Blog

Liquidate Surplus Inventory Process: A 2026 Guide

TL;DR:

- Excess inventory ties up capital, increases costs, and reduces operational flexibility if not managed properly. Implementing a disciplined liquidation process that includes accurate assessment, strategic channel selection, and precise execution can convert surplus stock into recoverable cash. Proper documentation, timely decisions, and post-sale analysis are essential for maximizing recovery and reducing future surplus risk.

Excess inventory is not a neutral condition. Every pallet of unsold product sitting in your warehouse represents tied-up capital, accumulating carrying costs, and reduced operational flexibility. When businesses fail to act on surplus stock with a structured plan, the financial drag compounds quickly. The liquidate surplus inventory process, when executed with discipline and the right channel strategy, converts that dead weight into recoverable cash. This guide provides a complete operational framework, from initial valuation through post-sale optimization, so decision-makers can act with both speed and precision.

Table of Contents

- Key takeaways

- Inventory assessment and valuation

- Choosing the right liquidation channel

- Executing the liquidation process

- Monitoring results and optimizing future cycles

- What I have learned from real liquidation events

- How Maascompanies supports asset recovery

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Assess before you act | Accurate inventory valuation, including age, condition, and demand, determines which channel and price tier to target. |

| Channel choice drives recovery | Wholesale B2B yields the highest recovery rates; auctions are fastest but return significantly less per unit. |

| Timing is a financial variable | A 60-day disposition clock, with staged markdowns, protects cash flow and prevents value erosion on aging stock. |

| Data hygiene changes outcomes | Complete manifests and verified SKU documentation increase bargaining power and reduce forced bulk discounting. |

| Monitor and adjust post-sale | Tracking sell-through rates and repricing by channel allows continuous improvement across future liquidation cycles. |

Inventory assessment and valuation

Before any surplus inventory liquidation can begin, you need an accurate picture of what you are actually selling. This step is where most businesses lose money, not in the sale itself, but in the preparation. Skipping a rigorous assessment forces reactive pricing and limits your channel options before negotiations even start.

The assessment process should identify three distinct inventory categories:

- Slow-moving stock: Products with low SKU velocity that are still sellable but accumulating carrying costs beyond their contribution margin.

- Seasonal or time-sensitive items: Goods tied to a calendar window where demand will decline sharply if not cleared promptly.

- Obsolete inventory: Products with no realistic demand path forward. Rapid disposition or write-off avoids increasing holding costs and operational overhead without improving recovery.

Once categorized, each group requires a condition verification. Physical counts must match system records. SKUs should be labeled accurately, and condition grades documented with photo evidence where applicable. This documentation is not administrative overhead. It is the foundation of your bargaining position.

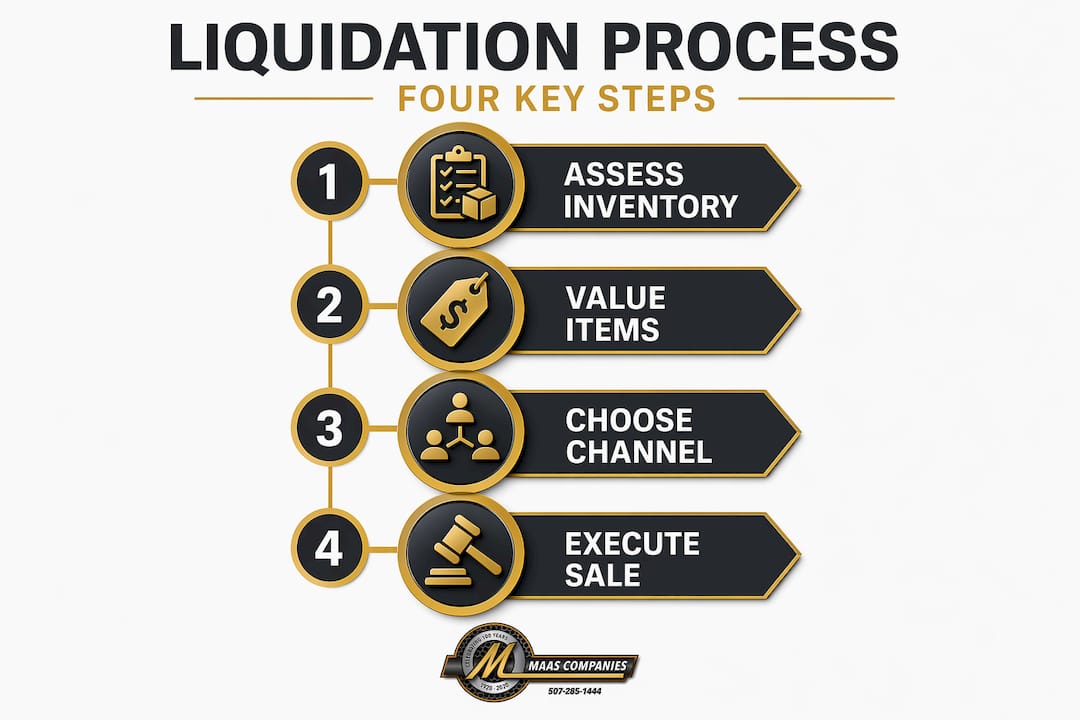

Estimating liquidation value requires honesty about market conditions. The four-step liquidation process covers assessment, value estimation, channel selection, and execution, and it starts with acknowledging that liquidation pricing reflects product age, current demand, and competitive alternatives, not original cost or retail price. A product worth $100 at retail may fetch $30 to $60 through the right channel, or as little as $10 through a bulk buyer if documentation is poor.

Pro Tip: Use inventory aging reports and SKU velocity data from your warehouse management system before contacting any buyers. Buyers will request this data during due diligence, and having it prepared in advance signals operational credibility and reduces negotiation friction.

Choosing the right liquidation channel

Channel selection is the single most consequential decision in the surplus inventory liquidation process. The right channel depends on three variables: how quickly you need the cash, how much recovery value you are willing to accept, and what brand exposure risk you can tolerate.

The recovery rate differences between channels are significant. Recovery rates vary by channel as follows:

| Channel | Recovery Rate | Speed |

|---|---|---|

| B2B wholesale buyers | 40% to 70% of cost | Moderate (weeks) |

| Flash sales | 30% to 60% of cost | Fast (days to weeks) |

| Online marketplaces | 15% to 40% of cost | Variable |

| Auctions | 10% to 30% of cost | Fast (days) |

| Bulk buyers | 5% to 20% of cost | Very fast (days) |

The speed versus recovery tradeoff is the defining tension in every liquidation decision. Auctions move inventory fastest, but they consistently return the lowest per-unit margin. B2B wholesale transactions take longer to negotiate and execute but preserve significantly more recovery value.

Brand risk is a consideration that operations leaders sometimes underweight. Steep discounts in liquidation can damage brand perception, with customers interpreting deep markdowns as a signal of poor product quality rather than a managed clearance. For branded goods or products still sold through active retail channels, this risk must be weighed against recovery urgency.

The best channel match depends on inventory type and business objectives:

- Industrial equipment and plant assets: Auctions and B2B wholesale, where buyers have specific technical needs and appreciate detailed documentation.

- Consumer goods with remaining shelf life: Flash sales or marketplace listings where speed and volume are priorities.

- Branded merchandise: Wholesale to secondary market buyers outside your primary retail footprint reduces brand channel conflict.

Pro Tip: Do not commit all surplus stock to a single channel. Segment your inventory by recovery potential and route high-value, well-documented SKUs to B2B wholesale while reserving lower-grade or mixed lots for auction or bulk disposition. This tiered approach maximizes blended recovery across the full liquidation event.

For a detailed comparison of auction channels and their respective recovery profiles, the industrial auction channel analysis from Maascompanies provides a practical framework grounded in real transaction data.

Executing the liquidation process

Once the inventory is assessed and channels are selected, execution becomes an operational discipline. The difference between a well-run liquidation and a chaotic one is almost always traceable to process consistency at this stage.

A structured execution sequence should follow these steps:

- Receive and sort inventory. All stock designated for liquidation should be physically staged and separated from active inventory. Commingling active and surplus stock creates mis-shipment risk and complicates accounting.

- Verify SKUs and condition grades. Each item must be confirmed against the manifest. Outsourcing inventory operations involves warehouse receipt, SKU verification, labeling, and counts before WMS/ERP integration. Whether you manage this internally or through a third party, the same standards apply.

- Apply staged markdown pricing. Begin pricing at 75% to 85% of MSRP and trigger deeper discounts based on time elapsed and remaining volume. Staged depletion pricing improves gross margin by applying multiple markdown phases rather than a single fire-sale price.

- Activate the 60-day disposition clock. If inventory does not clear through primary channels within 60 days, shift to bulk liquidation to maintain cash flow velocity. This rule enforces discipline and prevents inventory from aging further while you wait for better buyers.

- Execute buyer contracts with clear terms. Every third-party transaction requires documented payout timing, logistics responsibilities, and dispute resolution terms. Poor contract agreements reduce cash flow velocity and leave inventory sitting on your books while disputes are resolved.

- Integrate with your WMS or ERP. Liquidated SKUs must be removed from active inventory records promptly. Delayed updates create phantom stock, complicate reordering decisions, and distort financial reporting.

Pro Tip: Assign a single point of accountability for each liquidation event. When responsibility is distributed across multiple teams without clear ownership, manifest accuracy suffers, communication gaps emerge with buyers, and disposition timelines slip. One person should own the outcome.

The inventory management checklist from ParcelPlanet offers a practical reference for the receiving and verification steps, particularly useful for teams new to structured liquidation workflows.

Monitoring results and optimizing future cycles

Execution does not end when the stock ships. Measuring performance after each liquidation event is what separates organizations that improve their recovery rates over time from those that repeat the same costly patterns.

The metrics that matter most in post-liquidation review include:

- Sell-through rate by channel: What percentage of designated surplus stock was sold within the target timeframe? A low sell-through rate in a given channel signals either a pricing mismatch or poor buyer fit for that inventory type.

- Revenue recovery percentage: Actual cash recovered divided by the cost of goods sold for the liquidated lot. Tracking this over multiple events reveals whether your channel mix and pricing strategy are improving.

- Timeline adherence: Did the disposition clock hold? Delays in execution carry real costs. The longer surplus stock stays in your facility, the higher the carrying costs relative to recovery value.

- Repricing trigger effectiveness: Did staged markdowns move volume at each price tier, or did inventory stall before reaching bulk disposition? This tells you whether your initial pricing was calibrated to market demand.

Accounting accuracy is also non-negotiable at this stage. Under U.S. GAAP rules, once inventory is written down under ASC 330, the write-down cannot be reversed even if market conditions improve. Write-down decisions must align with your financial reporting windows because the accounting treatment is permanent. Operations leaders who coordinate liquidation timing with finance teams avoid costly surprises during quarterly closes.

The learnings from each liquidation cycle feed directly into inventory planning. If a specific product category consistently generates surplus, the root cause lies upstream in purchasing decisions, demand forecasting, or supplier minimums. Documented SOPs reduce execution risk and refine channel choices for speed, cash recovery, and brand protection across future events. Treating each liquidation as a data-generating process, rather than a one-time problem to solve, is how businesses reduce future surplus exposure over time.

For guidance on how inventory review decisions connect to broader financial recovery strategies, the liquidation expert inventory review framework from Maascompanies provides structured decision criteria.

What I have learned from real liquidation events

In my experience working through industrial asset and inventory recovery events, the most consistent mistake I observe is urgency without preparation. Decision-makers face pressure to convert surplus stock into cash quickly, and that pressure leads to skipping assessment steps, accepting the first buyer offer, or routing all inventory to the fastest channel regardless of recovery potential.

The businesses that consistently achieve higher recovery rates are not faster. They are more organized before the sale begins. Clean manifests, verified condition grades, and complete SKU documentation give sellers genuine negotiating leverage. Without that documentation, buyers price in their own uncertainty with steep discounts. Incomplete manifests force discounted bulk channel sales with lower margin recovery. That is not a buyer advantage. That is an avoidable seller loss.

I have also found that most organizations underestimate how much brand risk compounds when liquidation is managed reactively. A controlled B2B wholesale program, even at a slower pace, protects channel relationships and customer perception far better than a public flash sale that signals distress. The choice of how you liquidate communicates something to your market. Treat that communication as intentional, not incidental.

The tools available in 2026, from WMS integrations to specialized marketplace platforms, reduce execution friction considerably. But technology does not substitute for the discipline of following a structured process. The fundamentals of the liquidate surplus inventory process have not changed: assess accurately, choose channels deliberately, execute with documented procedures, and measure every outcome.

— Vector

How Maascompanies supports asset recovery

When the scale or complexity of a liquidation event requires experienced guidance, Maascompanies brings decades of proven results to industrial and commercial asset recovery. From surplus equipment auctions involving complete plant facilities to negotiated sales of specialized industrial assets, Maascompanies manages the full process with an aggressive marketing program and the technical expertise to reach qualified buyers worldwide.

If you are evaluating how to liquidate inventory from a plant closure, restructuring, or operational downsizing, the Maascompanies team provides consultation, valuation support, and tailored disposition programs. Visit the seller services page to explore how Maascompanies can maximize recovery for your specific situation.

FAQ

What are the main steps to liquidate surplus inventory?

The liquidate surplus inventory process follows four core steps: inventory assessment and valuation, liquidation value estimation, channel selection, and execution with post-sale monitoring. Each step builds on the previous one to maximize cash recovery while managing brand and timing risk.

Which liquidation channel offers the highest recovery rate?

B2B wholesale buyers typically offer the highest recovery rates, ranging from 40% to 70% of inventory cost, making them the preferred channel when time permits. Auctions and bulk buyers move inventory faster but return significantly less per unit.

How does ASC 330 affect inventory liquidation decisions?

Under ASC 330, inventory write-downs recorded under U.S. GAAP are permanent and cannot be reversed if market conditions improve later. Finance teams should coordinate liquidation timing with reporting periods to avoid unexpected impacts on quarterly or annual financial statements.

What is the 60-day disposition clock in liquidation planning?

The 60-day disposition clock is a structured timeline rule: if inventory does not sell through primary channels within 60 days, it shifts to bulk liquidation to preserve cash flow velocity and prevent further carrying cost accumulation.

How does poor documentation affect liquidation recovery?

Incomplete manifests and inaccurate SKU records reduce bargaining power during buyer negotiations, forcing sellers into bulk discount channels with lower recovery margins. Accurate documentation before marketing surplus stock directly improves final cash outcomes.

Recommended

- Plant liquidation strategies: maximize recovery in 2026 | Blog | Insights on Asset Liquidation and Auction Trends

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Equipment liquidation explained: maximizing asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- How to Plan Government Asset Sales for Spring 2026 | Blog | Insights on Asset Liquidation and Auction Trends