Blog

What Is Forced Liquidation: A Financial Professional’s Guide

TL;DR:

- Forced liquidation is an involuntary, rapid sale initiated by creditors, courts, or brokers to settle debts, often yielding only 40-60% of assets’ fair market value. It removes the owner’s control over timing and sale conditions, resulting in significantly lower recovery rates compared to orderly, managed sales. Proactive management of collateral, legal agreements, and early recognition of distress are essential to mitigate the financial impact of forced liquidation.

Forced liquidation is widely misunderstood. Most investors and business owners treat it as a straightforward forced sale, when in reality it represents a legally structured, financially consequential process that can strip asset value far below market expectations. Understanding what is forced liquidation, how it triggers, and what it means for recovery outcomes is not optional knowledge for serious financial professionals. It is the difference between preserving equity and watching it disappear under compressed timelines and adversarial sale conditions.

Table of Contents

- Key takeaways

- What is forced liquidation: definition and legal framework

- How forced liquidation works in trading and insolvency

- Valuation impacts: forced liquidation value vs. orderly liquidation value

- Effects of forced liquidation on investors, businesses, and creditors

- Managing and mitigating forced liquidation risks

- My perspective on what professionals consistently get wrong

- How Maascompanies helps maximize recovery in forced liquidation situations

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Forced liquidation is involuntary | A creditor, broker, or court initiates the sale, removing the owner’s control over timing and price. |

| Asset recovery rates are significantly lower | Forced liquidation typically yields 40-60% of fair market value due to compressed timelines. |

| Brokers can act without prior notice | Margin agreements legally allow brokers to liquidate positions without notifying the account holder. |

| Orderly sales recover 20%+ more value | Allowing adequate marketing time improves recovery rates substantially compared to forced auctions. |

| Proactive management reduces risk | Monitoring margin buffers, collateral quality, and liquidation clauses limits exposure before a forced event occurs. |

What is forced liquidation: definition and legal framework

Forced liquidation is the involuntary, rapid sale of assets initiated by a creditor, broker, or court to satisfy outstanding financial obligations. The owner of the assets does not choose the timing, the venue, or the sale price. That control is transferred entirely to the party enforcing the liquidation, whether that is a brokerage firm executing a margin call or a bankruptcy court directing a trustee to sell business assets.

The forced liquidation meaning extends across several distinct legal and financial contexts:

- Margin calls in leveraged trading: When a trader’s account equity drops below the required maintenance margin, the broker issues a margin call. If the trader cannot deposit additional funds, the broker forces the sale of positions to restore minimum margin requirements.

- Loan defaults: A lender holding collateral against a defaulted loan will seize and sell pledged assets to recover the outstanding balance.

- Bankruptcy proceedings: Under Chapter 7 bankruptcy in the U.S., a court-appointed trustee takes control of a debtor’s non-exempt assets and liquidates them for creditor benefit.

- Court orders: Regulatory bodies or courts can mandate asset sales as part of enforcement actions, judgments, or receivership proceedings.

“Forced liquidation is a last-resort risk control mechanism to prevent losses exceeding account balances, automatically triggered if maintenance margins are breached.” This principle applies equally in trading environments and business insolvency, where financial distress triggers action that the asset owner can no longer prevent.

The critical distinction between forced liquidation vs. voluntary liquidation lies in control. In a voluntary or orderly liquidation, the asset owner manages the process, selects the disposition method, and benefits from adequate marketing time. In a forced liquidation, urgency overrides value optimization. The process prioritizes obligation satisfaction, not recovery maximization.

How forced liquidation works in trading and insolvency

Understanding how does forced liquidation work requires separating two primary operational contexts: leveraged trading accounts and business bankruptcy proceedings. The mechanics differ, but the outcome in both cases is the same. The asset owner loses control, and the proceeds are applied to satisfy creditors rather than return maximum value to the owner.

Forced liquidation in leveraged trading

- Initial margin requirement: When opening a leveraged position, the trader deposits an initial margin, a percentage of the total position value. This creates a buffer against adverse price movements.

- Maintenance margin threshold: As market prices move against the position, account equity declines. Brokers set a maintenance margin level, typically below the initial margin, as the minimum acceptable equity level.

