Blog

What Is Asset Liquidation: A CFO’s Strategic Guide

TL;DR:

- Asset liquidation involves converting non-cash assets into cash through strategic, controlled processes, not just distress sales. It encompasses voluntary and involuntary transfers, with careful valuation premises and legal priorities influencing outcomes. Engaging specialists and planning early significantly improves recovery and minimizes legal and financial risks.

Asset liquidation is widely misunderstood as a last resort or a distressed fire sale. In practice, what is asset liquidation comes down to a precise financial process: converting non-cash assets into cash, whether in the context of voluntary restructuring, planned capital reallocation, or court-ordered insolvency proceedings. For CFOs, asset managers, and lenders, understanding this process is the difference between a controlled recovery and a costly, avoidable loss. This guide covers the asset liquidation definition, the process from identification to realization, critical valuation premises, legal priorities, and strategic applications for maximizing financial recovery.

Table of Contents

- Key takeaways

- What is asset liquidation: types and triggers

- The asset liquidation process from identification to realization

- Valuation premises every CFO must understand

- Legal priorities and fiduciary duties in liquidation

- Applying liquidation strategically to maximize recovery

- My perspective on where professionals lose value

- Maximize recovery with Maascompanies

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Liquidation is not just insolvency | Asset liquidation serves voluntary restructuring, capital reallocation, and planned exits, not only distressed situations. |

| Valuation premise determines recovery | Using FMV instead of OLV or FLV in collateral assessments leads to unrealistic recovery expectations. |

| Creditor waterfall is statutory | Proceeds follow a fixed legal order that directly affects how much each stakeholder class receives. |

| Timing controls outcome | Planned, orderly sales consistently generate higher recoveries than forced auctions under compressed timelines. |

| Expert partners improve results | Engaging specialized asset recovery firms reduces carrying costs, legal risk, and valuation errors. |

What is asset liquidation: types and triggers

The asset liquidation definition begins with a straightforward concept: converting non-cash assets into cash. The complexity lies in the context, timeline, and legal framework that governs that conversion.

Voluntary liquidation

Voluntary liquidation is a deliberate strategic decision made by a company or its owners. It occurs in two primary forms. A Members’ Voluntary Liquidation applies when a solvent company chooses to wind down. A Creditors’ Voluntary Liquidation applies when an insolvent company’s directors and creditors agree to appoint a liquidator without court intervention. In both cases, the company retains meaningful control over timing and sale methods. This control is one of the most significant benefits of asset liquidation done on a voluntary basis, since orderly, planned closures generate substantially higher recoveries than forced proceedings.

Common voluntary liquidation triggers for industrial and manufacturing businesses include:

- Plant closures resulting from technology shifts, geographic consolidation, or end-of-life facility decisions

- Restructuring programs that require divesting non-core assets or entire business units

- Excess inventory disposition after production line changes or product discontinuation

- Capital reallocation where funds tied up in equipment or real estate need to be freed for reinvestment

Involuntary liquidation

Involuntary liquidation is initiated by a court order or creditor action, typically following insolvency. In these scenarios, the liquidator is appointed externally and the company loses control over timing. Market pressure compresses auction timelines, asset protection can deteriorate, and the realized recovery frequently falls well below orderly liquidation values. Pre-insolvency asset sales at undervalue carry additional legal risk, including potential court reversal through clawback actions.

Pro Tip: If your organization is approaching financial difficulty, initiating a voluntary Creditors’ Voluntary Liquidation before a court forces one will almost always protect more value for creditors and reduce your personal liability exposure as a director.

The asset liquidation process from identification to realization

Executing a liquidation of business assets properly requires a disciplined, sequential approach. Skipping or compressing any phase reduces recovery and increases legal exposure.

-

Asset identification and inventory. Begin with a thorough physical and documentary inventory. This includes obvious fixed assets like machinery and real estate, but also overlooked items: tooling, spare parts, intellectual property with transferable value, prepaid contracts, and receivables. Off-site storage locations are frequently missed, leading to discovered assets after sales are finalized.

-

Professional appraisal. Engage a credentialed appraiser before any sale process begins. Liquidation value is almost always below book value, and using book value as a proxy for expected recovery will distort every financial projection that follows. Specify the correct valuation premise for your situation: Fair Market Value, Orderly Liquidation Value, or Forced Liquidation Value.

-

Asset protection and cost management. Before any public marketing or auction timeline is announced, confirm that insurance coverage is adequate, secured storage is in place for portable high-value items, and utilities or environmental controls needed to preserve asset condition are maintained. Carrying costs accumulate daily. Every week a facility sits idle before a sale reduces net recovery.

-

Selection of realization method. Liquidators use multiple methods to realize assets including public auctions, private treaty sales, in-situ sales, and receivables collection. The right method depends on asset type, condition, and market demand. Industrial process equipment, for example, may achieve better returns through a targeted negotiated sale to an industry buyer than through a general auction.

-

Marketing and execution. Aggressive, targeted marketing to relevant industry buyers increases competition for assets and lifts realized prices. This is where specialist firms add measurable value. Broad exposure to qualified buyers, particularly for complex assets like industrial plant equipment, directly correlates with recovery rates.

-

Distribution and documentation. Proceeds are distributed according to the statutory creditor waterfall. Every payment must be documented to demonstrate compliance with fiduciary duties and to protect the liquidator from personal liability.

Pro Tip: Never announce a public auction date before completing your asset inventory and appraisal. Setting an auction timeline first creates artificial urgency that buyers exploit, and it forces you to sell assets before you have fully assessed their value.

Valuation premises every CFO must understand

One of the most consequential decisions in the asset liquidation process is selecting the correct valuation premise. Three premises govern most commercial and insolvency contexts, and using the wrong one in a financial model or loan agreement can create serious problems.

| Premise | Definition | Assumed timeline | Typical recovery vs. FMV |

|---|---|---|---|

| Fair Market Value (FMV) | Price between willing buyer and willing seller, neither compelled | Open, unrestricted | 100% baseline |

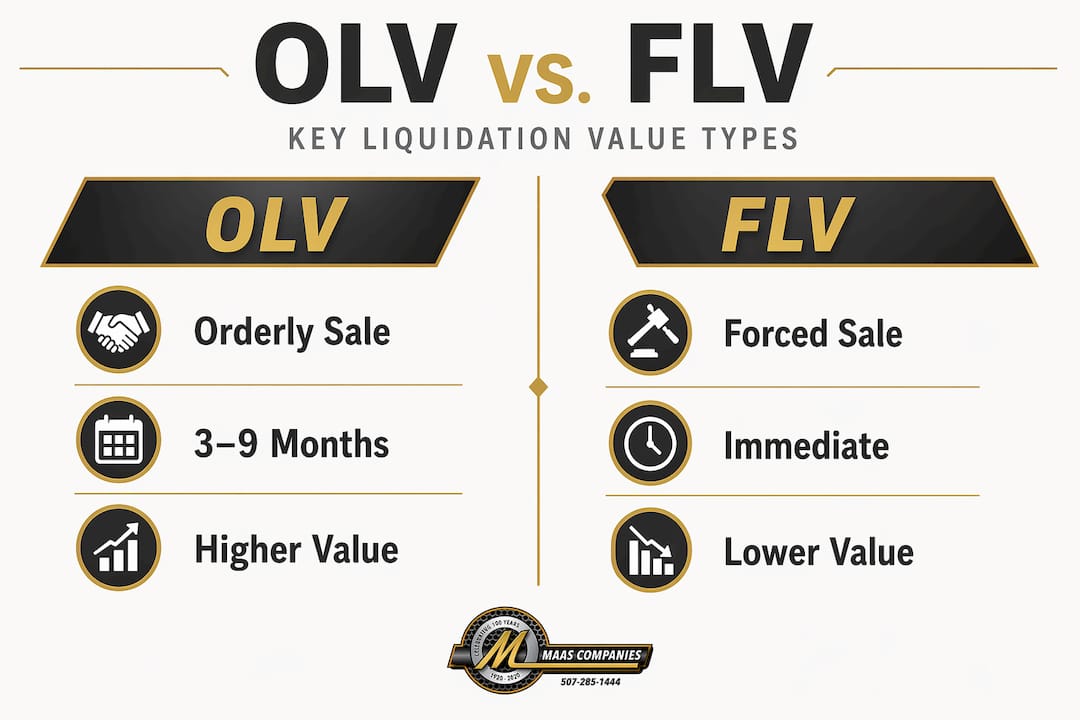

| Orderly Liquidation Value (OLV) | Compelled sale with reasonable marketing period | 3 to 9 months | 60% to 80% |

