Blog

Structured liquidation guide: maximize recovery for manufacturing assets

TL;DR:

- Structured liquidation maximizes asset recovery through coordinated legal, operational, and stakeholder management.

- Court-supervised Section 363 sales and credit bids are key mechanisms for efficient manufacturing asset disposition.

- Early risk identification and stakeholder alignment are essential for achieving optimal recovery outcomes.

When a manufacturing facility enters financial distress, every day without a structured exit plan accelerates value erosion. Equipment depreciates, carrying costs accumulate, and unsecured creditors grow impatient. Private equity firms and corporate decision-makers who attempt informal or piecemeal liquidation routinely leave 20 to 40 percent of recoverable value on the table. A structured approach, built on proper legal frameworks, coordinated stakeholder management, and disciplined execution, consistently produces better outcomes across asset classes ranging from precision machinery to industrial real estate.

Table of Contents

- What you need to get started with structured liquidation

- Step-by-step execution: the structured liquidation process

- Addressing edge cases and special risks

- Measuring success: recovery outcomes and post-sale steps

- The uncomfortable truth most guides miss about structured liquidation

- Need help maximizing asset recovery? Partner with experts.

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Early preparation is key | Gathering the right team and documents up front prevents costly surprises during structured liquidation. |

| Section 363 sales maximize value | Using Section 363 asset sales reduces liability and attracts more bidders compared to traditional methods. |

| Mitigate special risks | Address environmental, labor, and supplier risks proactively to avoid last-minute deal failures. |

| Monitor recovery benchmarks | Track liquidation results against industry standards and adjust strategies for future deals. |

| Expert support improves outcomes | Leveraging specialized advisors and auction partners often increases net recovery for industrial sellers. |

What you need to get started with structured liquidation

Structured liquidation is not simply selling off equipment. It is a coordinated legal and operational process designed to extract maximum value from distressed assets while managing creditor claims, regulatory obligations, and buyer due diligence simultaneously. Section 363 sales in Chapter 11 bankruptcy allow buyers, including private equity, to acquire assets free and clear of liens through court-supervised auctions, making them the dominant mechanism for maximizing recovery value in complex manufacturing situations.

Before any sale process begins, the following stakeholders must be identified and engaged:

- Legal counsel specializing in bankruptcy and commercial transactions

- Financial advisors capable of preparing creditor waterfall analyses and bid procedures

- Operations managers who can maintain equipment in marketable condition during the sale period

- Environmental consultants to assess remediation exposure and compliance status

- Union representatives where collective bargaining agreements are in place

- Third-party appraisers for independent asset valuations

Documentation readiness is equally critical. Asset registers must be current and verified against physical inventory. Lien searches on all major equipment and real property should be completed before marketing begins. Site access protocols, union contracts, and any equipment lease agreements need to be reviewed for assignment restrictions.

| Resource or tool | Purpose | Third-party support needed? |

|---|---|---|

| Asset register and appraisal | Establishes baseline valuation for bidding | Yes, independent appraiser |

| Lien and UCC search | Identifies encumbrances on assets | Yes, title/legal firm |

| Environmental site assessment | Quantifies remediation risk | Yes, environmental consultant |

| Bid procedures motion | Sets auction rules and timelines | Yes, bankruptcy counsel |

| Marketing and buyer outreach | Generates competitive interest | Yes, industrial marketing firm |

Reviewing ESG workflow considerations early is increasingly important, as institutional buyers now conduct environmental and social due diligence as a standard step before submitting bids.

Pro Tip: Engage lenders and debtors-in-possession as early as possible. Early conversations often reveal whether a Section 363 sale is viable before formal bankruptcy filing, which can compress timelines and reduce administrative costs. Review equipment liquidation strategies to understand how asset-specific planning affects overall recovery.

Step-by-step execution: the structured liquidation process

With preparation complete, execute your plan step by step for maximum asset recovery.

- Conduct independent asset valuation. Commission orderly liquidation value and fair market value appraisals for all major equipment, real property, and intangibles. These figures anchor bid procedures and protect against undervaluation claims.

