Blog

Why Use Structured Bidding to Maximize Asset Recovery

TL;DR:

- Structured bidding establishes a formal, auditable process that enhances asset recovery through genuine competition and standardized evaluation criteria. It produces comprehensive records, such as submission timestamps and evaluation worksheets, to defend award decisions against audits or legal challenges. Overall, it mitigates risks of unfavorable outcomes caused by informal, unstructured negotiations lacking transparency and documentation.

When asset values are on the line, the process you use to solicit bids matters as much as the assets themselves. Many executives assume bidding is simply a mechanism for driving prices down. That misunderstanding is costly. Understanding why use structured bidding means recognizing it as a compliance framework, a competitive tool, and an audit defense system simultaneously. This article gives corporate executives and financial professionals a practical look at how structured bidding works, what it protects, and why informal alternatives introduce risks that regularly undermine recovery outcomes.

Table of Contents

- Key takeaways

- Why use structured bidding: the foundational case

- Competitive advantage and risk mitigation in asset recovery

- Compliance and documentation controls that protect your process

- Structured bidding strategies in financial and investment contexts

- Implementing structured bidding best practices

- My perspective on why this process cannot be informal

- How Maascompanies supports structured asset liquidations

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Structured bidding is not just about price | It standardizes evaluation criteria, enforces fairness, and creates a defensible record for every procurement decision. |

| Audit trails are non-negotiable | Submission timestamps, addenda acknowledgments, and bid-opening documentation are the operational backbone of any compliant process. |

| Competitive tension drives recovery value | Multiple qualified bidders, evaluated objectively, produce better prices and surface risks before contract execution. |

| Financial bidding requires specialized analysis | Investment product bids must incorporate after-tax, regulatory, and option-cost factors, not just headline yield comparisons. |

| Technology strengthens defensibility | Electronic bid management with secure controls reduces protest exposure and produces cleaner audit documentation than manual systems. |

Why use structured bidding: the foundational case

Structured bidding is a formal procurement method that standardizes how solicitation documents are prepared, how bids are received, and how evaluation decisions are made. Its core purpose is not to guarantee the lowest price. It is to produce a documented, defensible record that can withstand regulatory scrutiny, legal challenge, and internal audit review.

The three core drivers of structured bidding are price transparency, objective vendor comparison, and risk mitigation through the surfacing of vendor capabilities and limitations. Each driver serves a different organizational need, but together they form a process architecture that informal bidding simply cannot replicate.

The benefits of structured bidding are especially visible in asset recovery and liquidation contexts. When a plant closure or restructuring event requires rapid disposition of high-value equipment, the organization needs a process that attracts multiple serious buyers, treats all parties equally, and produces a record that justifies the final award decision.

Key components that define a structured bidding framework include:

- Predefined solicitation documents with consistent scope descriptions distributed identically to all qualified bidders

- Standardized evaluation criteria established before bid receipt, not after, to prevent retroactive scoring adjustments

- Formal bid receipt controls that log submission times and maintain confidentiality until the official opening

- Documented award rationale linking evaluation scores directly to the final selection decision

Pro Tip: Establish your evaluation scoring matrix before the solicitation period opens. Any criteria introduced after bids are received will expose the process to challenge and may invalidate the award.

Linkage to regulatory and compliance frameworks is what separates structured bidding from a commercial negotiation. The process steps, including needs identification, solicitation, bid receipt, evaluation, and award, follow a sequence that mirrors public procurement standards and holds up to the same level of scrutiny.

Competitive advantage and risk mitigation in asset recovery

The competitive advantage of structured bidding is not theoretical. When multiple qualified parties submit bids under identical conditions, their responses reveal real market pricing, vendor capacity, and risk tolerance. That information is operationally valuable beyond the immediate transaction.

“Competitive bidding is fundamentally about accountability and fairness, packaging scope and evaluation criteria into formal documents for defendable decisions.” (legalclarity.org)

Consider what happens when an executive bypasses this process during a plant liquidation. A single buyer, even one known to the organization, negotiates from an information advantage. There is no competitive tension. There is no external validation of asset pricing. The outcome may seem acceptable, but there is no way to prove it was optimal.