| Forced Liquidation Value (FLV) | Immediate sale, compressed timeline, public auction conditions | Days to weeks | 40% to 70% |

The practical implications are significant. Asset-based lenders typically rely on OLV to set borrowing bases because it reflects a realistic worst-case recovery over a reasonable marketing period. The SBA requires equipment appraisals on an OLV basis for loans of $500,000 or more for precisely this reason.

Where professionals frequently make errors:

- Using FMV in a collateral calculation for a distressed borrower, which overstates the lender’s position

- Applying FLV to a voluntary liquidation where a 6-month marketing window is fully available, which understates recovery and may lead to premature price concessions

- Failing to revisit the valuation premise as market conditions shift during the liquidation process

The differences between FMV, OLV, and FLV are not theoretical distinctions. They directly determine how much a lender will advance, what a liquidator expects to recover, and whether a creditor’s claim is fully or partially satisfied.

Legal priorities and fiduciary duties in liquidation

Understanding the statutory creditor waterfall is not optional for anyone involved in the liquidation of business assets. The order of payment from liquidation proceeds is fixed by law and controls every distribution decision:

- Liquidation costs and the liquidator’s fees are paid first

- Secured creditors are paid from the proceeds of assets held as collateral

- Preferential creditors, which include certain employee wages and pension contributions, are paid next

- Unsecured creditors receive distributions from remaining funds

- Shareholders receive anything left, which in most insolvencies is nothing

Unsecured creditors frequently receive only a small percentage of their claims after senior obligations are satisfied. This reality must inform how directors and boards communicate with stakeholders before and during a liquidation.

The liquidator’s fiduciary duty runs to the creditor body collectively, not to directors or shareholders. A liquidator who fails to obtain the best reasonably obtainable price for assets faces personal liability for breach of fiduciary duty. This is a material risk, not a procedural formality.

“The fiduciary duty to creditors often surprises corporate insiders unfamiliar with liquidation legal frameworks. Directors accustomed to acting in shareholders’ interests must recognize that, once insolvency is reached, the duty of care shifts entirely to creditors.”

Pre-insolvency transactions carry particular risk. Any asset sale or preferential payment made within statutory review periods can be challenged and reversed by courts if completed at undervalue or to benefit one creditor over others. Documenting the business purpose and fair value basis for every pre-insolvency disposition is non-negotiable.

Applying liquidation strategically to maximize recovery

CFOs and asset managers who understand how to liquidate assets as a strategic tool, rather than treating it purely as a reactive process, consistently achieve better financial outcomes. Several practical principles guide this approach.

-

Assess alternatives before committing. Asset liquidation is one option among several. Sale-leaseback arrangements, debt restructuring, or targeted asset sales may preserve more going-concern value in some scenarios. Liquidation should be selected when it clearly optimizes net recovery relative to the cost of alternatives.

-

Match the sale method to the asset. Commodity equipment such as forklifts or generators often performs well at public auction because the buyer pool is broad. Specialized process equipment, proprietary manufacturing systems, or integrated facility components typically achieve better returns through negotiated sale strategies targeting qualified industry buyers.

-

Control timing deliberately. Controlled, planned plant closures using orderly liquidation approaches generate significantly higher recoveries than rushed forced auctions. Every week added to the marketing timeline in a voluntary liquidation has a measurable positive impact on realized prices, up to the point where carrying costs begin to erode the benefit.

-

Coordinate across disciplines. Effective asset liquidation requires simultaneous input from legal counsel, financial advisors, environmental consultants where applicable, and operations personnel who understand the assets being sold. Siloed decision-making creates gaps in compliance and leaves value on the table.

-

Engage specialist firms early. Firms with deep industrial sector expertise and established buyer networks generate competitive bidding that generic auction platforms cannot replicate. For large industrial plant and equipment dispositions, the fee paid to a specialist firm is consistently recovered through improved recovery rates.

Pro Tip: When planning an equipment auction for industrial plant closures, engage your asset recovery partner at least 90 days before the target sale date. This window allows proper inventory, appraisal, marketing, and buyer qualification to occur without artificial time pressure.

My perspective on where professionals lose value

I’ve worked alongside CFOs and special asset managers on enough industrial liquidation projects to see the same mistakes repeated. The most costly one is treating liquidation as something you do when you’ve run out of options, rather than something you plan for when you still have choices.

When an organization waits until creditors are at the door to begin asset identification, appraisal, and marketing, it eliminates most of the timing advantage that voluntary liquidation provides. The difference between a 6-month orderly sale and a 30-day forced auction can represent a 20 to 30 percentage point difference in recovery. On a $5 million asset base, that is $1 million to $1.5 million left behind.

I’ve also seen professionals use the wrong valuation premise repeatedly, particularly applying FMV in situations where OLV was the correct standard for lender reporting. This doesn’t just create a reporting problem. It sets false expectations for creditors and boards, and it makes the eventual realized recovery look like a failure when it was actually consistent with proper standards.

The fiduciary point deserves emphasis. Directors who have not previously been through an insolvency often believe their obligations remain to shareholders. They don’t. Once insolvency is evident, every decision must be made in creditors’ interests. Getting this wrong is not just a financial risk. It is a personal legal risk for the individuals involved.

Partnering with specialists who understand valuation, legal compliance, and industrial asset markets eliminates most of these failure modes before they materialize.

— Vector

Maximize recovery with Maascompanies

When asset liquidation projects involve industrial plants, specialized manufacturing equipment, or complex multi-asset dispositions, the margin between a competent outcome and an exceptional one comes down to marketing reach, industry expertise, and process discipline.

Maascompanies brings decades of experience in successfully marketing industrial plants, equipment, real estate, and commercial properties across international markets. From complex biodiesel plant liquidations to targeted orderly negotiated sales for specialized process equipment, Maascompanies structures every project around one objective: maximizing net recovery for clients through aggressive, targeted marketing to qualified buyers. If you are managing a plant closure, restructuring, or equipment disposition, explore your liquidation sale options with Maascompanies to understand what a professionally managed process can deliver for your recovery targets.

FAQ

What is asset liquidation in simple terms?

Asset liquidation is the process of converting non-cash business assets into cash, either through sale at auction, negotiated transaction, or other realization methods. It applies to both voluntary strategic dispositions and involuntary insolvency proceedings.

What are the main types of asset liquidation?

The two primary types are voluntary liquidation, where a company controls the timing and sale process, and involuntary liquidation, which is court-ordered and typically results in lower recoveries due to compressed timelines and market pressure.

Why do businesses liquidate assets?

Businesses liquidate assets to free capital tied up in non-core or surplus equipment, to satisfy creditor obligations during insolvency, or to execute planned exits, plant closures, and restructuring programs. The benefits of asset liquidation depend heavily on how early and deliberately the process is managed.

What is the difference between OLV and FLV?

Orderly Liquidation Value assumes a compelled sale with a reasonable marketing period of 3 to 9 months and typically recovers 60% to 80% of Fair Market Value. Forced Liquidation Value assumes an immediate sale under auction conditions and typically recovers only 40% to 70% of Fair Market Value.

Why use asset liquidation services from a specialist firm?

Specialist firms provide professional appraisal, targeted buyer marketing, legal compliance support, and sale method selection. These capabilities directly increase realized recovery rates, reduce carrying costs, and protect the liquidator and directors from fiduciary and legal risks.

Recommended

- Equipment liquidation explained: maximizing asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Liquidation sales explained: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Maximize Budget Flexibility with Year-End Asset Sales | Blog | Insights on Asset Liquidation and Auction Trends

- How to Plan Government Asset Sales for Spring 2026 | Blog | Insights on Asset Liquidation and Auction Trends