Blog

Equipment Liquidation Workflow: Maximize Asset Recovery

TL;DR:

- Structured liquidation workflows significantly increase asset recovery rates compared to forced sales.

- Proper preparation, including asset inventory and valuation, is essential before executing a sale.

- Engaging experienced liquidation partners ensures efficient process management and maximizes value.

When a distressed industrial asset hits your balance sheet, every day without a structured plan costs real money. Carrying costs accumulate, buyer interest fades, and the window for maximum recovery narrows fast. Auctions recover 30-65% of FMV for property, plant, and equipment in bankruptcy situations, while forced sales average far less. For private equity professionals and corporate decision-makers managing plant closures, carve-outs, or divestitures, an orderly equipment liquidation workflow is not a procedural formality. It is the single greatest lever you can pull to protect and maximize asset recovery value.

Table of Contents

- Understanding equipment liquidation in distressed scenarios

- Preparing for equipment liquidation: What you need to get started

- Step-by-step equipment liquidation workflow

- Common mistakes and verification: Keeping liquidation on track

- Why most equipment liquidation workflows miss value — and what really works

- Leverage expert liquidation partners for optimal outcomes

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Orderly workflow maximizes value | Structured liquidation processes consistently recover more asset value than forced sales. |

| Preparation prevents pitfalls | Thorough inventory and documentation prep are essential for compliant, effective liquidation. |

| Step-by-step execution matters | Following a defined workflow with clear checks and controls leads to better outcomes and fewer risks. |

| Expert partnerships add value | Working with specialized liquidation advisors can further increase recovery rates and process confidence. |

Understanding equipment liquidation in distressed scenarios

Equipment liquidation, at its core, is the structured process of converting physical industrial assets into cash. But the method used determines how much cash you actually recover. Three terms anchor every serious conversation about distressed assets:

- Property, plant, and equipment (PPE): The physical industrial assets on a company’s balance sheet, from CNC machinery to processing lines and facility infrastructure.

- Fair market value (FMV): The price a willing buyer pays a willing seller, both with reasonable knowledge of the facts and neither under compulsion.

- Orderly vs. forced liquidation: Orderly liquidation allows adequate time to find qualified buyers and optimize pricing. Forced liquidation compresses timelines and gives sellers little negotiating power.

For private equity firms executing carve-outs, divestitures, or operational turnarounds, the stakes around these definitions are significant. A facility undergoing a plant-level wind-down is not just a logistics problem. It is a recovery event with material impact on fund returns. Liquidation sales strategies that are well-planned consistently outperform reactive approaches across every measurable metric.

“Orderly liquidation processes allow sellers to engage the broadest possible buyer pool, which is the most reliable path to higher recovery rates compared to compressed, forced-sale timelines.”

Data supports this clearly. Recovery rates for non-financial firms average just 35% of FMV for PPE in bankruptcy proceedings. That figure rises considerably when workflow quality improves. The difference between 35% and 60% recovery on a $10 million equipment portfolio is $2.5 million. That number makes workflow quality a financial priority, not an operational afterthought.

A structured workflow delivers four concrete benefits:

- Speed with control: Defined timelines prevent drift while ensuring no phase is rushed.

- Transparency: Buyers trust processes with clear documentation, which drives competitive bidding.

- Compliance: Environmental, legal, and union requirements are addressed systematically, not reactively.

- Accountability: Each stakeholder knows their role, reducing coordination failures.

Leaders reviewing plant liquidation in 2026 are finding that disciplined workflow design is the single most consistent predictor of recovery performance.

Preparing for equipment liquidation: What you need to get started

Preparation is where most value is either protected or lost. Before a single asset is listed or a buyer is contacted, your team needs to complete a thorough readiness review. PE firms focused on carve-outs and divestitures of non-core industrial assets consistently find that preparation quality directly determines final recovery outcomes.

Here is a structured preparation checklist organized by priority:

- Complete asset inventory: Catalog every piece of equipment with serial numbers, age, condition ratings, and maintenance history. Gaps in inventory lead to missed assets and lower buyer confidence.

- Commission independent appraisals: Establish FMV and orderly liquidation value (OLV) baselines before any sale discussions begin.

- Conduct stakeholder alignment: Engage legal counsel, environmental health and safety (EHS) officers, union representatives if applicable, and lenders holding security interests.

- Gather title and compliance documentation: Confirm clear title, resolve any liens, and compile environmental permits, inspection records, and decommissioning requirements.

- Engage third-party specialists: Bring in qualified appraisers, auction firms, or expert asset review professionals early to support accurate valuation and buyer outreach.

| Preparation area | Key deliverable | Responsible party |

|---|---|---|

| Asset inventory | Itemized equipment catalog | Operations/PE advisor |

| Valuation | Certified appraisal report | Independent appraiser |

| Legal/lien review | Clear title confirmation | Legal counsel |

| EHS compliance | Environmental clearance memo | EHS officer |

| Sale structure | Method recommendation | Liquidation specialist |

Pro Tip: Do not wait for legal closure or formal board approval before starting the inventory. Parallel workstreams in preparation cut weeks off your overall timeline without adding risk.