- Margin call issuance: When equity falls to the maintenance margin, the broker issues a margin call requiring the trader to deposit additional funds or close positions voluntarily.

- Forced position closure: If the trader fails to meet the margin call, brokers execute forced closure to prevent equity from turning negative. Auto-liquidation systems monitor accounts continuously and trigger immediate closure when maximum loss limits are breached.

- Execution at market price: Forced positions close at prevailing market prices. During volatile conditions, this can result in significant slippage, meaning the actual execution price is worse than the quoted price at the time of the margin call.

Pro Tip: Review your margin agreement carefully before opening leveraged positions. Most brokerage agreements grant firms the right to liquidate portfolios at their discretion without prior notice. Understanding this clause eliminates any misplaced expectation of advance warning.

Forced liquidation in business bankruptcy

In a business context, forced liquidation typically follows a court petition, creditor action, or regulatory order. A trustee or receiver takes possession of assets, assesses their value, and conducts a public auction to generate proceeds. Court-mandated forced liquidations prioritize creditor recovery over maximizing the sale price, which means assets are sold under auction conditions rather than through targeted marketing campaigns that would attract qualified buyers.

The process moves quickly by design. Carrying costs, legal fees, and creditor pressure all compress the timeline. This speed is precisely what suppresses recovery values.

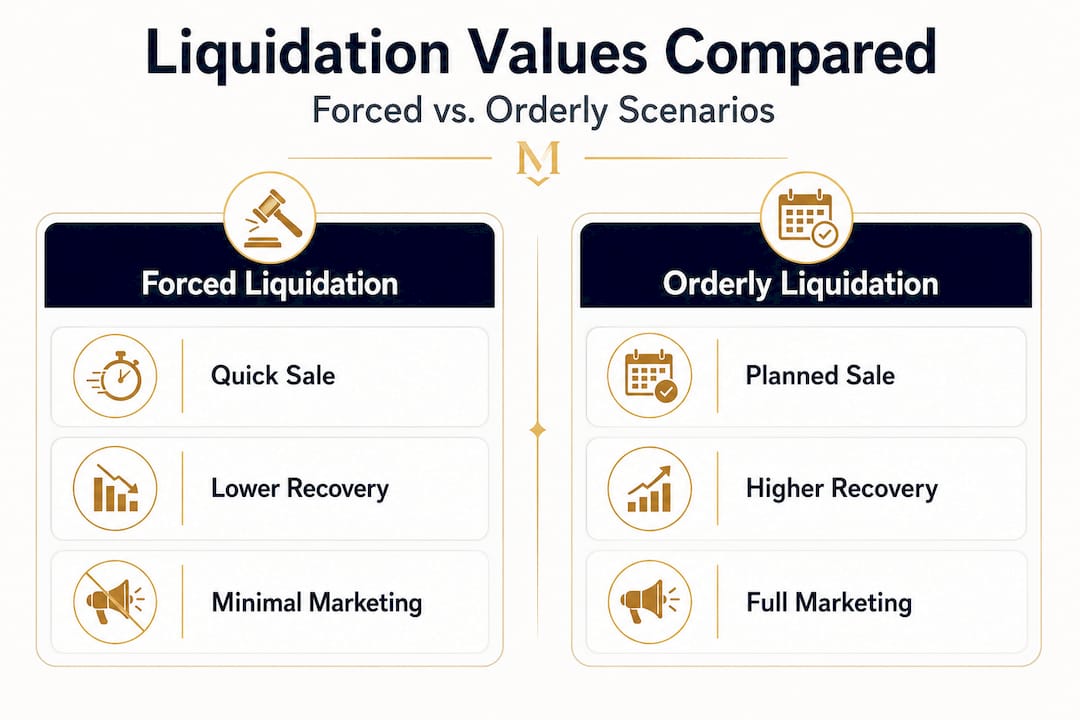

Valuation impacts: forced liquidation value vs. orderly liquidation value

No aspect of forced liquidation carries more financial weight than its effect on asset values. Two distinct appraisal standards capture this difference: Forced Liquidation Value (FLV) and Orderly Liquidation Value (OLV).

