for smaller, straightforward sales. |

| Agency confirmation | Paying a buyer’s premium does not create representation; confirm agency relationships in writing before bidding. |

Why broker selection is the decision most acquisition teams get wrong

My experience working across industrial plant closures, equipment liquidations, and multi-site asset sales consistently points to the same failure pattern. Acquisition teams spend significant time evaluating assets and almost no time evaluating the broker managing the auction. They assume all licensed brokers deliver equivalent process quality. They do not.

The brokers who consistently produce better recovery outcomes share three characteristics. First, they hold active licenses in the specific jurisdictions where the auction will occur, not just general credentials. Second, they have a documented compliance track record in the auction type involved, whether that is a bankruptcy sale, a regulated equipment auction, or a controlled business sale. Third, they provide written agency disclosures before any engagement begins, not after questions arise.

I have seen transactions where a seller engaged a broker with strong marketing reach but no experience managing the eligibility gating requirements of a court-supervised sale. The result was a delayed auction, a reduced buyer pool, and a materially lower recovery than the asset warranted. Marketing reach matters. Compliance expertise matters more.

For buyers, the lesson is equally direct. Confirm your representation in writing before the auction opens. Review the broker’s fee structure and understand exactly what triggers their commission. And factor the 30–35 day settlement timeline into your post-acquisition logistics plan from day one. These are not administrative details. They are the variables that determine whether a transaction closes cleanly or generates months of follow-on friction.

— Vector

How Maascompanies supports complex auction and brokerage transactions

Maascompanies brings decades of experience managing industrial plant auctions, equipment liquidations, and commercial property sales for clients who need structured, compliant, and results-oriented auction execution. From initial asset valuation and catalog development through aggressive multi-channel marketing and final settlement, Maascompanies manages the full process with the precision that complex asset transactions require.

Whether you are managing a plant closure, restructuring surplus inventory, or acquiring industrial assets through a regulated sale, Maascompanies provides the licensing, buyer network, and process discipline to maximize recovery. Review the current biodiesel plant auction to see how Maascompanies structures large-scale industrial auction projects, or visit the seller services page to discuss your asset recovery objectives directly.

FAQ

What is the primary role of a broker in an auction?

A broker in an auction acts as a licensed intermediary who enables buyer access to restricted markets, executes bids on behalf of clients, and manages the transaction from eligibility documentation through post-auction settlement.

Does paying a buyer’s premium mean the broker represents the buyer?

No. Buyer’s premium payment does not create agency. Representation is determined by who retained the broker and the terms of the written contract, not by who pays the premium.

How long does auction settlement typically take?

Settlement and net proceeds distribution typically occur within 30–35 days post-payment clearance. Buyers and sellers should build this timeline into working capital and logistics planning.

When should I use an investment banker instead of a business broker?

Use an investment banker for transactions above $5 million or involving complex asset portfolios, plant closures, or restructurings. Investment bankers run controlled auctions across 60–150 buyers, generating competitive tension that business brokers cannot replicate through sequential marketing.

How do brokers help buyers in bankruptcy or court-supervised auctions?

Brokers manage the full eligibility gating process, including deposit submissions, proof-of-funds packages, and qualified bidder documentation. Failure in eligibility gating is a leading cause of disqualification in regulated sales, and experienced brokers prevent it by completing requirements well before the sale hearing date.

Recommended

- Auction absentee bidding: strategies for industrial equipment | Blog | Insights on Asset Liquidation and Auction Trends

- How to Navigate Commercial Property Foreclosure Sales | Blog | Insights on Asset Liquidation and Auction Trends

- Commercial Real Estate Auctions Speed Up Sales | Blog | Insights on Asset Liquidation and Auction Trends

- Top reasons to buy at auction: maximize value & cut risk | Blog | Insights on Asset Liquidation and Auction Trends