The advantages of structured bidding in asset recovery include:

- Maximized recovery pricing through genuine competition among pre-qualified buyers, each submitting independent valuations

- Objective vendor comparison enabling the selling organization to evaluate total consideration, not just headline bid price, against consistent scope documents

- Pre-contract risk identification where vendor responses reveal logistical constraints, removal timelines, and financing contingencies before any commitment is made

- Reduced favoritism exposure because decisions are anchored to documented criteria rather than relationship factors

One practical example: a manufacturing firm disposing of excess industrial equipment through a formal sealed-bid process routinely receives 15 to 30 percent higher realized values than comparable equipment sold through direct negotiation. The competitive process forces buyers to price aggressively rather than anchor to a starting negotiation position.

Risk identification before contract execution is an often-overlooked benefit. When structured bidding requires bidders to confirm scope, identify removal requirements, and acknowledge asset condition, it surfaces issues that would otherwise emerge as post-award disputes. That pre-screening function protects the selling organization’s timeline and carrying costs.

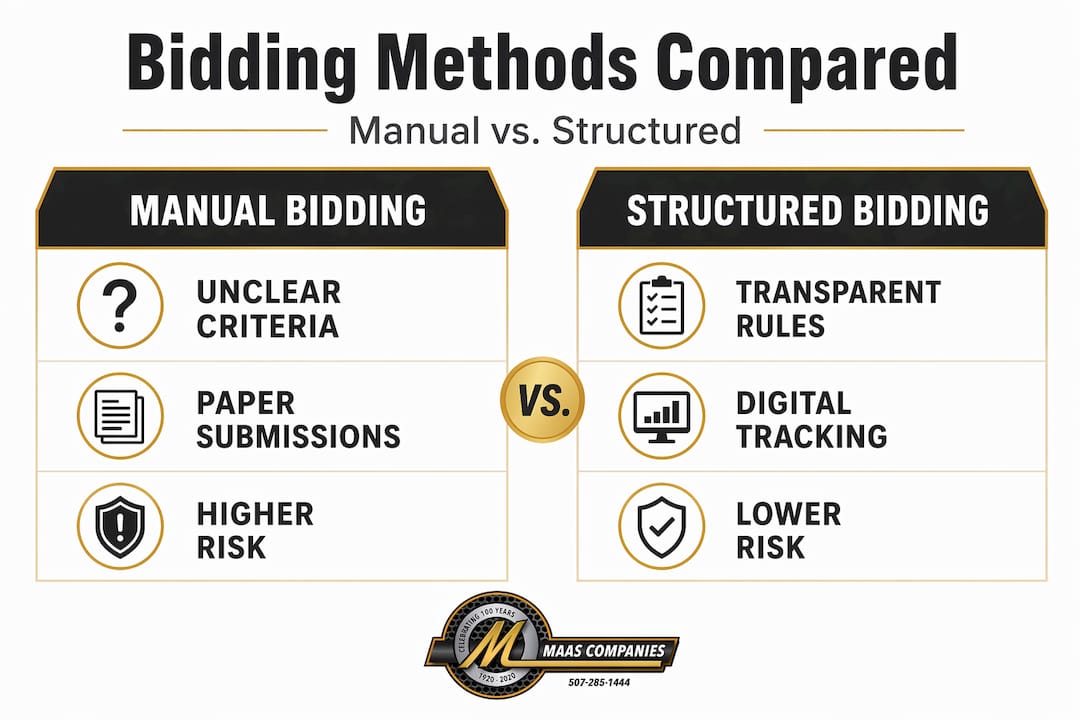

Compliance and documentation controls that protect your process

The compliance architecture of structured bidding is where most organizations either succeed or fail under audit. Sealed bid compliance ensures bid confidentiality until official opening, equal treatment of all bidders, and a process record that can be reproduced on demand.