| Valuation Type | Timeline | Typical Recovery Rate | Sale Conditions |

|---|---|---|---|

| Forced Liquidation Value (FLV) | Days to weeks | 40-60% of fair market value | Public auction, distress conditions, limited marketing |

| Orderly Liquidation Value (OLV) | 3-9 months | 60-80% of fair market value | Structured marketing, targeted buyer outreach, negotiated terms |

FLV represents the price an asset is expected to bring when sold under immediate, compelled conditions with minimal marketing time. OLV, by contrast, assumes adequate exposure to the market, a reasonable pool of informed buyers, and the ability to negotiate. Orderly sales can improve recovery rates by more than 20% compared to forced auctions.

The gap between FLV and OLV matters significantly for lenders assessing collateral coverage and for insolvency professionals setting creditor recovery expectations. A lender who bases a loan amount on fair market value without accounting for FLV discounts is exposed to a meaningful shortfall if the borrower defaults and assets must be liquidated quickly.

The spread between forced and orderly liquidation values is a decisive factor in collateral valuation. Appraisers and financial professionals who treat FLV and OLV as interchangeable create material risk in their portfolios.

Effects of forced liquidation on investors, businesses, and creditors

The effects of forced liquidation extend well beyond the immediate sale event. Each stakeholder category faces a distinct set of consequences.

For investors in leveraged trading:

- Positions close automatically at market price, often at the worst possible moment in a price cycle.

- Slippage during volatile markets means execution prices can be significantly worse than the margin call trigger level.

- In extreme cases, rapid price movements can result in a negative account balance, leaving the investor legally obligated to repay the deficit to the brokerage.

- Auto-liquidation systems prioritize rapid exposure neutralization over price optimization, which means the investor’s financial interest is secondary to market stability.

For business owners:

Forced liquidation during bankruptcy removes all operational control. The owner cannot time the sale, select buyers, or negotiate terms. Assets that would attract premium prices through targeted industry marketing are instead offered in generic public auctions where the buyer pool is limited and uniformed.

“Most investors are surprised that brokers can liquidate accounts without notice due to terms in margin agreements that prioritize market and broker capital protection.” The same dynamic applies to secured lenders, whose right to liquidate collateral without consent is typically embedded in loan documentation from the outset.

For creditors:

Creditor priority rules determine who receives proceeds and in what order. Senior secured creditors recover first; unsecured creditors often recover very little. Practical constraints, including auction fees, trustee compensation, legal costs, and the depressed prices inherent in forced sales, can erode proceeds significantly before subordinate creditors see any distribution.

Pro Tip: If you hold collateral against a business loan, require appraisals that specify both FLV and OLV. Use FLV as your conservative baseline for loan-to-value calculations, not fair market value.

Managing and mitigating forced liquidation risks

Forced liquidation is not inevitable. Investors, business owners, and lenders each have tools to reduce exposure and, when forced liquidation cannot be avoided, to improve recovery outcomes.

- Maintain margin buffers above the minimum. In leveraged trading, holding equity well above the maintenance margin threshold creates a cushion against sudden price moves. Setting a personal risk threshold above the broker’s maintenance level provides time to make deliberate decisions rather than react to an automated closure.

- Monitor collateral quality continuously. For lenders and asset managers, the condition and market liquidity of pledged collateral should be assessed periodically, not just at loan origination. Collateral that was liquid at origination may become illiquid as market conditions shift.

- Negotiate liquidation clauses before signing. Both margin agreements and loan documents contain liquidation provisions that vary significantly between counterparties. Engaging legal counsel to review and negotiate these clauses before signing can limit adverse outcomes later.

- Pursue orderly sale alternatives when possible. When financial distress is recognized early, an orderly negotiated sale typically generates substantially better recovery than waiting until a court or creditor forces a distressed auction. Time is the single most valuable resource in asset disposition.

- Engage specialized asset disposition partners early. Firms with established buyer networks and industry-specific marketing capabilities can maximize recovery in complex liquidations even under compressed timelines, particularly for industrial equipment, real estate, and commercial assets. The difference between a generic auction and a targeted marketing campaign is often the difference between FLV and OLV recovery rates.

The decision between forced liquidation vs. voluntary liquidation often comes down to how early warning signs are recognized and acted upon. Organizations that monitor financial covenants, leverage ratios, and collateral values proactively retain options that disappear once a creditor or court takes control.

My perspective on what professionals consistently get wrong

I’ve worked with investors, lenders, and business owners across enough asset recovery situations to recognize a consistent pattern. The damage from forced liquidation rarely begins at the moment of forced sale. It begins months earlier, when decision-makers either fail to recognize the warning signs or convince themselves that the situation will self-correct.

What I’ve learned is that the psychology of delayed action is more financially destructive than almost any market condition. Investors holding leveraged positions hold too long, expecting a reversal. Business owners resist engaging restructuring advisors because doing so feels like admitting failure. Lenders avoid exercising remedies because the process is uncomfortable. By the time the forced liquidation mechanism activates, the controllable window has already closed.

The other misconception I encounter repeatedly is the belief that brokers and creditors are acting against the borrower’s interests when they force a sale. They are not. They are executing contractual rights that were clearly disclosed at the outset. The real failure is not reading and understanding those agreements before signing. Margin agreements are not formalities; they are the operating rules for a high-stakes environment.

For any financial professional or business owner with exposure to leveraged assets or collateral-backed obligations, the time to understand forced liquidation mechanics is well before they become relevant. Proactive management of margin levels, collateral quality, and legal documentation is the practical answer to a problem that is otherwise very expensive to learn about through direct experience.

— Vector

How Maascompanies helps maximize recovery in forced liquidation situations

When forced liquidation cannot be avoided, the quality of the asset disposition process becomes the primary determinant of recovery value. Maascompanies has extensive experience managing complex industrial asset sales under the compressed timelines and creditor constraints that define forced liquidation scenarios.

Maascompanies applies targeted marketing strategies, established industry buyer networks, and technical expertise to reduce the gap between FLV and OLV outcomes, even when sale timelines are compressed. A recent example is the 3-MGY Biodiesel Plant auction, which involved multiple facility types and surplus equipment across a complex disposition structure. Achieving competitive recovery on assets of that scale and complexity requires more than a standard auction listing.

If your organization is facing a forced or time-constrained asset disposition, Maascompanies offers specialized liquidation services tailored to industrial plants, equipment, real estate, and commercial properties. Contact Maascompanies to discuss a recovery strategy before timeline pressure forces a suboptimal outcome.

FAQ

What is the forced liquidation meaning in finance?

Forced liquidation is the involuntary sale of assets initiated by a creditor, broker, or court to satisfy outstanding financial obligations, typically resulting in asset sales at 40-60% of fair market value due to compressed timelines and distressed conditions.

Can a broker liquidate my account without notifying me first?

Yes. Most margin agreements legally grant brokers the right to liquidate portfolios without prior notice, as their primary obligation is protecting their capital and maintaining market stability rather than serving the investor’s timing preferences.

What is a forced liquidation example in business?

A Chapter 7 bankruptcy is a direct forced liquidation example. A court-appointed trustee seizes non-exempt business assets and sells them through public auction, with proceeds distributed to creditors according to priority rules, typically leaving equity holders with little or nothing.

How does forced liquidation differ from orderly liquidation?

Forced liquidation occurs under time pressure with minimal marketing, yielding lower recovery rates. Orderly liquidation allows 3-9 months of structured marketing and negotiation, typically recovering 20% more than forced auctions through targeted buyer outreach and competitive bidding.

What are the main reasons for forced liquidation?

The primary reasons for forced liquidation include margin calls in leveraged trading accounts, loan defaults triggering creditor collateral seizure, court-ordered bankruptcy proceedings under Chapter 7, and regulatory enforcement actions requiring asset divestiture.

Recommended

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Equipment liquidation explained: maximizing asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Plant liquidation strategies: maximize recovery in 2026 | Blog | Insights on Asset Liquidation and Auction Trends

- Maximize Asset Recovery: Top Real Estate Liquidation Methods | Blog | Insights on Asset Liquidation and Auction Trends