Blog

Bankruptcy Auctions Explained: Maximizing Asset Recovery

TL;DR:

- Bankruptcy auctions, when properly structured, can yield recovery rates comparable to private sales while ensuring transparency and maximizing asset value. Key participants include the debtor, secured creditors, stalking horse bidders, and the court, with the process typically lasting 45 to 90 days. Success relies heavily on pre-auction strategy, thorough due diligence, and targeted marketing to attract competitive bids and protect stakeholder interests.

Bankruptcy auctions carry an undeserved reputation for producing fire-sale prices. In practice, when structured and marketed correctly, a well-run Section 363 sale can generate recovery rates that rival or surpass private negotiated transactions, all while offering court-supervised transparency that protects every stakeholder. For private equity firms, secured lenders, and corporate decision-makers, understanding the mechanics, participants, and strategic levers of bankruptcy auctions is not optional. It is the difference between leaving value on the table and extracting the maximum return from a distressed asset portfolio.

Table of Contents

- What is a bankruptcy auction?

- Stages of a bankruptcy auction: How the process works

- Key bidders: Stalking horse, credit bidders, and competitive strategies

- Nuances and risks: Legal pitfalls and special scenarios

- Benchmarks and outcomes: Recovery rates and process efficiency

- Why the real lever in bankruptcy auctions is the pre-auction strategy

- Maximize asset recovery with proven bankruptcy auction experts

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Court-supervised auctions | Bankruptcy auctions are run by courts to maximize asset value through competitive bidding. |

| Key phases and stakeholders | Successful outcomes depend on pre-auction strategy, court approval, and savvy bidding. |

| Stalking horse and credit bidding | These strategies help set the stage and protect lender interests. |

| Beware of legal pitfalls | Product liability and bid protection disputes can complicate the process. |

| Recovery rates vary | Process efficiency and market prep are key to maximizing returns from bankruptcy auctions. |

What is a bankruptcy auction?

A bankruptcy auction is a court-supervised competitive sale process designed to extract maximum value from a debtor’s assets while maintaining transparency for all creditors. As the American Bar Association notes, a Section 363 sale is a court-supervised process where a debtor in Chapter 11 sells assets outside ordinary business through competitive bidding to maximize value. The process derives its name from Section 363 of the US Bankruptcy Code, which grants the debtor authority to sell property of the estate outside the normal course of business, subject to court approval.

The primary goals of a bankruptcy auction are straightforward: maximize the value returned to the estate, ensure transparency for all creditors and parties in interest, and provide a buyer with clean title to acquired assets. These goals align closely with what lenders and equity sponsors need when managing distressed situations.

“A bankruptcy auction is not a distress sale by default. It is a structured competitive process that, when properly marketed, attracts multiple qualified bidders and drives pricing toward fair market value or above.”

Key participants in every bankruptcy auction include:

- The debtor: The company or individual in bankruptcy proceedings, represented by counsel and typically a financial advisor.

- Secured creditors: Lenders holding liens on specific assets, who may credit bid or consent to the sale.

- The stalking horse bidder: A pre-selected buyer who sets the floor price and receives negotiated protections.

- Qualified competing bidders: Third-party buyers, strategic acquirers, or private equity firms who meet court-approved criteria.

- The bankruptcy court: The judicial authority that approves procedures, hears objections, and confirms the final sale.

Bankruptcy auctions are most commonly used when a Chapter 11 debtor needs to sell substantially all assets quickly, when a going-concern sale is preferable to piecemeal liquidation, or when a negotiated private sale would not generate sufficient creditor confidence. Understanding how to leverage auction machinery for recovery is essential for any professional involved in distressed asset management.