The operational proof points that define a defensible sealed-bid process are specific and sequential:

- Solicitation distribution records confirming all bidders received identical documents at the same time

- Submission timestamps showing each bid arrived within the acceptance window and was not accessed before opening

- Addenda acknowledgments from every bidder confirming receipt of any clarifications or scope modifications issued during the bid period

- Bid-opening documentation recording who was present, what was received, and the precise prices and conditions of each submission

- Evaluation worksheets with pre-assigned scorer identities and completed scoring prior to any internal discussion of results

The following table contrasts manual versus electronic bid management across the dimensions that matter most to compliance officers and auditors.

| Control dimension | Manual bid management | Electronic bid management |

|---|---|---|

| Submission timestamp integrity | Requires witnessed receipt log | System-generated, tamper-evident |

| Confidentiality before opening | Depends on physical security | Cryptographic lockout until opening time |

| Addenda distribution proof | Certified mail or email receipts | Automated acknowledgment tracking |

| Audit trail completeness | Manual assembly, prone to gaps | Full event log with user actions |

| Protest defensibility | Moderate, dependent on staff records | High, with court-admissible system logs |

Manual bid submissions without secure controls make it significantly harder to prove fairness and expose organizations to protests and audits. Electronic platforms resolve most of these vulnerabilities by automating the control system rather than relying on procedural discipline.

Pro Tip: Treat bid addenda as a formal amendment process. Every clarification issued to any bidder must go to all bidders simultaneously, with written acknowledgment collected before the bid deadline. An uneven information distribution, even unintentional, is the most common cause of post-award protests.

Controlled Q&A with uniform bidder access is not optional. Informal clarifications undermine fairness and create protest exposure that can delay or invalidate an award. That delay has direct carrying cost implications in asset liquidation scenarios.

Structured bidding strategies in financial and investment contexts

The advantages of structured bidding extend beyond physical asset procurement into investment product selection, where regulatory and tax compliance requirements make the process considerably more complex. Financial institutions and public entities use structured competitive bid processes to ensure that investment product selection is defensible to regulators, not just financially rational.

The table below outlines how evaluation criteria differ between standard asset recovery bidding and structured investment product bidding.

| Evaluation dimension | Asset recovery bidding | Investment product bidding |

|---|---|---|

| Primary criterion | Net recovery proceeds | After-tax, after-option-cost yield |

| Regulatory compliance factor | Procurement rules and state statute | Arbitrage rebate compliance, IRS regulations |

| Risk assessment | Buyer qualification and removal logistics | Credit quality, embedded option costs, liquidity |

| Expertise required | Asset valuation and logistics | Financial modeling, tax law, regulatory frameworks |

| Defensibility standard | Procurement audit | Regulatory examination, arbitrage audit |

Firms that use structured investment bidding incorporate tax and regulatory expertise alongside arbitrage rebate models to compare investment alternatives, including option costs. A bid that shows an attractive headline yield may carry embedded option costs that make it economically inferior to a lower-yielding alternative once the full cost structure is modeled.

This is why evaluating after-tax and option-cost impacts is non-negotiable in regulated investment procurement. Structured product bid comparisons must integrate complex financial models reflecting option-related costs to prevent misleading yield appearances. Organizations without the internal expertise to build these models need specialized advisors who can run the comparison correctly before the bid deadline.

The structured bidding strategies appropriate for investment contexts share one critical characteristic with physical asset bidding: the process must be documented well enough to defend every selection decision under examination, whether that examination comes from an internal audit, a regulatory review, or a legal challenge.

Implementing structured bidding best practices

Applying structured bidding best practices within your organization requires discipline at three stages: before the solicitation opens, during the bid period, and after award. Each stage has specific controls that determine whether the process will hold up to scrutiny.

Before the solicitation opens, the most critical task is bid qualification. A bid/no-bid scorecard disciplines resources and improves compliance by filtering opportunities through threshold scoring on compliance readiness, delivery risk, and probability of a successful outcome. For the selling organization, a parallel qualification screen applied to prospective bidders before invitation prevents unqualified parties from diluting the process.

During the bid period, vendor communication controls are the highest-risk area. Best practices include:

- Centralized question intake through a single designated contact, with all responses compiled and issued as formal addenda to the full bidder list

- Blackout periods prohibiting any substantive communication with bidders during the final days before submission to prevent last-minute informational advantages

- Consistent scope access so that site visits, if required, are offered on identical terms to all qualified bidders rather than accommodating individual scheduling preferences

- Documented decision log capturing every communication event, even requests that were declined, to demonstrate process integrity

After award, the documentation package should be assembled immediately while event memory is fresh. The package must include the original solicitation, all addenda, all received bids, evaluation worksheets, and the written award rationale. This package is the organization’s primary defense in any post-award challenge.

Pro Tip: For sealed bid sales of industrial and commercial assets, consider engaging a professional auction and marketing firm to manage solicitation distribution, bid receipt, and opening procedures. Third-party process management adds a layer of independence that strengthens the defensibility of the outcome.

Technology selection matters. Electronic bid management platforms that provide court-admissible audit logs, cryptographic submission controls, and automated addenda tracking eliminate the most common failure points in manual processes. The initial setup investment is substantially smaller than the cost of a single contested award.

My perspective on why this process cannot be informal

In my experience working with organizations managing high-value asset dispositions, the single most costly mistake is treating the bidding process as an administrative formality rather than a strategic control system. Executives who authorize informal processes, whether out of time pressure, vendor familiarity, or bureaucratic fatigue, routinely discover the consequences during post-transaction audits or legal challenges, not before.

I have seen organizations achieve strong headline recovery figures through informal direct negotiations, only to face regulatory findings that the process lacked documentation sufficient to prove competitive pricing. The result is clawback exposure, audit findings, or in public-sector contexts, contract nullification. The recovery figure becomes irrelevant when the process cannot be defended.

What I find most overlooked is the communication audit trail. Executives understand the importance of the bid-opening record. They rarely give equal attention to addenda timing and acknowledgment or to the record of what information was shared with which bidder and when. Those gaps are where audits find fault.

The balance between transparency and strategic negotiation is real, but it is not achieved by reducing process formality. It is achieved by designing a process with the right stages, competitive rounds, and evaluation criteria from the outset. Structured bidding, done correctly, gives you both the competitive outcome and the defensible record.

— Vector

How Maascompanies supports structured asset liquidations

Maascompanies has managed structured bidding and competitive marketing campaigns for industrial plants, oilseed processing facilities, grain handling operations, and surplus equipment portfolios across international markets. The firm’s process combines aggressive buyer solicitation with rigorous documentation controls, producing both competitive recovery values and audit-ready process records.

Organizations currently managing plant closures, financial restructuring, or excess inventory disposition can review a current example of Maascompanies’ structured bidding execution through the biodiesel plant auction project, which covers a 3-MGY facility, oilseed processing equipment, grain handling assets, and retail fuel stations. For organizations ready to explore recovery options, the sell industrial equipment page outlines how Maascompanies structures the engagement from initial valuation through final award.

FAQ

What is structured bidding?

Structured bidding is a formal procurement process that standardizes solicitation documents, evaluation criteria, and bid receipt controls to produce fair, transparent, and defensible award decisions. It applies to both physical asset dispositions and investment product procurement.

How does structured bidding improve asset recovery?

Structured bidding drives higher recovery values by creating genuine competitive tension among multiple qualified buyers evaluated against identical criteria, preventing any single party from negotiating from a one-sided information advantage.

What records are required for sealed-bid compliance?

Key compliance records include submission timestamps, addenda acknowledgments from all bidders, bid-opening documentation, and a written award rationale tied to pre-established evaluation criteria.

Why does structured bidding matter in financial investment contexts?

Structured investment bidding requires evaluating bids on after-tax yield, embedded option costs, and regulatory compliance factors, not just headline returns, making specialized financial modeling non-negotiable for defensible selection decisions.

What is the biggest risk of informal bidding processes?

Informal processes lack the documentation necessary to defend award decisions under audit or legal challenge, exposing organizations to clawback liability, regulatory findings, or contract nullification even when the final price appeared competitive.

Recommended

- Auction strategies for small businesses: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Maximize Asset Recovery: Top Real Estate Liquidation Methods | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends