Blog

How Auction Escrow Streamlines Distressed Asset Sales

TL;DR:

- Auction escrow introduces a neutral, legally governed mechanism that secures commitments, accelerates closings, and mitigates default risks in distressed asset sales. It involves a third-party holding funds or assets until sale conditions are met, ensuring trust between buyers and sellers across various legal frameworks like bankruptcy and foreclosures. Proper structuring of escrow, early planning, and understanding legal complexities maximize transaction certainty and value in distressed industrial asset auctions.

Many private equity firms and corporate decision-makers assume that competitive bidding alone creates enough accountability in distressed asset auctions. That assumption is costly. Without a properly structured escrow arrangement, even a winning bid can unravel, leaving sellers exposed to default risk and buyers questioning whether their deposits are protected. Auction escrow resolves these vulnerabilities by introducing a neutral, legally governed mechanism that secures commitments from all parties, accelerates closing timelines, and provides the chain of control that high-value industrial asset transactions demand.

Table of Contents

- What is auction escrow?

- How auction escrow works in distressed asset auctions

- Auction escrow frameworks: Comparison of major processes

- Challenges, edge cases, and practical risks in auction escrow

- Maximizing value and certainty with auction escrow: Best practices

- Auction escrow: What most decision-makers miss

- Explore efficient industrial auctions with trusted escrow solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Auction escrow ensures trust | Escrow secures bidder performance and payments, protecting all parties in complex distressed asset auctions. |

| Good faith deposits are standard | Qualified bidders must submit 5-10% deposits, held in escrow, to prove seriousness and financial readiness. |

| Frameworks vary by sale type | Section 363, UCC foreclosures, and secured party sales each have distinct escrow rules and procedures. |

| Know your risks and edge cases | Be aware of deposit forfeitures, credit bidding, and court controls to avoid costly mistakes. |

| Best practices drive results | Preparation, qualified escrow agents, and clarity on procedures maximize value and certainty in liquidation. |

What is auction escrow?

Auction escrow is a financial arrangement in which a neutral third party holds funds or assets on behalf of both buyer and seller until all conditions of the sale are satisfied. In distressed asset contexts, this takes on added importance because sellers are often operating under court supervision, creditor pressure, or compressed timelines that leave little room for failed transactions.

Auction escrow refers to the use of escrow arrangements in auction processes, particularly for securing bidder commitments through good faith deposits in distressed asset auctions like Section 363 bankruptcy sales or secured party sales.

The core function of escrow in these transactions is to resolve trust issues that naturally arise between parties who may have no prior relationship and competing financial interests. Sellers need assurance that the winning bidder can actually close. Buyers need assurance that their deposit is protected if the seller fails to deliver clear title or satisfy legal conditions.

Auction escrow applies across several distinct legal contexts, each with its own rules and risk profile:

- Section 363 bankruptcy sales: Court-supervised auctions where a debtor sells assets free and clear of liens, subject to bankruptcy court approval

- UCC Article 9 foreclosure sales: A secured creditor disposes of collateral after a debtor default, with escrow used to secure bidder commitments and manage proceeds

- Secured party sales: Similar to UCC foreclosures, but often conducted as private sales with escrow providing accountability in the absence of court oversight

- Government surplus and regulatory liquidations: Auctions where regulatory compliance requirements make neutral escrow handling essential

Understanding the legal context is the first step. Firms that apply auction absentee bidding strategies without first confirming escrow terms often expose themselves to complications when the sale closes. Equally, sellers who want to focus on speeding up asset disposition benefit directly from escrow’s ability to prevent last-minute bidder withdrawals that force costly re-auctions.

How auction escrow works in distressed asset auctions

The mechanics of auction escrow follow a predictable sequence, though the specific terms vary depending on asset type, legal framework, and the parties involved. Here is a step-by-step breakdown of how escrow functions in a standard distressed asset auction:

- Bidder qualification: Before a bidder can participate, they must demonstrate financial capability. This typically involves submitting proof of financing and signing confidentiality agreements. The escrow arrangement begins here, establishing clear expectations before the bidding starts.

- Good faith deposit submission: Qualified bidders submit a good faith deposit of 5% to 10% of their bid amount, held in escrow to demonstrate seriousness and financial capability. This deposit is non-negotiable in most Section 363 processes and is designed to filter out unqualified or speculative bidders.

- Auction execution: Bidding proceeds under the terms established in the court-approved bid procedures. The escrow agent holds all deposits throughout this phase, releasing unsuccessful bidders’ funds promptly after the auction closes.

- Sale approval and closing: For bankruptcy auctions, the court must approve the sale before the transaction can close. Escrow holds the winning bidder’s deposit during this period, which can range from days to several weeks depending on objections or competing interests.

- Post-closing holdbacks: Escrow holdbacks of 10% to 15% of the purchase price are used to secure indemnities and working capital adjustments in business acquisitions following auctions. These holdbacks protect both parties against post-closing claims, environmental liabilities, or inventory discrepancies discovered after the sale.

- Final release: Once all conditions are satisfied and the holdback period expires, remaining funds are released to the seller according to the escrow agreement.

Pro Tip: When structuring a distressed auction, specify the escrow agent, deposit amount, release conditions, and dispute resolution process in the bid procedures document before the auction goes public. Ambiguity at this stage creates disputes after the gavel falls.

Real estate auction liquidation follows a nearly identical sequence, though the holdback terms and title insurance requirements often differ from pure equipment sales. Firms that understand how brokerage and auction work together gain a significant advantage in structuring escrow arrangements that protect recovery without adding unnecessary closing friction.

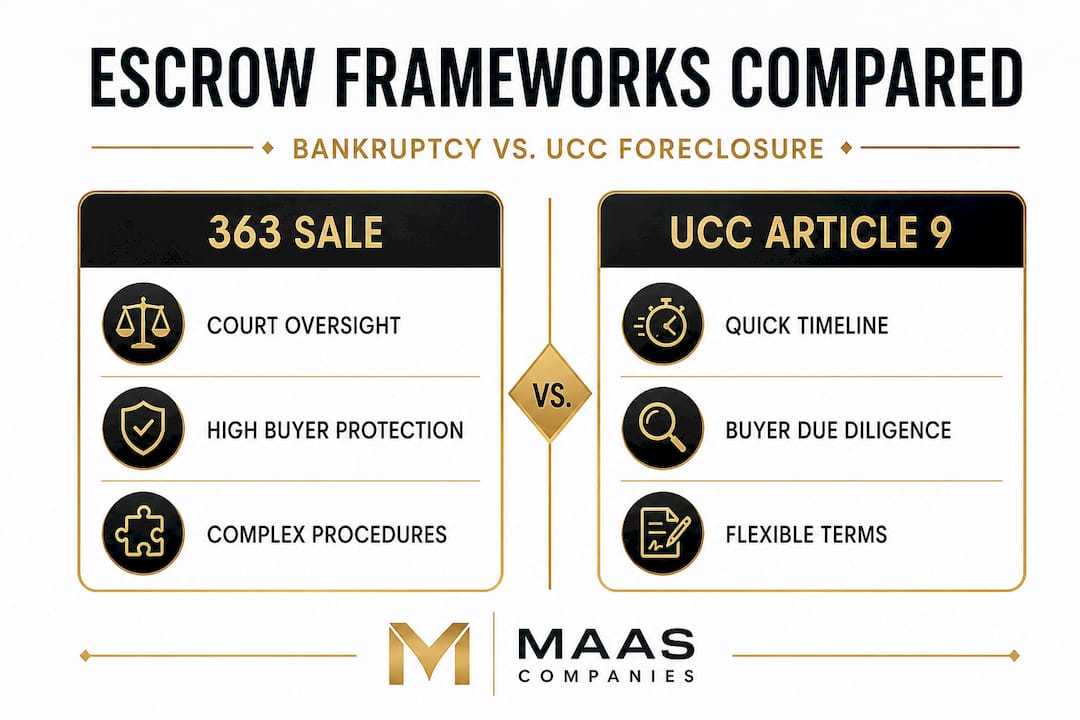

Auction escrow frameworks: Comparison of major processes

Distressed industrial assets are sold through bankruptcy (Section 363), UCC Article 9 foreclosures, or secured party sales, with each method maximizing value via competitive bidding while providing free-and-clear title under different legal conditions. The choice of framework directly affects how escrow is structured, the level of court oversight, and the speed of closing.

| Framework | Legal Authority | Court Oversight | Escrow Deposit Typical Range | Title Status | Timeline |

|---|---|---|---|---|---|

| Section 363 bankruptcy | Bankruptcy Code | Required | 5%–10% of bid | Free and clear | 45–90 days |

| UCC Article 9 foreclosure | Uniform Commercial Code | None required | Varies, often 10% | Subject to senior liens | 30–60 days |

| Secured party sale | State commercial law | None required | Negotiated | Subject to creditor claims | 30–75 days |

| Government surplus auction | Federal/state statute | Administrative review | Fixed percentage or flat fee | Clear by statute | 30–90 days |

Section 363 sales carry the most procedural complexity but offer the strongest buyer protections. The court’s involvement means that title disputes, lien challenges, and competing interests are resolved before closing, giving buyers a level of certainty that UCC foreclosures cannot always match.

UCC Article 9 foreclosures move faster but require buyers to conduct thorough due diligence independently. The choosing the right auction decision often comes down to how much time a seller has and how clean the asset’s title history is. A secured party sale with a well-drafted escrow agreement can approximate the protections of a 363 sale, but only when experienced legal counsel structures the terms correctly.

Challenges, edge cases, and practical risks in auction escrow

Even experienced private equity professionals encounter complications in auction escrow that erode recovery value or delay closings. Recognizing these risks before they materialize is essential.

Escrow agents ensure neutral holding of funds; in bankruptcy, court-approved procedures govern over standard escrow agreements, meaning parties cannot simply modify terms without judicial authorization.

Common oversights in complex distressed auctions include:

- Deposit forfeiture on bidder default: When a winning bidder fails to close, the deposit is forfeited and the asset may go to backup bidders. However, if no qualified backup bid exists, the seller faces a re-auction with significant carrying costs and time loss.

- Stalking horse breakup fee disputes: Stalking horse bidders negotiate breakup fees of 1% to 3% of the transaction value, held with escrow priority. These arrangements can become contested when other creditors argue the fees reduce estate value. The superpriority status of these fees is frequently litigated in larger Chapter 11 proceedings.

- Credit bidding by secured creditors: Secured creditors have the legal right to bid up to the face value of their debt without submitting a cash deposit. This creates an imbalance when other bidders must post 5% to 10% in escrow while the credit bidder posts nothing, which can suppress competitive participation.

- Escrow agent conflicts of interest: Using a bank with existing relationships to one of the parties as escrow agent introduces risk. Court-appointed or independent escrow agents are strongly preferred in contested proceedings.

- Incomplete bid procedures documentation: When escrow terms are vague about what triggers release or what constitutes a qualifying default, disputes arise that require court intervention to resolve.

| Risk Factor | Likelihood | Impact on Recovery | Mitigation |

|---|---|---|---|

| Bidder default | Moderate | High, delays re-auction | Require backup bids at close |

| Stalking horse dispute | Moderate | Moderate, legal costs | Cap breakup fees at 1.5% |

| Credit bid suppression | Common | Moderate, fewer bidders | Structure overbid minimums |

| Escrow agent conflict | Low | High if litigated | Use independent third party |

| Documentation gaps | Common | High, court delays | Pre-approve all escrow terms |

Pro Tip: Always confirm that the proposed escrow agent is court-approved and has no material relationship with any party. In contested bankruptcy auctions, even the appearance of bias can trigger objections that delay closing by weeks.

Firms responsible for planning industrial closures should address escrow terms during the pre-marketing phase. Similarly, thorough equipment auction preparation reduces the risk of late-stage surprises that force escrow modifications after bidders are already qualified.

Maximizing value and certainty with auction escrow: Best practices

Understanding the mechanics and risks of auction escrow creates a foundation for using it as a strategic tool rather than just a compliance requirement. Private equity firms that use auction escrow effectively in distressed deals prefer Section 363 for free-and-clear assets but must manage compressed timelines of 45 to 90 days to maximize recovery.

Here is a practical framework for optimizing auction escrow in distressed industrial asset transactions:

- Begin escrow planning at asset assessment: Identify the appropriate legal framework and escrow structure during the initial asset evaluation, not after the marketing campaign has launched. Early decisions about deposit thresholds and holdback terms directly influence bidder interest.

- Qualify bidders rigorously before the auction date: Require financial statements, bank letters, and signed confidentiality agreements as part of the qualification process. Escrow requirements should be communicated clearly in the bidder package so there are no surprises at the auction.

- Set deposit levels that filter without discouraging: A 10% deposit requirement filters unqualified bidders effectively, but setting it too high without justification can reduce participation, especially for large industrial plant sales where even 5% represents substantial capital.

- Structure holdbacks around known risk factors: If the asset has environmental liabilities, known equipment conditions issues, or pending regulatory matters, the holdback percentage and duration should reflect these specific risks rather than defaulting to a generic 10%.

- Establish clear dispute resolution protocols: Include a binding arbitration clause in the escrow agreement for non-bankruptcy sales. For 363 sales, identify the court’s role in resolving escrow disputes upfront and communicate this to all bidders.

- Communicate closing timelines precisely: Bidders and their financing sources need to know exactly when escrow will close and funds will be released. Surprises in the final days create unnecessary friction and can threaten closings.

- Confirm escrow agent credentials early: Select an agent with specific experience in distressed transactions. The escrow agent’s familiarity with bankruptcy court procedures, UCC requirements, and creditor priority issues can prevent procedural errors that delay closing.

Pro Tip: When working within a 45 to 90-day 363 sale timeline, speed up asset disposition by pre-clearing title issues, environmental reports, and lien searches before the auction. Every day saved in due diligence is a day gained toward a faster, higher-confidence closing.

Auction escrow: What most decision-makers miss

Most articles on auction escrow focus on the mechanics. The deeper challenge is strategic, and it involves trade-offs that even experienced private equity professionals frequently underestimate.

The first blind spot is the speed versus recovery trade-off. Auctions ensure speed and certainty but can produce lower recovery compared to a negotiated M&A process. Escrow makes the speed benefit possible by securing commitments quickly, but it does not automatically produce the highest price. When the timeline is compressed, fewer bidders qualify, fewer financing sources can commit, and the competitive tension that drives price discovery weakens.

The second blind spot is the stalking horse risk. A stalking horse bidder provides a floor for the auction, but if the stalking horse negotiates too many protections, potential competing bidders may conclude the deal is effectively pre-sold and decline to participate. The result is a sale at the floor price, with the seller having paid breakup fees for a competition that never materialized.

The third blind spot is the most important: in a bankruptcy auction, the court controls the escrow mechanics, not the parties. Private equity buyers accustomed to negotiating escrow terms in private M&A transactions sometimes attempt to import those expectations into a 363 sale, only to find that court-approved bid procedures override their assumptions. Building a recovery strategy around auction strategies for recovery requires understanding that flexibility decreases as court oversight increases.

The firms that generate the best outcomes treat escrow as a signal of deal quality. When escrow is properly structured, qualified, and transparently communicated, it attracts serious bidders and reduces friction at every stage. That is where the real value lies, not just in protecting against default, but in creating conditions where competitive tension can develop without uncertainty undermining participation.

Explore efficient industrial auctions with trusted escrow solutions

Applying these escrow principles to real transactions requires experience, legal coordination, and a marketing infrastructure capable of reaching qualified buyers on compressed timelines.

Maas Companies Inc. manages industrial plant and equipment auctions where proper escrow structuring is built into the marketing and bidding process from the start. Whether you are evaluating an active biodiesel plant auction or looking to sell industrial assets under a distressed timeline, our team brings the operational and legal coordination that protects your recovery. Explore our full range of auction and escrow services to see how structured, professionally managed auctions consistently produce better outcomes than uncoordinated liquidation efforts.

Frequently asked questions

What assets typically require auction escrow?

Auction escrow is commonly used for distressed industrial equipment, manufacturing plants, and commercial real estate sold through bankruptcy or foreclosure auctions, where court oversight or creditor interests require a neutral holding structure.

How much is the typical auction escrow deposit?

Deposits typically range from 5% to 10% of the bid amount in Section 363 sales, though the exact percentage depends on asset value, auction type, and the seller’s risk tolerance.

Who controls the escrow funds during an auction?

A neutral escrow agent holds and manages the funds throughout the auction and closing process, with court-approved agents required in bankruptcy proceedings to ensure impartiality.

What happens if a winning bidder defaults after an auction?

The escrow deposit is forfeited on default, and the asset may be offered to qualified backup bidders or placed in a re-auction, depending on the terms established in the bid procedures.

Can secured creditors bid without a cash deposit in auction escrow?

Secured creditors may submit credit bids up to the value of their debt claim without posting a cash deposit, which is a standard right in bankruptcy and foreclosure sales under applicable law.

Recommended

- Commercial Real Estate Auctions Speed Up Sales | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- Plan Better Industrial Closures With Expert Auction Help | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- Reverse Auctions have a Bright Future