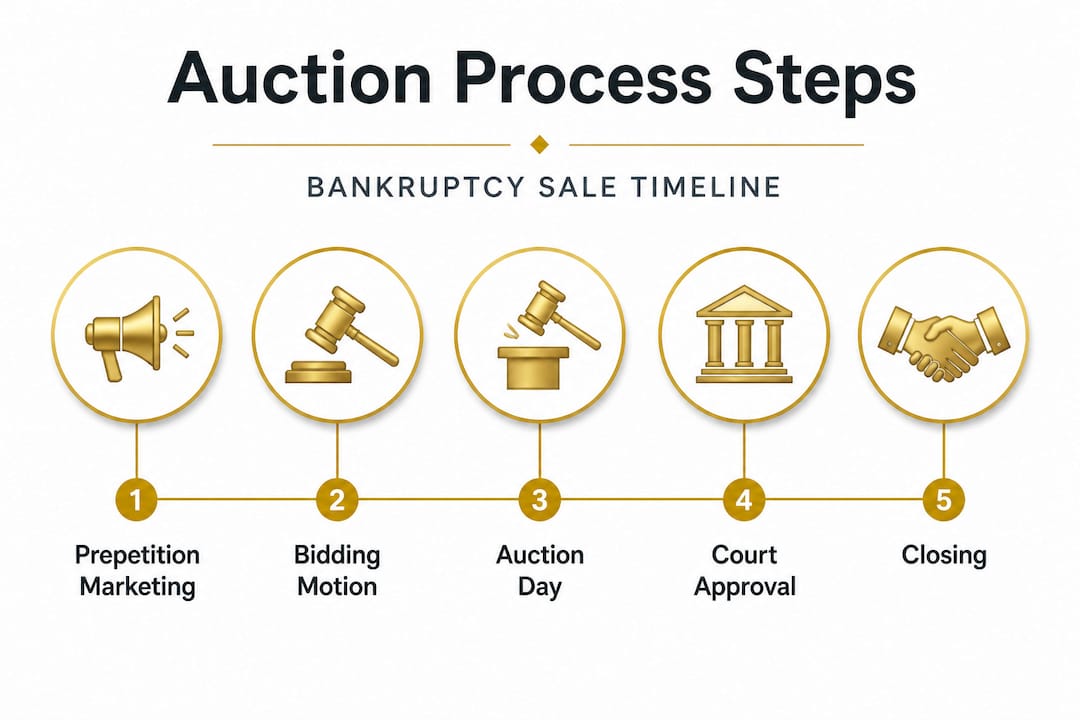

Stages of a bankruptcy auction: How the process works

The bankruptcy auction process follows a structured, predictable sequence that professionals can plan around and optimize. The five-stage process moves from prepetition marketing and stalking horse selection (with a typical breakup fee of 1 to 3%), through court approval of bidding procedures, additional marketing and the live auction for the highest and best bid, court approval of winning and backup bids, and finally closing with free-and-clear title under Section 363(f).

Here is how each stage unfolds in practice:

- Prepetition marketing and stalking horse selection. Before the bankruptcy filing, the debtor and its advisors identify and negotiate with a stalking horse bidder. This bidder sets the price floor and receives protections in exchange for committing early. Effective marketing at this stage attracts the broadest pool of potential buyers.

- Court approval of bidding procedures. The debtor files a motion requesting court approval of the auction rules, including qualification requirements, minimum bid increments, breakup fee amounts, and the auction date. Creditors and other parties can object at this stage.

- Additional marketing and buyer qualification. Following court approval, the debtor’s marketing team distributes information to qualified buyers, conducts due diligence sessions, and qualifies competing bidders. This phase is where aggressive, targeted marketing pays dividends in final recovery.

- The live auction and highest and best bid determination. Qualified bidders compete in a structured auction, often conducted over one or more rounds. The debtor and its advisors select the highest and best bid, which may not always be the numerically highest offer if other terms are superior.

- Court approval and closing with free-and-clear title. The court holds a sale hearing, considers any objections, and enters a sale order. Closing follows, transferring title free and clear of most liens and claims under Section 363(f).

The timeline typically runs 45 to 90 days from the bidding procedures motion to closing. Importantly, a good faith finding under Section 363(m) protects the buyer from having the sale reversed on appeal if the sale order is not stayed. This protection is critical for buyers who need certainty of closing.

| Stage | Typical duration | Key action |

|---|---|---|

| Prepetition marketing | 2 to 6 weeks | Stalking horse negotiation |

| Bidding procedures approval | 1 to 2 weeks | Court hearing and order |

| Marketing and qualification | 2 to 4 weeks | Buyer outreach and diligence |

| Auction | 1 day to 1 week | Competitive bidding |

| Court approval and closing | 1 to 2 weeks | Sale order and title transfer |

Pro Tip: Engage your marketing and liquidation team before the bankruptcy filing, not after. Pre-marketing to qualified buyers during the stalking horse phase consistently produces more competitive auctions and higher final recovery. Firms that speed up asset disposition through early preparation routinely outperform those that wait for court approval before beginning outreach. For a real-world example of this process in action, review the Kingman grain elevator bankruptcy auction to see how structured marketing drives competitive outcomes.

Key bidders: Stalking horse, credit bidders, and competitive strategies

Understanding who participates in bankruptcy auctions and how each party positions itself is essential for maximizing recovery, whether you are a seller, a lender, or a competing buyer.

