Blog

Industrial Property Sales Explained for Investors in 2026

TL;DR:

- Industrial property sales involve transferring specialized real estate assets used for manufacturing, logistics, and distribution, with valuation driven by physical specifications known as the spec stack. The market emphasizes physical attributes, lease terms, and buyer profiles, with cap rates indicating asset quality and influencing pricing gaps in 2026. Successful dispositions rely on complete documentation, targeted marketing, appropriate buyer engagement, and leveraging expertise to navigate market complexities.

Industrial property sales are defined as the marketing and transfer of specialized real estate assets used for manufacturing, warehousing, distribution, and logistics operations, requiring technical, financial, and strategic expertise that standard commercial real estate transactions do not demand. Unlike office or retail dispositions, industrial real estate transactions hinge on physical building specifications, institutional underwriting standards, and market dynamics that shift rapidly with supply chain and e-commerce demand. Real estate investors, corporate asset managers, and finance professionals who approach these transactions without understanding the full picture routinely leave capital on the table. This article provides a direct, data-grounded explanation of how industrial property sales work in 2026, from asset valuation to buyer targeting and disposition execution.

What is industrial property sales explained in plain terms?

Industrial property sales, known in institutional circles as industrial real estate disposition or asset liquidation, cover a broad spectrum of property types. These include bulk distribution centers, last-mile fulfillment facilities, flex industrial buildings, cold storage, and heavy manufacturing plants. Each asset type carries distinct valuation drivers, buyer pools, and marketing requirements.

The commercial property market overview for industrial assets in 2026 reflects sustained institutional demand, constrained new supply in key logistics corridors, and pricing sensitivity tied directly to asset quality. Participants in these transactions include real estate investment trusts (REITs), private equity real estate funds, institutional asset managers, regional owner-operators, and developers pursuing redevelopment plays. Understanding which participant is the right buyer for a specific asset is the first strategic decision in any disposition process.

Industrial property is distinguished from other commercial real estate by its functional requirements. Tenants and buyers evaluate loading dock configurations, power capacity, ceiling clearance, and site circulation, not lobby aesthetics or floor plan flexibility. This functional specificity means that a property’s physical specifications often determine its value more directly than its income history.

What physical specifications determine industrial property value?

Industrial underwriting experts prioritize the “spec stack” over traditional income metrics when evaluating industrial assets. The spec stack is the collective set of physical building attributes that define an asset’s utility for modern logistics and manufacturing tenants. Even a well-located property will trade at a discount if its spec stack falls short of institutional thresholds.

The six core elements of the spec stack, and their Class A benchmarks, are:

- Clear height: 32 to 36 feet minimum for bulk distribution; older buildings at 24 to 28 feet face significant tenant universe restrictions.

- Column grid: 54 by 60 feet or larger to allow efficient racking and material handling equipment movement.

- ESFR sprinkler system: Early Suppression Fast Response systems are required by most institutional tenants for high-pile storage.

- Floor load capacity: 8,000 pounds per square foot or greater for heavy manufacturing and logistics operations.

- Trailer parking ratio: One stall per 5,000 to 10,000 square feet of building area, with cross-dock configurations preferred.

- Dock door count and configuration: Matched to tenant throughput requirements, with grade-level doors supplementing dock-high positions for flexibility.

Legacy properties built before 2000 frequently fall below these thresholds on multiple dimensions. A 24-foot clear height building in a strong submarket will still attract buyers, but at a meaningful price discount relative to a 36-foot Class A asset nearby. The spec stack directly determines the tenant universe and, by extension, the valuation multiple an asset can command.

Separately deeded Improved Outdoor Storage (IOS) parcels adjacent to industrial buildings add a distinct valuation layer. These trailer yards and equipment storage lots carry their own cap rate and are increasingly priced as standalone assets by institutional buyers, with blended cap rates reflecting the differentiated value of building and yard components.