Common preparation pitfalls include treating the asset list as static when equipment is often moved or cannibalized during wind-down, and failing to account for removal costs in the net recovery calculation. Facility transition strategies that factor in rigging, loading, and freight significantly reduce unwelcome surprises at closing.

Step-by-step equipment liquidation workflow

With preparation complete, execution follows a defined sequence. Each phase has clear responsibilities, decision points, and warning flags that signal when to pause and reassess.

- Asset review and valuation (Days 1-10): Finalize the inventory, confirm appraisals, and establish the reserve or minimum acceptable price for each lot. Decision check: Does the OLV support the sale, or should select assets be redeployed internally?

- Marketing and buyer outreach (Days 10-30): Launch targeted outreach to qualified industrial buyers, auction registrants, and trade networks. The breadth of this phase directly affects competitive bidding outcomes.

- Sale execution (Days 30-60): Conduct the auction, negotiated sale, or bulk buyout based on asset type and timeline constraints. Auctions for asset disposition work best for high-volume, commodity-type equipment. Negotiated sales suit specialized or high-value machinery with a narrower buyer pool.

- Asset removal and transfer (Days 60-90): Coordinate buyer-contracted riggers, confirm load-out schedules, and document chain-of-control transfers. Shipping workflow efficiency practices borrowed from logistics management can meaningfully reduce removal bottlenecks.

- Financial and compliance close (Days 85-90): Reconcile proceeds, release liens, submit environmental clearances, and distribute recovery funds per the waterfall agreement.

| Sale method | Best for | Recovery potential | Timeline |

|---|---|---|---|

| Live/online auction | High-volume, general equipment | Moderate to high | 30-45 days |

| Negotiated sale | Specialty or high-value assets | High | 45-90 days |

| Bulk buyout | Speed priority, mixed assets | Lower | 15-30 days |

An orderly process boosts recovery rates and avoids the significant pitfalls of forced sales, including compressed buyer pools and inadequate due diligence time. PE firms frequently use hybrid structures, running auctions for production equipment while pursuing negotiated deals for proprietary systems in parallel.

Pro Tip: Set a formal go/no-go decision gate at the end of the marketing phase. If qualified buyer interest falls below a defined threshold, pivot to a bulk sale rather than running a poorly attended auction that anchors a low public price.

For a detailed breakdown of equipment liquidation steps by phase, including CFO-focused financial controls, additional resources are available that cover each stage in more granular detail.

Common mistakes and verification: Keeping liquidation on track

Even experienced teams encounter workflow failures. Understanding the most frequent mistakes and building verification steps into every transition point is what separates high-recovery events from costly ones.

Most frequent workflow mistakes include:

- Rushing the marketing phase to meet an artificial deadline, which compresses the buyer pool and reduces competitive pressure on pricing.

- Failing to document asset condition at the time of sale, creating disputes during removal.

- Overlooking environmental obligations tied to specific equipment, which can halt removal and trigger regulatory penalties.

- Allowing a double-sale error when inventory control is not centralized, particularly in multi-site wind-downs.

- Neglecting to notify secured lenders before executing sales, which can void transactions or create legal liability.

“Operational improvements made prior to exit, including thorough documentation and compliance clearance, are among the most reliable ways PE firms protect and enhance divestiture value.”

Operational improvements prior to exit directly maximize value for PE divestitures, and the same principle applies to equipment liquidation. A well-documented, clean asset is worth more to a buyer than an identical asset with missing records.

Verification checklist for closing a liquidation event:

- All sold assets physically removed and departure confirmed in writing

- Chain-of-control documentation signed by buyer and seller representatives

- Environmental clearances filed with relevant agencies

- Lien releases obtained and recorded

- Final proceeds reconciliation completed and reviewed by legal counsel

- Facility restored to agreed handover condition

For organizations managing plant liquidation for lenders or special asset managers, these verification steps are not optional. They represent the formal close of the recovery event and protect all parties from post-close disputes. The commercial relocation process offers useful parallel frameworks for managing physical asset transfer logistics in complex multi-party situations.

A successful liquidation looks like this: proceeds distributed within agreed timelines, no post-close buyer disputes, full environmental sign-off, and a final recovery rate at or above the OLV established at the outset.

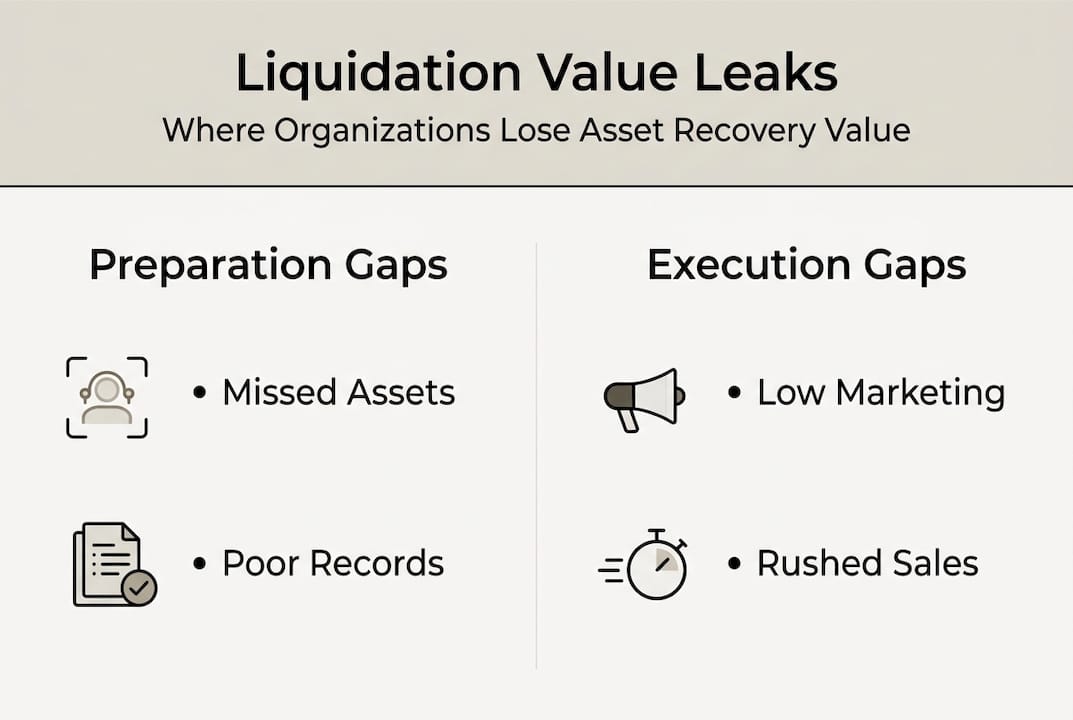

Why most equipment liquidation workflows miss value — and what really works

Here is a reality that most guides avoid: following a checklist is necessary but not sufficient. The organizations that consistently achieve top-tier recovery rates do something different from those that simply execute a process.

The most common value leak is not in execution. It is in the gap between preparation and marketing. Teams spend weeks getting the inventory right, then hand off to a single sales channel and wait. Sophisticated PE sponsors and their portfolio company operators pursue maximizing recovery in 2026 by investing in pre-liquidation operational clean-up: repairing, cleaning, and organizing equipment before buyer site visits. The visual and mechanical condition of assets at first impression drives bid confidence more than any appraisal report.

Organizational silos also cost money. When legal, operations, and finance run separate tracks without a single point of coordination, decisions that should take two days take two weeks. Specialized advisors with cross-functional experience eliminate that drag. Resistance to outside experts is where even experienced corporate teams leave value on the table. Internal teams know the assets; external specialists know the buyers.

Leverage expert liquidation partners for optimal outcomes

Putting a proven workflow into practice requires both the right process and the right partners. Maas Companies brings decades of international experience helping PE firms and corporate operators achieve maximum recovery on industrial equipment and facility assets.

From industrial equipment selling services to full-scale plant wind-downs, our team manages every phase of the liquidation workflow, from inventory and valuation through marketing, sale execution, and compliance close. Our specialized service offerings are designed for exactly the kinds of complex, time-sensitive asset events that PE professionals and corporate decision-makers face. See how we delivered results in a real-world example with our orderly negotiated sale at Clayton Industries. Contact Maas Companies to discuss your next asset event and put a structured recovery plan in place.

Frequently asked questions

How long does an equipment liquidation workflow typically take?

Most industrial equipment liquidations span 30-90 days depending on asset volume, condition, and the sale method selected. Orderly processes are faster and more efficient in recovery compared to reactive or forced approaches that often create downstream delays.

What is the average value recovery in a forced liquidation versus an orderly process?

Forced liquidations average just 35% of FMV for PPE in non-financial firm bankruptcies, while orderly sales with structured workflows routinely achieve significantly higher returns by attracting competitive buyer participation.

Can auctions and negotiated sales be run concurrently in a liquidation?

Yes, hybrid approaches are entirely viable and often deliver better outcomes when asset types vary. Orderly liquidation frameworks are flexible enough to accommodate simultaneous auction and negotiated sale tracks for different asset classes within the same event.

What documentation is needed before starting a liquidation?

A full equipment inventory, certified appraisals, prior title records, lien searches, environmental compliance documentation, and stakeholder authorization are all required before any sale activity should begin.

Recommended

- Equipment liquidation explained: maximizing asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- How Industrial Plant Liquidation Maximizes Recovery Value for Lenders | Blog | Insights on Asset Liquidation and Auction Trends

- Maximize Asset Recovery: Top Real Estate Liquidation Methods | Blog | Insights on Asset Liquidation and Auction Trends

- Asset Lifecycle Management - FullyOps