The stalking horse bidder occupies a unique and powerful position. According to established practice, the stalking horse sets the floor bid and receives protections including breakup fees of 1 to 3% (up to 4% in complex cases) and expense reimbursement. The minimum overbid is structured to account for these protections so the estate nets equivalent value. For buyers, becoming the stalking horse provides exclusive access to management, data rooms, and negotiating leverage before the open auction. For sellers and lenders, a well-chosen stalking horse signals market credibility and attracts additional bidders.

Credit bidding is the other major strategic tool available to secured creditors. Under Section 363(k), secured creditors may credit bid up to the full face value of their allowed secured claim, effectively using debt as currency in the auction. Private equity firms frequently use loan-to-own strategies, purchasing distressed debt at a discount and then credit bidding the full face value to acquire assets at below-market cost. However, this strategy carries risks, including potential equitable subordination if the court finds the creditor acted in bad faith.

Key strategic considerations for each participant type:

- Secured lenders: Evaluate credit bid rights early and assess whether the asset value supports a credit bid strategy or whether a cash sale to a third party maximizes recovery.

- Private equity buyers: Determine whether to enter as a stalking horse (with protections) or as a competing bidder (with more flexibility but less information access).

- Strategic acquirers: Focus on qualifying early, conducting thorough due diligence, and positioning bids to address non-price terms that may be decisive.

- Distressed debt funds: Analyze the debt trading price relative to asset value to determine whether loan-to-own is viable and whether equitable subordination risk is manageable.

Pro Tip: Negotiating bid increments and auction procedures before the court approves them is far more effective than objecting afterward. Competing bidders who engage early in the procedures process can shape the rules in ways that favor their participation. Reviewing auction strategies for maximizing recovery provides additional tactical frameworks applicable to complex situations. For lenders managing special assets, the principles behind industrial plant liquidation for lenders directly inform how credit bid strategies should be structured.

| Bidder type | Primary advantage | Key risk |

|---|---|---|

| Stalking horse | Protections, information access | Overbid exposure |

| Credit bidder | Debt-as-currency, no cash outlay | Equitable subordination |

| Strategic acquirer | Synergy value, operational insight | Diligence timeline pressure |

| Financial buyer | Flexibility, speed | Less information than stalking horse |

Nuances and risks: Legal pitfalls and special scenarios

Strategic participation in bankruptcy auctions requires more than understanding the standard process. The legal landscape contains several gray areas that can affect both buyers and sellers in material ways.

Insider dynamics receive heightened judicial scrutiny. When a debtor’s management or existing equity sponsors participate as bidders, courts examine bid protections more carefully and will not grant superpriority administrative expense status to breakup fees in insider transactions. This scrutiny can complicate management buyout scenarios and requires careful structuring.

The free-and-clear protections under Section 363(f) are powerful but not absolute. As courts have addressed in the Chrysler and GM cases, product liability successor claims may survive a free-and-clear sale order if post-sale accidents occur or if notice to potential claimants was inadequate. Buyers of manufacturing assets, consumer product companies, or any business with product liability exposure must conduct thorough diligence on this risk.

“Free-and-clear title under Section 363(f) is not an unconditional guarantee. Buyers who assume all product liability risk has been extinguished without independent legal analysis are taking on exposure that may not appear until years after closing.”

Additional nuances and risks to monitor include:

- Breakup fee sizing: Fees must benefit the estate under the O’Brien test. Fees that are too large chill competition and may be disallowed by the court, leaving the stalking horse without its negotiated protection.

- Late bids: Courts occasionally consider late bids, particularly when the late bid is materially higher and the auction has not yet been confirmed. Buyers and sellers should understand that the process is not always final until the gavel falls and the court approves.

- Successor liability for environmental claims: Environmental liabilities may survive a 363 sale in certain jurisdictions, requiring specific representations and indemnities in the purchase agreement.

- Credit bid challenges: Courts have the authority to limit credit bids for cause, which can disrupt a lender’s loan-to-own strategy at a late stage.

Understanding real estate auction dynamics in the context of bankruptcy adds another layer of complexity, particularly when real property with environmental history is included in the asset package.

Benchmarks and outcomes: Recovery rates and process efficiency

Data on bankruptcy auction outcomes provides critical context for setting realistic expectations and evaluating whether a 363 sale is the right path for a given situation.

Empirical research on insolvency outcomes shows EU gross recovery rates averaging approximately 42% (net 38%), with an average time to recovery of 4.2 years across all insolvency processes. Higher debt concentration before bankruptcy correlates with faster processes and higher class-level recoveries. Post-363 performance of acquired businesses often lags sector benchmarks, which is a critical consideration for strategic buyers evaluating synergy assumptions.

Key factors that drive higher recovery in bankruptcy auctions:

- Pre-auction marketing reach: Broader buyer outreach consistently produces more competitive bidding and higher final prices.