Pro Tip: Document every spec element with current measurements and certifications before going to market. Sellers who present incomplete or estimated specs routinely trigger buyer walkaways during due diligence, even when the asset itself is competitive.

How do market dynamics and financial metrics influence industrial sales?

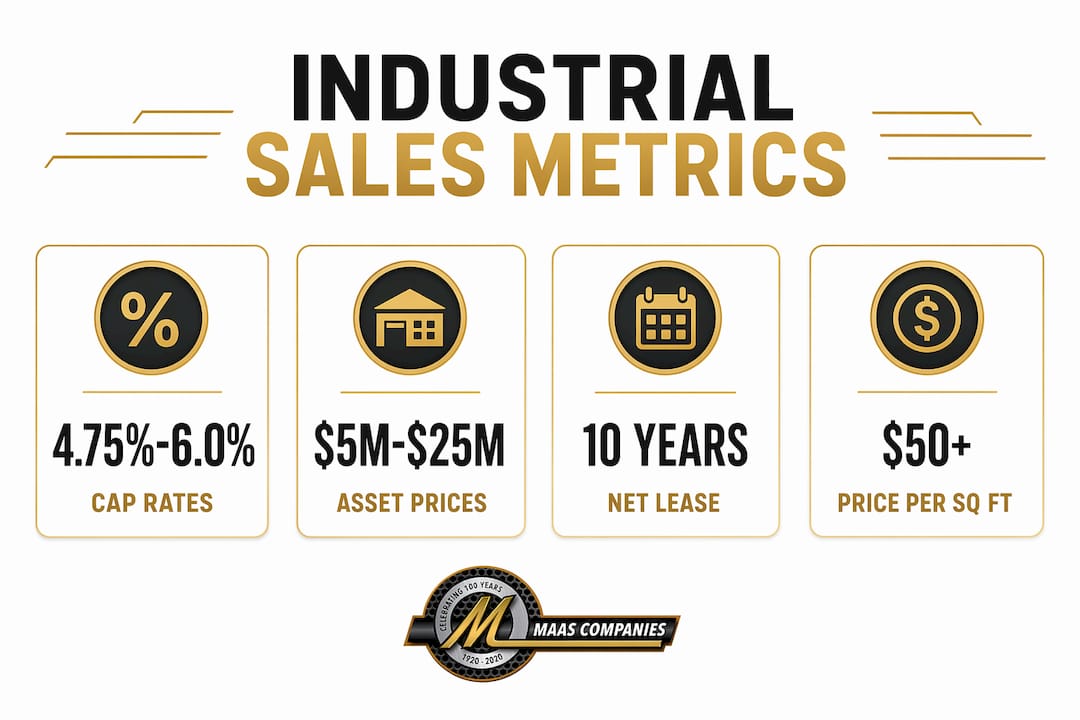

Cap rates are the primary pricing mechanism for income-producing industrial assets, and the spread between asset classes in 2026 is significant. Class A institutional assets trade at cap rates in the high 4s to low 6s, while older secondary properties trade at 6.5% to 8% or higher. This spread translates directly into per-square-foot pricing gaps that can exceed $50 to $80 per square foot between a modern logistics facility and a 1980s-vintage warehouse in the same submarket.

| Asset Class | Typical Cap Rate Range | Pricing Context |

|---|---|---|

| Class A bulk distribution (32 ft+) | 4.75% to 5.75% | Institutional REIT and PE buyer competition |

| Class B regional warehouse (24-28 ft) | 5.75% to 7.00% | Value-add investors and regional operators |

| Legacy industrial (sub-24 ft) | 7.00% to 8.50%+ | Owner-users and redevelopment buyers |

| IOS / trailer yard parcels | 5.50% to 7.50% | Specialty logistics operators and PE funds |

Lease structure and tenant credit quality are equally important for income-producing assets. A 10-year net lease with an investment-grade tenant at below-market rent will trade at a tighter cap rate than a shorter-term lease with a regional operator, even if the building specs are identical. Institutional buyers model lease rollover risk carefully, and residual value assumptions depend on whether the spec stack supports re-leasing at market rates after expiration.

Location relative to transportation infrastructure creates pricing premiums that can be substantial. Price per square foot can exceed $212 per square foot in last-mile distribution corridors compared to averages of $145 per square foot in secondary markets, as demonstrated by Goodman Group’s acquisition of the Anheuser-Busch brewery site. Proximity to port facilities, interstate interchanges, and dense population centers compresses cap rates and expands the buyer pool simultaneously.

Replacement cost is a pricing floor that disciplined buyers reference in every underwriting model. When acquisition cost approaches or exceeds replacement cost, buyers shift their analysis toward income yield and lease term certainty rather than speculative upside.

Who are the buyers in industrial real estate transactions?

The buyer universe for industrial property sales divides into three primary categories, each with distinct valuation priorities and acquisition criteria.

Institutional investors include REITs such as Prologis and EastGroup Properties, private equity real estate funds, and pension fund advisors. These buyers focus on spec stack compliance, lease term, tenant credit, and market liquidity. A 51-property portfolio totaling 8.5 million square feet traded for $1.81 billion in May 2026, with 90% occupancy and an operational platform transfer of 40 employees included in the transaction. This scale of deal is only accessible to institutional capital, and it illustrates how portfolio sales require a different marketing and negotiation approach than single-asset dispositions.

Local and regional owner-operators prioritize immediate functionality over spec perfection. A food manufacturer acquiring a facility for owner-occupancy will accept a 28-foot clear height if the power capacity, dock configuration, and site access meet their operational requirements. These buyers are less sensitive to cap rate pricing and more focused on replacement cost and operational fit.

Developers and value-add investors target assets with redevelopment potential, obsolete specs in high-demand locations, or below-market leases with near-term rollover. Their valuation model centers on land value, entitlement risk, and projected stabilized yield after capital investment.

Pro Tip: Tailor your marketing exposure to the buyer profile that matches your asset’s strengths. A legacy building in a supply-constrained submarket deserves developer outreach, not just institutional broker distribution. Misaligned marketing channels extend timelines and depress pricing.

What are effective strategies for selling industrial property?

Successful industrial property sales require preparation, positioning, and channel selection that align with the asset’s characteristics and the target buyer pool. The following steps define a disciplined disposition process.

-

Compile a complete documentation package. Vacant industrial facilities sell faster and at higher prices when sellers provide objective documentation covering zoning, power capacity, dock configurations, environmental status, and site access. Institutional buyers demand this data early, and gaps trigger delays or buyer exits.

-

Determine the optimal sale condition. Selling vacant, stabilizing with a short-term lease before sale, or marketing with lease-up upside priced into the offering each produce different buyer pools and pricing outcomes. Vacant sales attract owner-users and developers; stabilized assets attract income-focused institutional buyers.

-

Select the right marketing channels. Off-market transactions dominate large portfolio dispositions, protecting tenant confidentiality and managing diligence complexity. Single-asset sales in competitive markets benefit from broad broker distribution and, in some cases, structured auction processes that create competitive tension among qualified buyers.

-

Price from data, not sentiment. Sellers who set prices emotionally rather than from comparable sales, cap rate analysis, and replacement cost benchmarks consistently underperform. Institutional buyers apply math-first valuations and will not negotiate upward from an unsupported ask.

-

Negotiate beyond price. Diligence scope, contingency periods, earnest money structure, and buyer financial qualification are as important as the headline number. A lower offer from a well-capitalized, experienced buyer with a short diligence period often produces a better outcome than a higher offer from an undercapitalized buyer with broad contingencies.

For sellers managing facility liquidation strategies, the disposition of real property and personal property often proceeds in parallel, requiring coordination between real estate brokers, equipment auctioneers, and legal counsel to avoid conflicts in timing and asset classification.

Key takeaways

Industrial property sales succeed when physical specifications, financial metrics, and buyer-specific marketing align with the asset’s actual condition and market position.

| Point | Details |

|---|---|

| Spec stack drives value | Clear height, dock doors, floor load, and ESFR systems determine tenant universe and pricing multiples. |

| Cap rate spread is wide | Class A assets trade at 4.75% to 5.75%; legacy properties trade at 7% to 8.5% or higher in 2026. |

| Buyer type shapes strategy | Institutional, owner-operator, and developer buyers each require different marketing channels and negotiation tactics. |

| Documentation prevents walkaways | Complete physical and financial documentation packages reduce diligence delays and buyer exits. |

| Off-market channels protect value | Large portfolio sales frequently use off-market processes to manage tenant confidentiality and transaction complexity. |

What the 2026 market is actually telling sellers

The industrial market in 2026 is not forgiving of sellers who treat all industrial assets as interchangeable. Institutional underwriting standards have tightened around the spec stack in ways that were not standard practice five years ago. A building that traded easily in 2019 on income alone now faces scrutiny on clear height, ESFR compliance, and trailer parking ratios before a buyer will commit to a letter of intent.

What I observe consistently is that sellers who invest in pre-sale documentation and spec verification close faster and at prices closer to their initial ask. The sellers who struggle are those who assume their asset’s location or occupancy will carry the transaction without addressing spec deficiencies or documentation gaps.

The shift toward off-market portfolio sales is also real and accelerating. Institutional sellers managing large portfolios increasingly prefer controlled processes with pre-qualified buyers over broad market exposure. This protects tenant relationships, limits operational disruption, and allows for more precise pricing. For single-asset sellers, the lesson is that broker selection and buyer targeting matter as much as the asset itself.

Leveraging specialized partners with direct access to institutional buyer networks, auction capabilities, and industrial asset expertise is not optional for complex dispositions. It is the difference between a transaction that closes on schedule at market pricing and one that stalls in diligence or reprices at the last moment.

— Vector

How Maascompanies supports complex industrial property sales

Maascompanies brings decades of experience managing industrial real estate transactions and asset liquidations across manufacturing, logistics, and processing sectors worldwide. When a disposition involves specialized facilities, surplus equipment, or multi-asset portfolios, Maascompanies applies an aggressive, targeted marketing approach that reaches qualified institutional and operational buyers directly.

A current example of this expertise is the biodiesel plant and processing facility auction, which includes oilseed processing, grain handling, manufacturing and warehouse facilities, retail fuel stations, and surplus equipment. This project illustrates the full scope of Maascompanies’ capability to manage complex, multi-asset industrial dispositions from documentation through closing. To explore how Maascompanies can support your industrial asset sale, contact the team directly for a tailored recovery strategy.

FAQ

What is the definition of industrial property sales?

Industrial property sales are the transfer of real estate assets used for manufacturing, warehousing, distribution, and logistics, requiring specialized valuation based on physical specifications, lease structure, and institutional market standards.

What is the spec stack in industrial real estate?

The spec stack is the set of physical building attributes, including clear height, dock doors, ESFR sprinklers, floor load, column grid, and trailer parking, that institutional buyers use to determine asset quality and pricing.

How are cap rates used in industrial property valuation?

Cap rates translate net operating income into asset value. Class A industrial assets trade at cap rates in the high 4s to low 6s in 2026, while older secondary properties trade at 6.5% to 8.5% or higher.

What documentation is needed to sell an industrial property?

Sellers should prepare zoning records, power capacity certifications, dock and site access specifications, environmental reports, and current lease abstracts. Incomplete documentation is a leading cause of buyer walkaways during due diligence.

When should industrial property sellers use off-market sales channels?

Off-market channels are appropriate for large portfolio dispositions, assets with sensitive tenant profiles, or transactions where broad market exposure could disrupt operations or tenant relationships.

Recommended

- Real estate auctions: Fast liquidation for industrial assets | Blog | Insights on Asset Liquidation and Auction Trends

- How to Plan Government Asset Sales for Spring 2026 | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends