Blog

Why Third-Party Auctions Maximize Asset Value and Cut Risk

TL;DR:

- Auction-first distressed asset dispositions outperform traditional negotiated sales by achieving higher net proceeds and significantly reducing inventory time. Engaging qualified third-party auctioneers early ensures standardized, defensible processes that protect all stakeholders and maximize asset recovery. Delaying such engagement often results in erosion of value and higher overall costs, emphasizing the importance of prompt action in distressed asset management.

Private equity managers and lenders handling distressed assets frequently assume that a carefully negotiated traditional sale will generate the best possible return. That assumption carries real financial consequences. Auction-first distressed dispositions have been reported to achieve materially better net-proceeds outcomes than traditional REO dispositions, challenging the conventional playbook and prompting financial decision-makers to take a harder look at what competitive auction mechanisms actually deliver.

Table of Contents

- The case for auctions: Why traditional sales fall short

- How third-party auctions standardize and de-risk the process

- Balancing speed with value: What experts actually recommend

- Applying the auction advantage: When and how to engage third parties

- The uncomfortable truth: Why most firms wait too long to call the experts

- Unlock your asset value with the right auction partner

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Auctions outperform traditional sales | Competitive auction processes deliver higher net proceeds and reduce sale timelines compared to negotiated deals. |

| Standardization lowers execution risk | Third-party management introduces structure and transparency, minimizing litigation and process disputes. |

| Early engagement maximizes value | Bringing in auction professionals early helps strike the right balance between sale speed and asset value. |

| Defensible outcomes for stakeholders | Court-reviewed auction procedures protect against challenges and support credible, fair sales. |

The case for auctions: Why traditional sales fall short

The performance gap between traditional negotiated sales and third-party auction processes is not a matter of opinion. It shows up in measurable outcomes: net proceeds, days in inventory, carrying costs, and stakeholder exposure. Understanding that gap is the first step toward making better disposition decisions for industrial assets, real estate, and commercial properties.

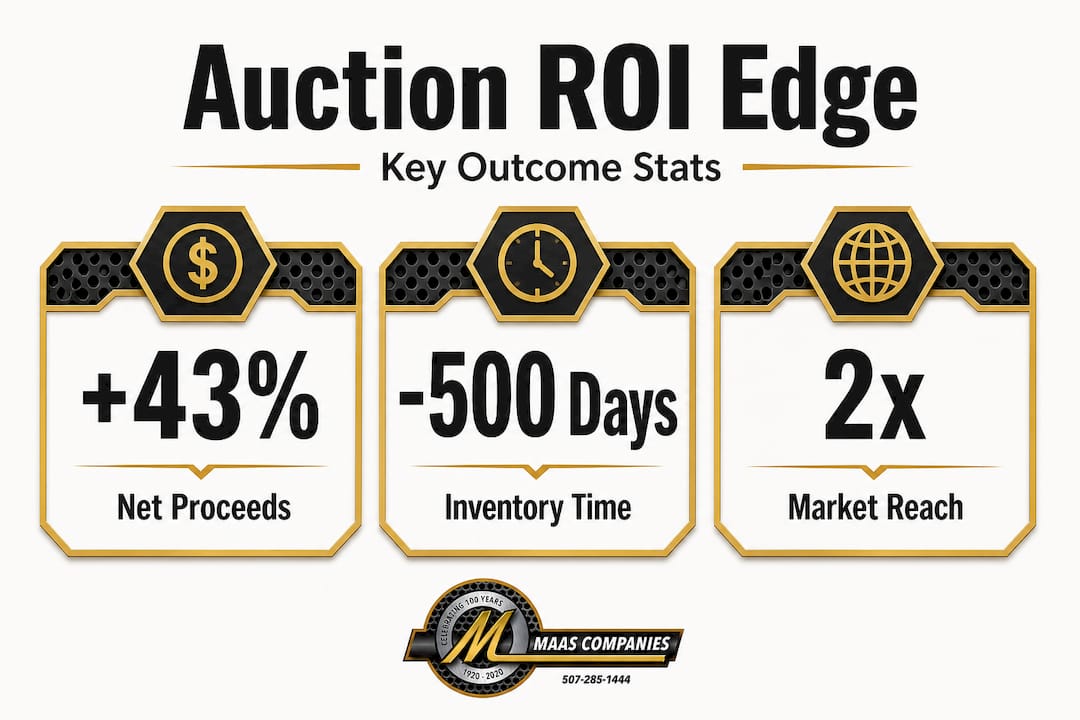

Auction-first distressed asset processes achieve a 43-point net proceeds advantage and reduce inventory days by over 500 compared to traditional real estate owned (REO) methods. That is not a marginal improvement. A 500-day reduction in inventory time eliminates enormous carrying costs, including taxes, insurance, maintenance, security, and opportunity costs on capital that remains trapped in non-performing assets. For a lender managing a portfolio of distressed manufacturing facilities, those costs compound quickly.

Performance comparison: Traditional sales vs. third-party auctions

| Metric | Traditional negotiated sale | Third-party auction |

|---|---|---|

| Net proceeds advantage | Baseline | Up to 43 percentage points higher |

| Average inventory days | 500+ days longer | Significantly reduced |

| Bidder pool | Limited, relationship-driven | Broad, open, competitive |

| Price discovery | Opaque, subject to negotiation | Transparent, market-driven |

| Stakeholder defensibility | Often contested | Standardized, auditable |

| Execution risk | Higher (deal-by-deal) | Lower (process-driven) |

Reviewing this comparison makes it clear why leading financial institutions increasingly favor auctions for asset recovery when speed and certainty matter. The structured nature of a competitive auction creates price discovery through market participation, not through back-channel negotiation between a small number of known parties.

“Auction-first dispositions achieve net proceeds advantages of 43 percentage points and reduce inventory days by over 500 compared to traditional REO methods, demonstrating that competitive processes consistently outperform negotiated sales in distressed scenarios.”

The core drawbacks of traditional sale methods in distressed asset contexts include:

- Extended timelines that inflate carrying costs and erode asset value before a transaction closes

- Narrow buyer pools that limit competitive pressure and favor buyers who recognize they have limited competition

- Price opacity that makes it difficult for lenders, creditors, and courts to validate that the sale represents fair market value

- Execution uncertainty because negotiated deals can fall through late in the process without the competitive backstop an auction provides

- Suboptimal capital recovery that reduces distributions to creditors and lenders, sometimes triggering legal disputes about whether the disposition was properly managed

When assets are industrial in nature, such as manufacturing equipment, process plants, or specialized machinery, the risk of a narrow buyer pool is especially acute. Effective manufacturing process optimization strategies can make equipment more valuable before a sale, but even optimized assets require a broad, qualified buyer pool to realize their true market value.

How third-party auctions standardize and de-risk the process

Now that we’ve seen the hard numbers, let’s examine what makes third-party auctions uniquely effective and defensible. The involvement of a qualified third-party auctioneer does far more than simply run a bidding event. It introduces institutional structure that protects all parties and withstands scrutiny from courts, creditors, and regulatory bodies.

Third-party involvement supports auction methodology including bid procedures, qualified bidder rules, notice requirements, and court scrutiny in bankruptcy-style auctions. That methodology standardizes the process and meaningfully reduces execution risk. In practice, this means that every step from marketing to closing follows a documented, enforceable protocol that any stakeholder can review and challenge if warranted.

In-house process vs. third-party managed auction

| Process element | In-house disposition | Third-party managed auction |

|---|---|---|

| Marketing reach | Internal contacts, local networks | National and international qualified buyer pools |

| Bid procedures | Informal, inconsistently applied | Standardized, legally defensible |

| Qualified bidder vetting | Varies, often inconsistent | Structured qualification criteria |

| Notice requirements | May be inadequate | Meets or exceeds legal standards |

| Creditor and court defensibility | Frequently challenged | Auditable process, minimal dispute |

| Conflict of interest exposure | High, especially with insider bids | Neutralized by independent oversight |

The third-party auctioneer value extends directly into stakeholder protection. When a lender or private equity firm is disposing of a distressed industrial plant, creditors and co-investors want assurance that the process was fair. An independent auctioneer provides that assurance because their role is defined by process neutrality, not by a relationship with either buyer or seller.

For streamlining manufacturing asset dispositions, the structured approach also reduces the internal burden on the asset holder’s own staff. Rather than managing buyer inquiries, negotiating terms, and coordinating legal reviews internally, the team focuses on oversight while the auctioneer manages execution. That division of responsibility preserves internal resources and reduces errors.

Pro Tip: When preparing for a distressed asset auction, engage your legal counsel early to review bid procedures and qualified bidder standards before the auctioneer begins marketing. Standardized procedures established upfront significantly reduce the probability of court challenges or creditor objections after the sale closes.

Balancing speed with value: What experts actually recommend

Understanding process mechanics makes the tradeoffs clear, but what do experts actually advise in challenging, distressed scenarios? The tension between speed and value is real. Waiting too long to act on a distressed asset allows deterioration, carrying costs, and market shifts to erode net proceeds. But moving too quickly without adequate competitive exposure risks leaving money on the table or producing a sale result that courts or creditors reject as insufficiently competitive.

Expert guidance on distressed sales emphasizes that process design must balance speed to avoid value erosion with competitiveness and credibility. Third-party auctioneers and receivers are specifically equipped to manage this tradeoff so that the sale remains defensible to courts and creditors. That balance is not achieved through intuition but through structured auction timelines that allow enough marketing exposure to attract qualified bidders while maintaining a firm closing schedule.

“Process design must balance speed (to avoid value erosion) with competitiveness and credibility. Third-party auctioneers and receivers help manage this tradeoff so the sale remains defensible to courts and creditors while maximizing competitive pressure.”

The practical steps for speeding up asset disposition without sacrificing competitive outcomes follow a clear sequence:

- Conduct an asset assessment early. Identify all assets, their condition, and their market value range before engaging any buyer or auctioneer. This baseline drives appropriate process design.

- Engage a qualified third-party auctioneer. Select a firm with demonstrable experience in the specific asset category, whether that is industrial equipment, commercial real estate, or specialized process plants.

- Establish bid procedures and timelines upfront. Define minimum bid increments, qualified bidder criteria, deposit requirements, and closing timelines before marketing begins.

- Execute an aggressive, multi-channel marketing campaign. Reach registered buyers, industry contacts, institutional investors, and international markets simultaneously to maximize bidder pool depth.

- Run a transparent, competitive bidding event. Whether live, online, or hybrid, the process must be observable and verifiable by all stakeholders.

- Close under documented protocols. Every step from accepted bid to transfer of title should follow written procedures that support post-closing review.

Each of these steps reinforces the credibility of the sale outcome. A well-documented process protects lenders from legal liability, satisfies creditor committees, and ensures that the price achieved reflects genuine market demand rather than a constrained negotiation.

Applying the auction advantage: When and how to engage third parties

With an understanding of the balance and clear expert recommendations, let’s turn to practical guidance on how to leverage third-party auctions effectively. Not every asset disposal situation calls for the same approach, but there are reliable signals that indicate when a third-party auction is clearly the superior path.

Key signals that a third-party auction is the right choice:

- The asset is distressed or the entity is in financial difficulty. Receiverships, bankruptcies, and workout situations require independent, defensible processes.

- Multiple stakeholders have competing interests. When lenders, equity holders, creditors, and regulatory bodies all have a stake in the outcome, an independent auctioneer neutralizes conflict.

- The asset is specialized or industrial in nature. Equipment, plants, and commercial properties require buyer pools that extend beyond local real estate brokers or equipment dealers.

- Carrying costs are mounting. Every month an asset remains unsold represents direct cash cost. Auction timelines enforce certainty.

- Prior marketing efforts have stalled. If a traditional listing or brokerage process has not generated qualified offers, a competitive auction resets market exposure.

- Regulatory or court oversight is involved. Standardized auction procedures meet the evidentiary and procedural standards courts require.

The Section 363 sale process in bankruptcy is one of the clearest examples where third-party auctioneer involvement is not optional but expected. The methodology it requires, including formal bid procedures, qualified bidder standards, and notice requirements, mirrors the practices that experienced auction firms apply in any high-stakes industrial disposition.

A step-by-step evaluation for decision-makers considering this path begins with an honest internal assessment of whether in-house resources can manage the process with the speed and defensibility the situation requires. If the answer is uncertain, that uncertainty itself is a signal to engage outside expertise immediately.

Pro Tip: Early engagement of a third-party auctioneer, ideally at or before the decision to liquidate, consistently produces higher proceeds than engaging one as a last resort. Early involvement allows the auctioneer to participate in asset assessment, marketing strategy, and process design from the beginning, which directly improves outcomes compared to a rushed, reactive engagement.

Reviewing a surplus equipment sale guide can help decision-makers understand the specific preparation steps that make an auction successful, particularly for manufacturing and industrial assets where condition documentation, technical specifications, and operational history all influence buyer willingness and bid levels.

The uncomfortable truth: Why most firms wait too long to call the experts

Ultimately, the most overlooked factor in asset dispositions is not process but timing. Here is what actually happens in most situations: the asset holder spends weeks or months attempting internal solutions, pursuing informal buyer conversations, or waiting for market conditions to improve. By the time a third-party auctioneer is engaged, value has already eroded.

The delay is rarely deliberate. It is driven by a combination of factors. Internal teams believe they understand the asset’s value and can achieve it without outside help. Leadership is reluctant to absorb the fees associated with professional auction services without first exhausting cheaper alternatives. And, frankly, engaging an auctioneer signals to stakeholders that internal options have been exhausted, which some executives find uncomfortable to acknowledge.

But the numbers are unambiguous. A facility or equipment portfolio that could have been marketed aggressively in month one begins accumulating carrying costs, physical deterioration, and buyer perception problems by month three or four. Buyers who are aware that an asset has been on the market for an extended period will adjust their bids downward to account for seller desperation and unknown deterioration. The market is not forgiving of visible delay.

We have seen situations where clients engaged external auction expertise six months after they should have, losing proceeds that far exceeded what professional auction fees would have cost. The lesson is straightforward: the cost of late engagement is almost always higher than the cost of early engagement. Firms that treat auction services as a last resort systematically underperform compared to those that treat them as a first-choice tool in distressed or surplus disposition scenarios.

The discipline required is not complicated. Establish an internal trigger for when third-party auction expertise is engaged, such as when a distressed asset has been held for more than 60 days without a qualified buyer, or when an asset is formally classified as non-performing. Then follow it. For decision-makers focused on maximizing asset recovery across a portfolio, consistent process is more valuable than case-by-case judgment calls that are vulnerable to optimism bias.

Unlock your asset value with the right auction partner

If the evidence presented here aligns with challenges your firm is managing right now, whether that is a distressed industrial facility, surplus manufacturing equipment, or a commercial property portfolio that needs efficient disposition, the next step is a direct conversation with an experienced auction and marketing partner.

Maas Companies brings decades of experience marketing industrial plants, equipment, real estate, and commercial properties to qualified buyer pools worldwide. Our aggressive advertising and marketing approach, combined with structured auction methodologies, is designed to maximize net proceeds while protecting stakeholders throughout the process. To explore current opportunities or discuss how our services apply to your specific situation, visit our sell industrial equipment page or review our full auction services portfolio to see the range of asset types and markets we serve.

Frequently asked questions

What makes third-party auctions more effective for asset liquidation?

Third-party auctions use standardized bid procedures, qualified bidder rules, and transparent notice requirements that attract a broad pool of competitive buyers, which reduces execution risk and consistently drives higher net proceeds than informal negotiated processes.

How do auctions compare to negotiated sales for distressed assets?

Auctions significantly outperform traditional negotiated sales in distressed scenarios, with auction-first dispositions achieving net proceeds advantages of over 40 percentage points and reducing inventory time by more than 500 days compared to traditional REO methods.

When should a company consider a third-party auctioneer?

A third-party auctioneer should be engaged early, ideally at the point when a distressed or surplus asset is first identified, since early involvement in marketing and process design consistently produces higher proceeds than a reactive, last-resort engagement for large, specialized, or distressed assets.

What risks do third-party auctions help avoid?

Third-party auctions minimize execution risk, reduce the probability of creditor and court challenges by following defensible standardized procedures, and ensure the final price reflects genuine competitive market demand rather than a constrained negotiation outcome.

Recommended

- Top reasons to buy at auction: maximize value & cut risk | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- How to Navigate Commercial Property Foreclosure Sales | Blog | Insights on Asset Liquidation and Auction Trends