Blog

Orderly liquidation: Maximize asset recovery and stability

TL;DR:

- Orderly liquidation is a structured sale process that maximizes asset recovery within a planned timeframe.

- Professional appraisals and targeted marketing are essential to achieving higher recovery rates in manufacturing liquidations.

- Following best practices like early engagement, asset staging, and buyer education improves outcomes significantly.

When private equity firms and manufacturing executives hear the word “liquidation,” the instinctive reaction is often one of dread, conjuring images of deeply discounted assets sold in chaos under time pressure. That assumption is both common and costly. Orderly liquidation is a structured, strategically managed process that operates on a fundamentally different basis than a distressed fire sale, and the distinction directly determines how much value you recover from manufacturing assets. This article clarifies what orderly liquidation means, how it works in practice, and what decision-makers must prioritize to achieve maximum recovery during restructuring events.

Table of Contents

- Defining orderly liquidation: What it means and why it matters

- The mechanics of orderly liquidation: Step-by-step process

- Valuing assets in orderly liquidation: OLV, FMV, and more

- Orderly liquidation in manufacturing: Best practices and critical factors

- The real value: What most leaders overlook when liquidating assets

- Optimize your recovery: Experts in orderly liquidation for manufacturing

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Orderly beats forced sale | Structured liquidation avoids panic-driven discounts, enabling higher asset recovery through preparation and marketing. |

| OLV drives decision-making | Accurate OLV calculation helps guide pricing, negotiation, and recovery expectations during restructure. |

| Appraisals are essential | Professional appraisals establish benchmarks, defend value, and maximize returns for manufacturing assets. |

| Best practices improve outcomes | Careful planning, timing, and asset preparation directly affect liquidation success rates. |

| Partner expertise matters | Engaging liquidation experts and brokerages unlocks structured recovery solutions for distressed manufacturing assets. |

Defining orderly liquidation: What it means and why it matters

Having introduced the misconception around liquidation, let’s clarify exactly what orderly liquidation is, and why its structured approach makes a meaningful difference in real-world asset recovery scenarios.

Orderly liquidation is a managed sale process in which assets are marketed and sold within a reasonable, predetermined timeframe, typically ranging from a few weeks to several months. Unlike a forced sale driven by an immediate court order or creditor pressure, an orderly process allows for preparation, targeted marketing, and buyer qualification. This structured timeline is what separates recoverable value from avoidable loss.

At the center of this approach is a key benchmark: Orderly Liquidation Value, or OLV, which is the estimated gross proceeds from an asset sale positioned between Fair Market Value (FMV) and Forced Liquidation Value (FLV). In formula terms, OLV = Market Value minus Business Liabilities, representing net proceeds available after obligations. This metric gives lenders, restructuring advisors, and PE firms a defensible estimate of what a structured sale will yield before the process begins.

The contrast between orderly and forced liquidation is significant, and decision-makers should understand both positions clearly before committing to a path:

| Factor | Orderly liquidation | Forced liquidation |

|---|---|---|

| Timeframe | Weeks to months | Days to hours |

| Marketing exposure | Broad, targeted buyer pool | Limited, reactive |

| Asset preparation | Full staging and documentation | Minimal or none |

| Recovery rate | Higher (near OLV) | Lower (near FLV) |

| Buyer pool | Qualified, industry-specific | General auction crowd |

| Risk of value loss | Moderate and manageable | High |

Avoiding fire sale dynamics is not just about timing. It is about knowledge management, buyer access, and marketing execution. Forced sales from urgency or panic create illiquidity and destroy institutional knowledge embedded in specialized equipment, process lines, and facility configurations. Orderly processes preserve that knowledge and translate it into recoverable financial value.

The practical implications for manufacturing portfolios are direct. A structured approach to plant liquidation strategies enables selling specialized equipment to qualified buyers who understand its value, rather than accepting bids from general asset buyers who will discount heavily for unfamiliarity. Understanding what liquidation sales explained in full operational context can help leadership teams align expectations before engaging the market.

“The difference between orderly and forced liquidation is not just procedural. It is the difference between realizing asset value and surrendering it under pressure.”

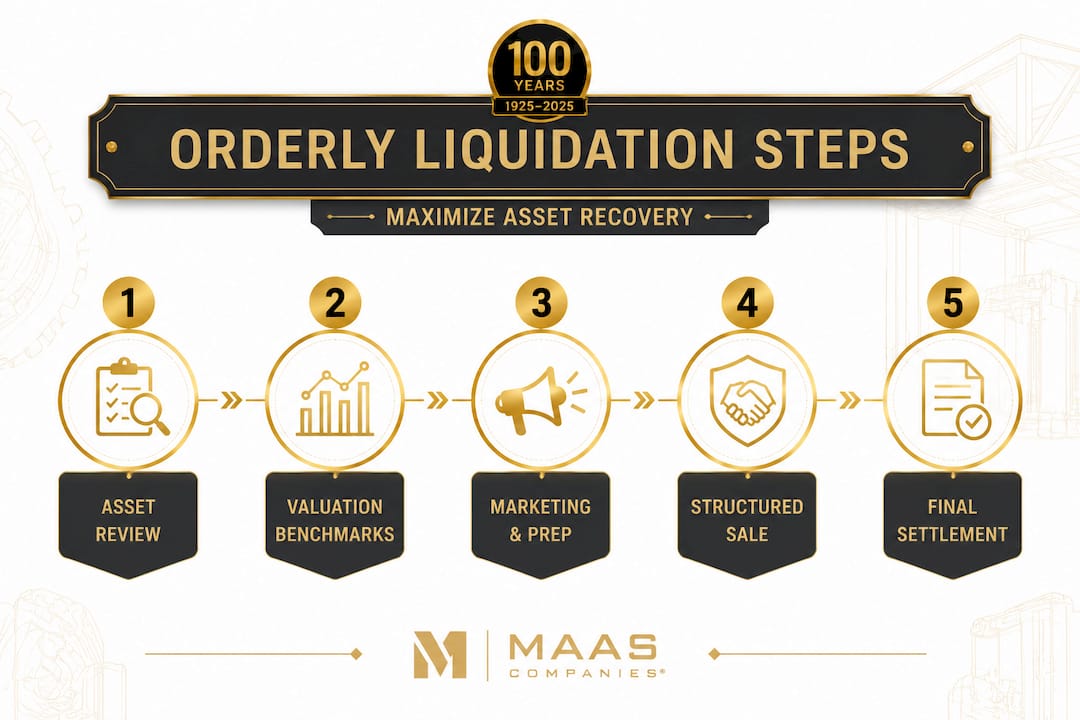

The mechanics of orderly liquidation: Step-by-step process

Now that we have defined orderly liquidation and compared it to other methods, let’s examine how a structured approach is put into action, from asset review to final sale.

An orderly liquidation follows a deliberate sequence. Each stage builds on the previous one, and skipping steps creates compounding losses. Here is how the process unfolds in a manufacturing context:

- Asset inventory and documentation. The first step is a full physical and financial inventory of all assets, including machinery, tooling, inventory, real estate, and intangible assets. Accurate documentation supports defensible valuations and reduces buyer risk perceptions.

- Professional appraisal. Independent appraisers assess OLV, FMV, and FLV for each asset category. This establishes the pricing floor and guides the marketing strategy that follows.

- Marketing preparation and asset staging. Equipment is cleaned, photographed, and organized. Technical specifications, maintenance records, and operational histories are compiled. This directly impacts buyer willingness to pay and reduces due diligence time.

- Targeted buyer outreach. Experienced liquidation firms leverage industry networks, proprietary buyer databases, and digital marketing channels to reach qualified buyers who will pay for value rather than discount for unknowns.

- Auction or negotiated sale execution. Depending on asset type and market conditions, either a live or online auction, or a negotiated private sale, is executed. The format is chosen based on the asset mix and timeline constraints.

- Removal, logistics, and title transfer. Post-sale logistics are coordinated, including asset removal, rigging, transportation arrangements, and clean title documentation.

- Final accounting and disbursement. Net proceeds are calculated after deducting costs such as brokerage fees, removal expenses, and legal costs (Net Orderly Liquidation Value, or NOLV), and distributions are made to stakeholders.

In-place versus removed sale scenarios demonstrate that orderly liquidation consistently yields higher recoveries than forced liquidation due to marketing time, with in-place sales achieving a 10-20% premium over removal-basis valuations. Assets sold while still installed and operational command higher prices because buyers can verify function, assess integration complexity, and reduce their own risk. Facility liquidation strategies should account for this premium and prioritize in-place sales wherever feasible.

Liquidation timing is also a significant variable. Seasonal market conditions, industry cycles, and capital availability among potential buyers all influence the achievable recovery rate. Aligning your sale timeline with peak buyer activity in the relevant manufacturing sector can meaningfully improve outcomes.

Pro Tip: For complex manufacturing facilities with mixed asset types, consider running parallel sale tracks. Offer the full plant as a going concern first, then segment into process lines, then individual equipment lots. This staged approach captures buyers at multiple value levels and maximizes total recovery without leaving money on the table.

Consulting low-volume manufacturing insights can also inform decisions about specialized equipment that may have strong residual value with niche buyers, even when the broader facility sale is straightforward.

Valuing assets in orderly liquidation: OLV, FMV, and more

With the process understood, it is essential to examine how assets are valued and what benchmarks determine success in an orderly liquidation.

Three primary benchmarks drive asset valuation decisions in a liquidation context:

- Fair Market Value (FMV): The price a willing buyer pays a willing seller, with neither under compulsion and both having reasonable knowledge of the facts. FMV is the theoretical ceiling.

- Orderly Liquidation Value (OLV): An estimated amount that an asset would realize in a structured sale within a reasonable timeframe. OLV falls between FMV and FLV, reflecting the conditions of a managed but time-bounded process.

- Forced Liquidation Value (FLV): The amount that an asset would realize at an immediate, unrestricted auction. FLV is the floor and represents the worst-case scenario for most manufacturing assets.

- Net Orderly Liquidation Value (NOLV): OLV minus all costs of sale, including brokerage, removal and transport, legal fees, and administrative costs.

The gap between these benchmarks can be substantial. Empirical data illustrates the stakes clearly. IBC resolution data shows that resolution plans recover 162% of liquidation value, while EU net recovery rates for orderly processes average approximately 38% compared to significantly lower rates for forced scenarios, and historical bank liquidation data reflects net recoveries near 75% in well-managed structured sales.

| Valuation benchmark | Definition | Typical recovery relative to FMV |

|---|---|---|

| FMV | No compulsion, full market exposure | 100% (baseline) |

| OLV | Structured sale, reasonable timeframe | 70-85% |

| NOLV | OLV minus sale costs | 55-75% |

| FLV | Immediate forced auction | 40-60% |

Professional appraisals are not a formality. They are a strategic investment. An expert asset review establishes the benchmarks that guide negotiation floors, sets reserve prices for auctions, and provides defensible documentation for stakeholders, lenders, and legal counsel. The absence of a professional appraisal typically results in underpricing assets or failing to identify high-value lots that warrant separate marketing treatment.

Equipment liquidation for CFOs and finance leads must include a clear valuation strategy from day one. Engaging industrial liquidation experts early ensures that the appraisal methodology aligns with the asset mix, the intended sale format, and the timeline constraints of the restructuring event.

Pro Tip: Request that appraisers provide both OLV and NOLV estimates for each major asset category. The delta between these two figures reveals the true cost of sale execution and allows for more accurate cash flow planning during the restructuring process.

Orderly liquidation in manufacturing: Best practices and critical factors

Now, let’s bring these principles into practical focus. What specific steps and factors should manufacturing leaders and private equity decision-makers prioritize when facing an orderly liquidation?

The following best practices are grounded in documented outcomes and the operational realities of industrial asset recovery:

- Start the process early. Every week of additional marketing time translates into broader buyer exposure and more competitive bidding. Delaying engagement with a liquidation partner compresses timelines unnecessarily and pushes recoveries toward FLV rather than OLV.

- Segment assets by buyer type. Specialized process equipment attracts different buyers than general-purpose machinery. Tailored marketing campaigns that speak to the technical specifications of each asset category consistently outperform generic lot listings.

- Maintain assets during the sale process. Equipment that remains operational, or at minimum functional, commands meaningfully higher prices. Shutting down maintenance prematurely is one of the most common and avoidable value-destroyers in manufacturing liquidations.

- Control the narrative. Structured liquidations benefit from proactive communication with vendors, employees, and community stakeholders. Uncontrolled information flow can damage buyer confidence and reduce competitive tension at auction.

- Document chain of control. Proper asset titles, maintenance records, and regulatory compliance documentation reduce buyer risk perceptions and support higher bid levels.

- Use competitive sale formats. Online auctions with extended bidding windows and live event options maximize competitive tension and buyer participation for high-value equipment.

Resolution plans versus liquidation data consistently shows that structured approaches recover 35-45% of claims compared to only 5-10% for traditional unmanaged liquidations, with liquidation averaging 89% of its stated liquidation value but at a lower absolute dollar figure. This gap underscores why maximizing plant recovery through professional management is not optional for PE firms and lenders with significant exposure.

Real estate liquidation methods should also be integrated into the broader asset disposal strategy when manufacturing facilities include owned real property. Coordinating equipment and real estate timelines prevents conflicts and ensures that site access for equipment removal does not undermine the property sale timeline.

An orderly negotiated sale example from the construction contractor sector illustrates how surplus inventory and equipment can be handled through a combination of private negotiations and structured marketing, achieving results that a standalone auction would not have generated.

Pro Tip: Asset staging matters more than most firms expect. Investing resources in cleaning, organizing, and presenting equipment professionally before buyer inspections can increase realized prices by 5-15%. First impressions at a site walkthrough or in online photographs directly influence how much a qualified buyer will commit.

The real value: What most leaders overlook when liquidating assets

Having covered the operational details and best practices, there is a strategic dimension that most decision-makers consistently undervalue, and it is worth addressing directly.

The most common mistake in manufacturing liquidations is not choosing the wrong sale format. It is skipping the professional appraisal because it appears to be an unnecessary cost during a cash-constrained restructuring event. This calculation is backwards. The appraisal fee is almost always recovered many times over through the pricing discipline and buyer confidence it creates. Without a defensible benchmark, reserve prices are set by intuition, negotiations lack credibility, and buyers sense weakness.

IBC empirical data showing that orderly processes outperform forced sales by significant margins does not happen automatically. Those results are achieved by firms that invest in preparation, marketing, and professional guidance rather than cutting corners to save upfront costs that are trivial relative to the asset values at stake.

There are additional overlooked drivers of recovery value that most restructuring teams fail to address until it is too late:

- Buyer education materials. Technical documentation, process flow diagrams, and operating manuals provided to prospective buyers remove uncertainty and justify higher bids.

- Utility and service connections. Coordinating with facility management to keep power, compressed air, and other services active during buyer inspections allows for live demonstrations that dramatically increase buyer confidence.

- Coordination with remaining workforce. Former operators and maintenance personnel who can answer technical questions from buyers during site visits add measurable credibility and value to the sale process.

- International marketing reach. Many specialized manufacturing assets command the highest prices from buyers outside the domestic market. Firms with global buyer networks consistently outperform those limited to local or regional outreach.

The expert guidance for asset reviews available from experienced liquidation professionals addresses each of these factors systematically, which is why the difference between a professionally managed orderly liquidation and a self-managed sale can represent millions of dollars in recovered value for large manufacturing portfolios.

Optimize your recovery: Experts in orderly liquidation for manufacturing

If you are ready to apply these principles and optimize your asset recovery, here is how specialized partners can guide your structured liquidation efforts.

Maas Companies Inc. brings decades of experience in marketing and selling industrial plants, manufacturing equipment, real estate, and commercial properties on an international scale. Our approach combines aggressive, multi-channel marketing with deep industry expertise to maximize competitive tension and recovery rates for every asset category. Whether your situation calls for a live auction, an online bidding event, a negotiated private sale, or a combination approach, our team builds the strategy around your assets and timeline. If you are ready to sell industrial equipment or explore structured liquidation options, our full services portfolio outlines how we support manufacturing firms, PE sponsors, and lenders through every stage of the asset disposition process.

Frequently asked questions

How is orderly liquidation different from a forced sale?

Orderly liquidation leverages preparation and marketing time to avoid discounts, reaching qualified buyers who recognize and pay for asset value, rather than accepting the first offer under time pressure.

What factors determine orderly liquidation value (OLV)?

OLV equals market value minus business liabilities, adjusted for marketing time, asset condition, and cost deductions including brokerage, removal, and legal fees.

What kind of recovery rates can be expected from orderly liquidation?

Structured processes typically achieve a 10-20% premium over forced liquidation, with resolution benchmarks showing 35-45% recovery of claims compared to 5-10% for traditional unmanaged liquidations.

Why are appraisals so important in orderly liquidation?

Professional appraisals establish defensible benchmarks that set credible reserve prices, support lender reporting, and guide strategic pricing decisions that maximize recovery across all asset valuation benchmarks.

Can orderly liquidation work for specialized assets and equipment?

Yes. Orderly liquidation processes are specifically well-suited to specialized manufacturing assets because the extended marketing timeline allows experts to identify and qualify niche buyers who understand the equipment’s value and will pay accordingly.

Recommended

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- How Industrial Plant Liquidation Maximizes Recovery Value for Lenders | Blog | Insights on Asset Liquidation and Auction Trends

- Equipment liquidation explained: maximizing asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Plant liquidation strategies: maximize recovery in 2026 | Blog | Insights on Asset Liquidation and Auction Trends

- Understanding wine liquidation: How collectors maximise value