- Select the sale method. Choose between a court-supervised auction, a negotiated stalking horse sale, or a combination. Stalking horse bids establish a price floor and attract competing offers.

- File legal motions and provide required notices. Bankruptcy counsel files bid procedure motions, sale motions, and cure notices for assumed contracts. Creditors, unions, and regulatory agencies receive statutory notice periods.

- Run the marketing and sales process. Distribute offering memoranda, conduct site tours, manage buyer due diligence, and collect qualified bids by the court-approved deadline.

- Hold the auction and select the winning bid. The court-supervised auction produces a final buyer. Credit bidding by secured lenders is permitted and frequently determines the outcome.

- Close and transfer assets. Execute the asset purchase agreement, release liens, transfer titles, and complete any required regulatory filings.

Asset sale vs. stock sale: key differences

| Factor | Asset sale (Section 363) | Stock sale |

|---|---|---|

| Liability isolation | Strong: buyer takes selected assets only | Weak: buyer inherits all liabilities |

| Recovery speed | Faster with court approval | Slower due to broader due diligence |

| Lien treatment | Assets sold free and clear | Liens remain with entity |

| Buyer preference | High for distressed situations | Lower when liabilities are uncertain |

| Tax treatment | Asset step-up available | Carryover basis applies |

Credit bidding deserves specific attention. When a secured lender holds a $100 million claim against a distressed manufacturer, it can submit that debt as a bid rather than cash. Centre Lane’s $100M credit bid for Hardinge Inc. and the $69 million Worldwide Machinery sale illustrate how private equity uses this mechanism to acquire precision manufacturing assets with minimal cash outlay. For sellers, understanding that credit bids set a competitive floor is essential to structuring bid procedures that still attract cash buyers.

Pro Tip: Prefer asset deals over stock deals in distressed manufacturing situations. Asset purchases allow buyers to isolate specific equipment and real property while leaving environmental or pension liabilities with the estate. Review plant liquidation strategies and choosing the right auction format before finalizing your sale method.

“The auction format you select shapes every downstream outcome. Stalking horse arrangements protect floor value; open auctions maximize competitive tension. Neither works without aggressive pre-auction marketing.”

Addressing edge cases and special risks

Even with strong execution, unaddressed edge cases can threaten asset recovery. The following risks appear most frequently in manufacturing liquidations and require proactive management:

- Environmental remediation costs. Contaminated soil, underground storage tanks, or hazardous material storage can generate liabilities that exceed equipment value at some facilities. Buyers will discount bids aggressively or walk away entirely if remediation scope is undefined.

- Union contracts and WARN Act compliance. The federal WARN Act requires 60-day advance notice before mass layoffs or plant closures affecting 50 or more employees. Failure to comply creates wage and benefit claims that become administrative expenses in bankruptcy, reducing creditor recoveries.

- Supplier anti-assignment clauses. Many manufacturing supply agreements prohibit assignment without vendor consent. Buyers acquiring production lines that depend on proprietary supply relationships may find those contracts unenforceable post-sale.

- Successor liability exposure. Courts in some jurisdictions impose product liability, warranty, or pension obligations on asset buyers if the transaction is structured as a de facto merger. Holdbacks and indemnification provisions in the purchase agreement are the primary mitigation tools.

Monitoring environmental monitoring technology at the facility during the sale period helps document baseline conditions, which protects both sellers and buyers from post-closing disputes over contamination scope.

“Risks like remediation and successor liability often derail well-planned sales when missed early.”

Court requirements add another layer of complexity. Sale motions must identify all executory contracts the buyer intends to assume, along with cure amounts for any defaults. Government agencies, including the EPA and state environmental regulators, may have notification rights or approval authority before certain assets transfer. Engaging specialized legal and facility transition strategies expertise early prevents last-minute delays that inflate carrying costs and erode buyer confidence.

Seasonal liquidation challenges also affect timing decisions. Heavy equipment auctions held in winter months in northern states often attract fewer bidders, which directly reduces competitive tension and final sale prices.

Measuring success: recovery outcomes and post-sale steps

Following execution and risk control, it’s time to verify performance and wrap up the process.

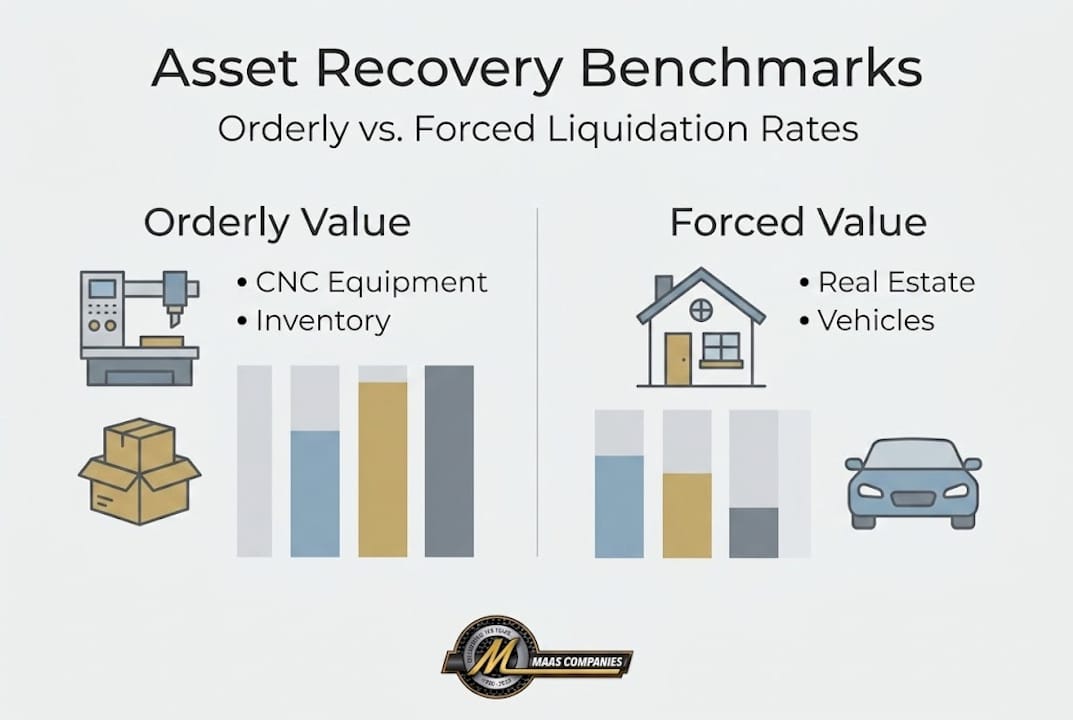

Typical recovery benchmarks by asset class

| Asset class | Orderly liquidation value (% of book) | Forced liquidation value (% of book) |

|---|---|---|

| CNC and precision machinery | 40 to 65% | 20 to 35% |

| General manufacturing equipment | 25 to 50% | 10 to 25% |

| Industrial real estate | 55 to 80% | 35 to 60% |

| Raw material inventory | 30 to 60% | 15 to 30% |

| Intellectual property and patents | Highly variable | Highly variable |

Resolution plans yield 35 to 45% recovery compared to liquidation’s 5 to 10% in the most distressed scenarios. This gap reinforces why liquidation should be treated as a fallback when resolution efforts fail, not a first choice. When no qualified bidders emerge or sale delays extend beyond 90 days, liquidation becomes the only viable path to creditor recovery.

Post-sale obligations are often underestimated. A complete post-sale checklist includes:

- Financial reconciliation: Verify that all bid deposits, closing adjustments, and cure payments are correctly applied against creditor claims.

- Lien releases: Confirm that UCC termination statements and mortgage releases are filed promptly after closing.

- Environmental compliance: Complete any required site assessments, remediation commitments, or regulatory filings tied to the transfer of industrial property.

- Records management: Transfer or archive all equipment maintenance records, environmental permits, and compliance documentation as required by the purchase agreement.

- Employee notifications: Confirm WARN Act compliance documentation is complete and filed.

Reviewing a surplus equipment sale guide and real estate liquidation methods after closing helps decision-makers benchmark their results against comparable transactions and identify process improvements for future situations. Applying best inventory management practices during the wind-down period also reduces shrinkage and preserves recoverable value on remaining stock.

The uncomfortable truth most guides miss about structured liquidation

Most guides focus on process steps and legal mechanics. What they rarely address is why firms that follow every step still achieve below-average recoveries. The answer almost always comes down to timing, stakeholder alignment, and pre-auction preparation quality.

Private equity firms that outperform in distressed manufacturing acquisitions do not simply follow the Section 363 playbook. They identify distress signals 6 to 12 months before a formal filing and begin building relationships with lenders and management teams early. This positions them to serve as stalking horse bidders, which gives them data advantages and negotiating leverage that late-arriving bidders cannot replicate.

On the sell side, too many firms underestimate indirect risks. Environmental liability is consistently underpriced in initial valuations, which creates buyer surprises during due diligence and triggers bid reductions or withdrawals. Overconfidence in auction timing is equally damaging. Sellers who delay marketing to wait for a “better” market often face accelerating carrying costs and deteriorating equipment condition that more than offset any price improvement.

The other overlooked factor is post-auction communication. Buyers who feel unsupported after winning a bid are slower to close, more likely to renegotiate, and less likely to refer future opportunities. Building a structured post-sale communication window into every transaction improves close rates and protects final recovery figures.

Advanced plant strategies that incorporate pre-marketing due diligence, aggressive buyer outreach, and defined post-sale review periods consistently outperform those that treat liquidation as a purely legal exercise.

Pro Tip: Schedule a formal post-sale review within 30 days of closing. Document what worked, what caused delays, and where recovery fell short of projections. This institutional knowledge directly improves outcomes on the next transaction.

Need help maximizing asset recovery? Partner with experts.

Structured liquidation in manufacturing requires more than legal knowledge. It demands coordinated marketing, buyer network access, and operational expertise that most internal teams cannot provide under distressed timelines.

Maas Companies brings decades of experience marketing industrial plants, equipment, and commercial real estate to qualified buyers worldwide. Our approach combines aggressive advertising with deep industry relationships to generate competitive interest and maximize final recovery. Whether you are managing a single facility wind-down or a multi-site portfolio disposition, our team is ready to support every stage of the process. Visit our sell industrial equipment page to start a conversation, explore our full range of Maas services, or review our current auction projects to see active transactions in progress.

Frequently asked questions

What is a Section 363 sale and why is it preferred in manufacturing asset liquidation?

Section 363 sales allow assets to be sold free and clear of liens through court-supervised auctions, making them the preferred mechanism for protecting buyers from inherited liabilities while maximizing creditor recovery in bankruptcy.

How does credit bidding benefit private equity buyers in a structured liquidation?

Credit bidding allows private equity buyers to use their existing debt claims as bid currency, which means they can acquire distressed assets without deploying equivalent cash and often outcompete buyers who must finance acquisitions externally.

What are typical recovery rates for structured liquidation compared to resolution plans?

Resolution plans yield 35 to 45% recovery on average versus 5 to 10% in pure liquidation scenarios, so liquidation is best treated as a fallback when no viable buyers or resolution paths exist.

What special risks should industrial sellers watch for in a structured liquidation?

Environmental remediation costs, union contract obligations, supplier anti-assignment clauses, and successor liability exposure are the four risks most likely to reduce final recovery or derail a sale if not identified and addressed before marketing begins.

Recommended

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Plant liquidation strategies: maximize recovery in 2026 | Blog | Insights on Asset Liquidation and Auction Trends

- Equipment liquidation explained: maximizing asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Maximize Asset Recovery: Top Real Estate Liquidation Methods | Blog | Insights on Asset Liquidation and Auction Trends