- Asset mix and condition: Well-maintained, operational assets with clear title history attract more qualified bidders.

- Debt concentration: Simpler capital structures with fewer secured creditor classes tend to produce cleaner, faster auctions.

- Stalking horse quality: A credible, well-capitalized stalking horse signals asset quality and attracts competing bids.

- Marketing timeline: Longer, more aggressive pre-auction marketing periods produce better outcomes than compressed timelines.

As Mayer Brown’s analysis of 363 sales confirms, these auctions are faster and more efficient than reorganization plans but involve public competitive processes versus private sales. They are preferred for clean title transfer despite the inherent bid risk. For industrial assets specifically, understanding why equipment auctions outperform alternatives reinforces the case for a structured auction approach over private negotiated sales in most distressed scenarios.

Why the real lever in bankruptcy auctions is the pre-auction strategy

Most professionals focus on auction day tactics: bid increments, stalking horse protections, and credit bid calculations. These matter. But in our experience managing complex bankruptcy auctions across industrial, real estate, and commercial asset classes, the outcome is largely determined before the first bid is ever submitted.

Information asymmetry is the most underappreciated factor in bankruptcy auction results. Buyers who conduct thorough prepetition due diligence, build relationships with management, and understand the asset’s operational history arrive at the auction with a materially different valuation than buyers who rely solely on the data room. This asymmetry consistently translates into pricing confidence and willingness to bid aggressively at the margin.

The most common mistake we observe is waiting too long to begin marketing. Debtors and their advisors sometimes delay outreach until after court approval of bidding procedures, compressing the buyer qualification timeline and reducing the competitive field. A narrower field means less competitive tension and lower final recovery. Aggressive pre-filing marketing, when legally permissible, changes the outcome.

Ignoring the strategic buyer universe is another costly error. Financial buyers are visible and predictable. Strategic acquirers, including competitors, suppliers, and customers of the debtor, often assign higher value to specific assets because of operational synergies that financial buyers cannot capture. Reaching this audience requires targeted industry outreach, not generic marketing.

The most successful bankruptcy auction outcomes we have observed share a common thread: the debtor’s team treated the auction as the final step in a structured liquidation plan, not as a substitute for one. Pre-auction preparation, including auction readiness best practices, asset documentation, environmental clearance, and targeted buyer outreach, consistently produces results that exceed expectations set by distressed asset stereotypes.

Maximize asset recovery with proven bankruptcy auction experts

If you are managing a distressed asset situation and evaluating whether a bankruptcy auction is the right path, the quality of your marketing and liquidation partner will materially affect your outcome.

Maas Companies brings decades of experience managing complex bankruptcy auctions across industrial plants, manufacturing equipment, real estate, and commercial properties worldwide. From pre-filing marketing strategy through closing and title transfer, our team provides the aggressive, targeted outreach that drives competitive bidding and maximizes recovery for lenders, PE firms, and corporate clients. Explore our full range of auction and liquidation services to see how we approach each engagement. If you have assets to move, connect with our team directly through our asset selling platform and let us build a recovery strategy around your specific situation.

Frequently asked questions

What is a Section 363 sale in bankruptcy?

A Section 363 sale is a court-supervised auction process where a debtor sells assets outside ordinary business operations to maximize value for creditors, typically producing clean title transfer and a competitive bidding environment.

Who can participate in a bankruptcy auction?

Any qualified bidder, including secured creditors, private equity firms, and outside buyers, can participate subject to court-approved procedures. Secured creditors may credit bid under Section 363(k), while private equity firms often use loan-to-own strategies to acquire assets efficiently.

How long does a typical bankruptcy auction process take?

Most processes conclude in 45 to 90 days from the bidding procedures motion to closing, making bankruptcy auctions one of the faster options for distressed asset liquidation compared to full reorganization plans.

Are assets in bankruptcy auctions sold with clear title?

Generally yes, but successor product liability claims may survive a free-and-clear sale order for post-sale incidents or when notice to potential claimants was inadequate, requiring buyers to conduct independent legal analysis.

What are the main risks for buyers or sellers in bankruptcy auctions?

Key risks include heightened scrutiny for insider bids, potential successor liability for product and environmental claims, and the possibility that late bids or legal objections may delay or complicate closing.

Recommended

- Auction strategies for small businesses: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- Maximize Asset Recovery: Top Real Estate Liquidation Methods | Blog | Insights on Asset Liquidation and Auction Trends

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Real Estate Auction Blog | Tips, Strategies & Insights

- Bankruptcy Appraisals in New Jersey | Certified Home Values – NJREAG