Blog

Role of Lenders in Liquidation: A 2026 Guide

TL;DR:

- Lenders play a crucial role in liquidation by asserting security interests, filing claims, and actively participating in oversight. Their recovery depends on their position in the statutory hierarchy, the type of security held, and their engagement during insolvency. Proactive lenders who monitor asset sales, challenge undervalued transactions, and join liquidation committees recover more and protect their interests.

Lenders are defined as secured or unsecured creditors whose rights, recovery outcomes, and legal obligations are directly shaped by every decision made during a company’s liquidation. The role of lenders in liquidation extends well beyond passive debt collection. Lenders must assert security interests, navigate statutory creditor hierarchies, comply with bankruptcy procedural rules, and actively engage with liquidation committees to protect their claims. Whether you represent a commercial bank holding a fixed charge, a mortgage lender managing post-petition fees, or an unsecured trade creditor, your position in the priority waterfall determines how much you recover and how quickly. This guide explains the creditor hierarchy, lender responsibilities during insolvency, and the practical strategies that separate proactive lenders from those who accept reduced recoveries.

What is the role of lenders in liquidation proceedings?

Lenders occupy the most consequential position in any corporate insolvency. Their influence over the liquidation process and lenders’ ultimate recovery depends on the type of security held, the speed of procedural action, and the quality of engagement with the appointed liquidator.

Secured lenders holding fixed charges rank first in the payment waterfall. That priority gives them significant leverage over asset disposition decisions, including the timing and method of sale. Unsecured lenders, by contrast, sit near the bottom of the hierarchy and often recover cents on the dollar unless they organize collectively through a creditor committee.

The impact of lenders on liquidation outcomes is measurable. Lenders who file timely proofs of claim, monitor asset valuations, and challenge underperforming liquidators consistently recover more than those who wait for distributions. Passive creditor behavior is the single most common reason for avoidable recovery shortfalls.

Financial institutions in liquidation also carry compliance obligations that do not pause during insolvency proceedings. Mortgage servicers, equipment lenders, and revolving credit facilities each face specific statutory requirements that must be met from the moment a bankruptcy petition is filed.

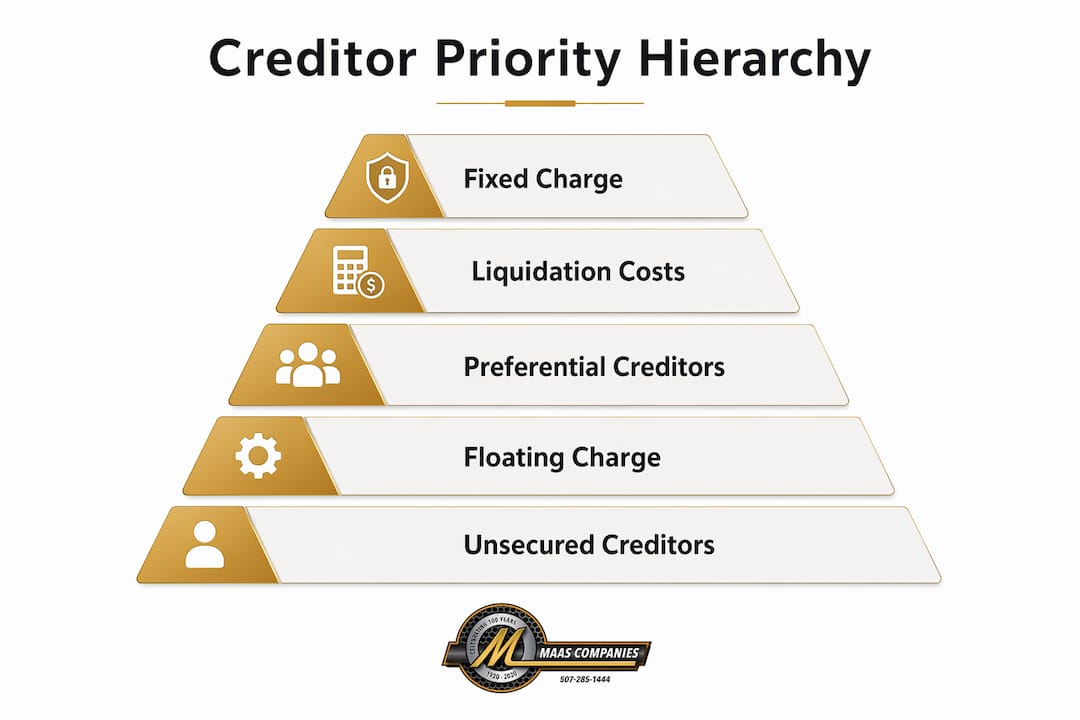

What is the creditor priority hierarchy and how does it affect lenders?

The creditor priority order in UK liquidation ranks fixed charge holders first, liquidation costs second, preferential creditors third, a prescribed part for unsecured creditors fourth, floating charge holders fifth, unsecured creditors sixth, and shareholders last. That sequence is statutory and cannot be altered by agreement between parties.

The prescribed part is a carve-out that materially affects floating charge lenders. It is calculated as 50% of the first £10,000 of floating charge realizations and 20% of anything above £10,000, capped at £800,000. Floating charge holders must account for this reduction when modeling expected recovery before a liquidation commences.

The distinction between secured and unsecured creditor positions is the most critical variable in any recovery analysis:

- Fixed charge holders retain direct enforcement rights over specific assets such as property, plant, and specialized equipment. They can appoint a receiver independently of the liquidation estate in many jurisdictions.

- Floating charge holders hold security over a class of assets that changes over time, such as inventory or receivables. Their recovery is subject to the prescribed part deduction and ranks below preferential creditors.

- Unsecured creditors include trade suppliers, bondholders, and subordinated lenders. They share in the residual estate after all senior claims are satisfied, which in many liquidations produces little or no recovery.

- Shareholders receive distributions only after all creditor classes are paid in full. In practice, shareholders rarely recover anything in a formal liquidation.

| Creditor class | Security type | Typical recovery position |

|---|---|---|

| Fixed charge holders | Specific asset security | First priority, highest recovery |

| Preferential creditors | Statutory preference | Ahead of floating charges |

| Floating charge holders | Circulating asset security | Subject to prescribed part deduction |

| Unsecured creditors | None | Residual estate only |

| Shareholders | Equity | Last in line |

Understanding where you sit in this table before a borrower files for insolvency is not optional. It determines every negotiation, every motion, and every committee decision you make throughout the process.

What are lender responsibilities and obligations during bankruptcy?

Lender responsibilities in bankruptcy are procedural, time-sensitive, and non-negotiable. Missing a deadline does not reduce your claim. It eliminates it.

Mortgage lenders face one of the most specific compliance requirements in the process. They must file notices for payment changes and post-petition fees within 180 days using Form 410S-2 to maintain recoverability. Failure to file within that window forfeits the right to collect those fees entirely, regardless of the underlying loan agreement.

The automatic stay is the second major compliance obligation. Under 11 U.S.C. 362(k), a willful violation of the automatic stay exposes lenders to sanctions including actual damages, punitive damages, and attorney’s fees. The stay takes effect the moment a bankruptcy petition is filed and immediately halts all collection actions, foreclosure proceedings, and repossession efforts.

Key lender obligations from day one of a bankruptcy filing include:

- Halt all automated billing and collection systems immediately upon receiving notice of the bankruptcy filing to avoid inadvertent stay violations.

- Stop foreclosure and repossession actions already in progress, even if they are days from completion.

- File a proof of claim by the court-established bar date to preserve the right to receive any distribution from the estate.

- Engage bankruptcy counsel to evaluate whether a motion for relief from the automatic stay is appropriate given the collateral position and debtor’s equity.

- Monitor the docket for asset sale motions, plan filings, and liquidation reports that affect your collateral.

Pro Tip: Set up automated docket alerts through PACER for every bankruptcy case where your institution holds a claim. Missing a sale motion or a plan confirmation deadline is the most preventable cause of recovery loss.

Compliance with these obligations is not merely defensive. Lenders who establish procedural discipline from the outset are better positioned to assert rights aggressively when the opportunity arises.

How do lenders participate in creditor meetings and liquidation committees?

Creditor meetings and liquidation committees are the primary mechanisms through which lenders exercise collective oversight of the insolvency process. Active participation in these structures is one of the highest-leverage actions available to any creditor.

Creditors can demand an in-person meeting if they meet thresholds of 10% by value, 10% by number, or a minimum of 10 individual creditors. That threshold is low enough that a single institutional lender holding a significant claim can trigger a meeting independently.

Liquidation committees typically have 3 to 5 members, with an odd number to prevent voting deadlock. The committee structure gives participating lenders direct authority over the liquidator’s conduct, fees, and strategic decisions.

The steps to establish and operate an effective creditor committee are as follows:

- Identify the threshold requirement. Confirm whether your claim meets the 10% by value threshold or whether you need to coordinate with other creditors to reach the minimum number requirement.

- Nominate committee members. Propose candidates at the creditors’ meeting. Institutional lenders with the largest claims typically secure representation, but smaller creditors can also participate.

- Review liquidator reports. Committees receive detailed reports on asset realizations, costs, and distributions. Review these reports critically, not as a formality.

- Approve or challenge liquidator fees. Committees have direct authority over remuneration. Excessive fee structures reduce the pool available for distribution to creditors.

- Exercise removal authority if warranted. Committees can replace underperforming liquidators who are not pursuing viable claims or maximizing asset values aggressively enough.

Pro Tip: If you hold a floating charge or are a significant unsecured creditor, joining the liquidation committee is almost always worth the time investment. The oversight access alone can prevent fee overruns that would otherwise reduce your distribution.

Proactive creditor engagement and forming creditor committees enhance transparency and can improve recovery outcomes beyond what passive creditor roles produce. The committee structure is underutilized by most institutional lenders, which is a significant missed opportunity.

What strategies can lenders employ to maximize recovery?

Lenders during company insolvency who take a strategic posture from the outset recover more than those who rely on the liquidator to act in their interest. The liquidator’s duty is to the general body of creditors, not to any individual lender’s security position.

The most effective recovery strategies for lenders include:

- File for relief from the automatic stay early. Proactive lenders who engage early and file relief from stay motions when appropriate consistently outperform passive creditors. Delay favors the debtor and reduces the lender’s negotiating leverage.

- Monitor asset disposition closely. Review every proposed sale of collateral for adequacy of marketing, valuation methodology, and sale price. Inadequate marketing of industrial assets, manufacturing equipment, and real property is the most common source of below-market recoveries.

- Challenge undervalued asset sales. File objections to proposed sales where the marketing process was insufficient or the purchase price does not reflect fair market value. Courts take these objections seriously when supported by independent appraisal evidence.

- Engage insolvency professionals for independent valuation. Do not rely solely on the liquidator’s appointed valuer. Commission independent appraisals for significant collateral, particularly for specialized industrial equipment, processing plants, and commercial real estate.

- Analyze third-party guarantees and mortgages separately. Relinquishing security in a borrower’s liquidation does not extinguish third-party guarantees or mortgages. Recent NCLT rulings confirm that lenders must analyze these interests independently to avoid unintentional waiver of enforceable claims.

Jurisdiction-specific rules govern how security relinquishment affects third-party claims. Lenders must understand these legal nuances to safeguard the full scope of their recovery rights across all available collateral.

The liquidation process and lenders who navigate it successfully share one common trait: they treat insolvency as an active legal and commercial process, not an administrative wind-down. The difference between a 40% recovery and a 70% recovery on the same collateral often comes down to the quality of the marketing process and the lender’s willingness to challenge inadequate outcomes.

Independent enforcement of security interests outside the liquidation estate requires strict statutory compliance. Missed notification deadlines lead to loss of enforcement rights, regardless of the underlying security agreement’s terms.

Key takeaways

Lenders who combine procedural discipline with active creditor engagement consistently achieve superior recovery outcomes compared to those who adopt a passive stance during liquidation proceedings.

| Point | Details |

|---|---|

| Creditor priority is statutory | Fixed charge holders recover first; unsecured creditors share only the residual estate after all senior claims are satisfied. |

| Deadline compliance is non-negotiable | Mortgage lenders must file Form 410S-2 within 180 days of incurring post-petition fees or forfeit those collections permanently. |

| Automatic stay requires immediate action | Halt all collection and foreclosure actions the moment a bankruptcy filing is received to avoid sanctions under 11 U.S.C. 362(k). |

| Committee participation improves outcomes | Joining a liquidation committee gives lenders direct authority over liquidator fees, conduct, and asset disposition strategy. |

| Third-party security survives relinquishment | Releasing security in the borrower’s liquidation does not extinguish guarantees or mortgages held against third parties. |

Why passive lenders leave money on the table

The most persistent misconception I encounter among institutional lenders is that the liquidator will protect their interests by default. That assumption is wrong, and it costs creditors real money in every significant insolvency I have observed.

Liquidators are officers of the court with duties to the general body of creditors. They are not advocates for any individual lender’s security position. A floating charge holder who does not attend creditor meetings, review asset sale proposals, or challenge inadequate marketing processes will almost always recover less than one who does. The gap is not marginal. On complex industrial liquidations involving processing plants, manufacturing equipment, and commercial real estate, the difference between a well-marketed sale and a distressed fire sale can represent 30% to 50% of collateral value.

The shift from a collection mindset to a procedural mindset is the single most important change a lender can make when a borrower files for insolvency. Collection thinking focuses on the debt. Procedural thinking focuses on the process, the timeline, the asset values, and the legal mechanisms available to protect and enforce rights. Lenders who coordinate with bankruptcy counsel from day one, evaluate stay relief motions early, and engage with the liquidation committee consistently outperform those who wait for distributions.

Regulatory complexity in 2026 adds another layer of urgency. Jurisdiction-specific rules on security enforcement, prescribed parts, and committee formation vary significantly across the United States, the United Kingdom, and other common law jurisdictions. Lenders operating across multiple jurisdictions cannot apply a single procedural template. Each insolvency requires a jurisdiction-specific legal review before any action is taken.

— Vector

How Maascompanies supports lenders through complex liquidations

Lenders managing collateral through a formal liquidation need more than a liquidator’s report. They need an experienced asset recovery partner who understands how to market industrial plants, manufacturing equipment, and commercial real estate to the right buyers at the right time.

Maascompanies brings decades of experience in auction management, asset valuation, and targeted marketing of industrial and commercial assets to lenders, special asset managers, and insolvency professionals worldwide. From biodiesel plants to processing facilities, Maascompanies structures recovery programs that maximize realized value, not just speed of sale. Review Maascompanies’ current asset recovery projects to see active liquidations in progress, or explore the full Maascompanies services portfolio to discuss how a structured marketing program can improve your recovery outcome.

FAQ

What is the role of lenders in liquidation?

Lenders are key stakeholders in liquidation who assert security interests, file proofs of claim, participate in creditor committees, and monitor asset disposition to maximize recovery. Their position in the statutory creditor priority hierarchy determines the order and amount of any distribution they receive.

How does the automatic stay affect lenders during bankruptcy?

The automatic stay halts all collection actions, foreclosure proceedings, and repossession efforts immediately upon a bankruptcy filing. Willful violations expose lenders to sanctions including damages and attorney’s fees under 11 U.S.C. 362(k).

What is a liquidation committee and why should lenders join?

A liquidation committee is a body of 3 to 5 creditors elected to oversee the liquidator’s conduct, approve fees, and authorize key decisions. Lenders who join committees gain direct oversight authority that can prevent fee overruns and improve asset recovery outcomes.

Can a lender enforce a third-party guarantee after releasing security in liquidation?

Yes. Relinquishing security in a borrower’s liquidation does not extinguish third-party guarantees or mortgages. Lenders must analyze these interests separately and preserve enforcement rights through appropriate legal action.

What is the prescribed part in a UK liquidation?

The prescribed part is a statutory carve-out from floating charge realizations reserved for unsecured creditors. It equals 50% of the first £10,000 realized and 20% of amounts above that threshold, capped at £800,000, and directly reduces floating charge holder recoveries.

Recommended

- How Industrial Plant Liquidation Maximizes Recovery Value for Lenders | Blog | Insights on Asset Liquidation and Auction Trends

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Plant liquidation strategies: maximize recovery in 2026 | Blog | Insights on Asset Liquidation and Auction Trends

- Equipment liquidation explained: maximizing asset recovery | Blog | Insights on Asset Liquidation and Auction Trends