Blog

Maximize asset recovery: how auctions drive results

TL;DR:

- Modern auctions, especially court-supervised or online platforms, often outperform private sales in speed, certainty, and fair market value for distressed industrial assets. They leverage designs like Section 363 bankruptcy sales and credit bidding to maximize recovery while reducing holding costs and operational risks. Choosing the appropriate auction model and strategy, including lotting and bidding protections, is crucial for optimizing asset value in distressed manufacturing environments.

Private equity firms and corporate decision-makers managing distressed manufacturing assets often treat auctions as a fallback option when nothing else works. That assumption costs money. Well-structured auctions, particularly those using court-supervised processes or expertly marketed online platforms, regularly produce recovery rates that match or exceed private sale outcomes, while also delivering speed and certainty that drawn-out negotiations simply cannot match. This guide explains how modern auction strategies work, what protections exist for participants, and how your team can use these tools to realize full value from distressed industrial assets.

Table of Contents

- Why auctions are central to modern asset recovery

- The mechanics of asset auctions: timelines, protections, and bidding strategies

- Auction strategy: credit bidding and maximizing lender recoveries

- Choosing the right auction model for manufacturing and industrial assets

- The surprising truth about auctions in distressed asset recovery

- Next steps: connect with trusted auction specialists

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Auctions deliver speed and certainty | Distressed asset auctions provide fast timelines and transparent, court-supervised outcomes. |

| Credit bidding maximizes recoveries | Secured lenders can bid their debt and often achieve higher asset recovery through strategic auction participation. |

| Stalking horse bids protect early movers | Initial bidders gain valuable protections and help establish competitive price floors for assets. |

| Auction model selection matters | Choosing the right auction type and marketing strategy impacts recovery value and sale speed. |

| Private sales vs. auctions | Private sales may outpace auctions only when time allows and ideal buyers are engaged early. |

Why auctions are central to modern asset recovery

The persistent myth that auctions only attract bottom-feeders looking for steep discounts has led many private equity firms to delay or avoid the auction route entirely. That delay frequently destroys the very value they were trying to protect. Auctions create a controlled, time-bound environment where competition among qualified buyers drives pricing upward, not downward.

Three core characteristics make auctions strategically sound for distressed asset recovery:

- Speed: A formal auction process compresses the sale timeline significantly, reducing carrying costs such as insurance, maintenance, security, and financing that accumulate during prolonged liquidation periods.

- Certainty: Auction contracts are typically non-contingent, meaning buyers commit without extended due diligence periods or financing escape clauses that routinely kill private deals.

- Transparency: Court-supervised or publicly marketed auctions demonstrate that the seller achieved fair market value, which is critical for lenders, trustees, and other stakeholders who must account for proceeds.

Auction models vary, and matching the right model to your asset class matters enormously. Live on-site auctions work well for heavy equipment where buyers want physical inspection. Online timed auctions expand the buyer pool globally. Sealed-bid formats favor situations where confidentiality is important or assets are unique. Hybrid models, combining live and online participation, now dominate many large industrial sales.

One of the most powerful auction mechanisms available to distressed asset managers is the Section 363 bankruptcy sale. These plant liquidation strategies deliver “free and clear” title transfer, meaning buyers take assets without successor liability, environmental claims, or pre-existing liens following through to them. Section 363 auctions use stalking horse bids to establish a floor price, typically complete within 45 to 90 days, and include break-up fee protections of 1 to 3% for the initial bidder, making them attractive for both buyers and sellers.

“The free-and-clear title provision in Section 363 sales removes the single biggest barrier to buyer participation in distressed asset markets: successor liability risk. When buyers know exactly what they are acquiring, competitive tension increases and so does the final price.”

Auctions are not a last resort. They are a precise tool. Used at the right moment, with the right marketing, they outperform nearly every other disposition method when time and certainty are the governing constraints.

The mechanics of asset auctions: timelines, protections, and bidding strategies

Understanding how auctions actually unfold helps decision-makers plan their recovery strategy with confidence. The operational sequence is more structured than many realize, and each step contains protections that reduce risk for both buyers and sellers.

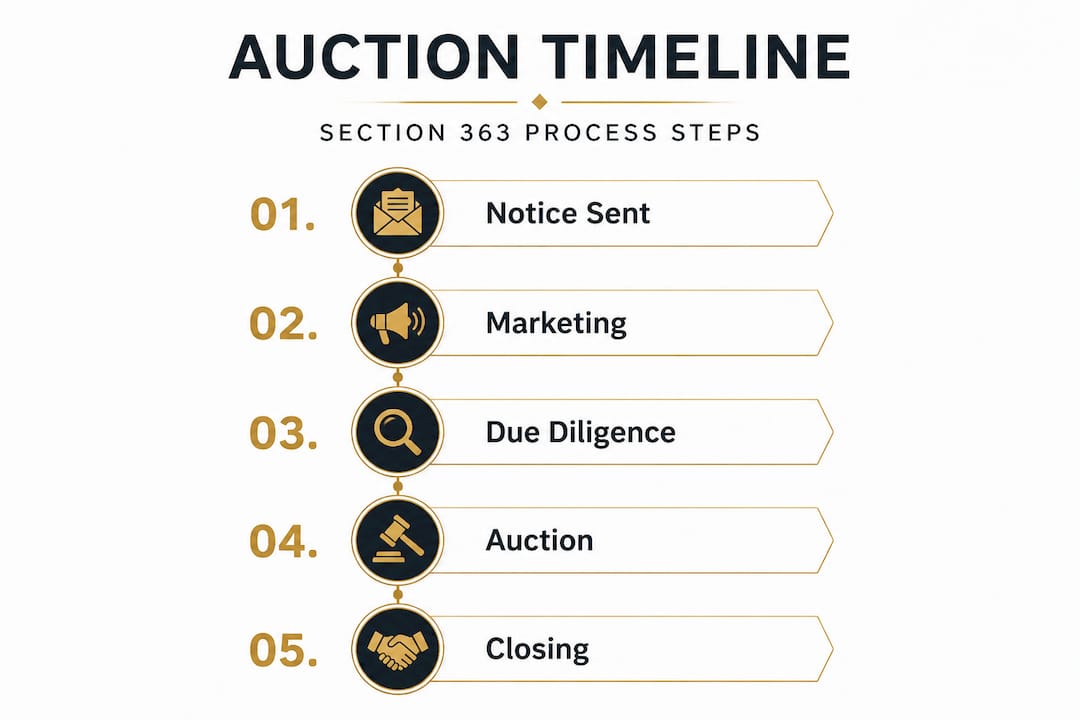

The standard auction process for distressed industrial assets follows this sequence:

- Notice and marketing period: The seller, often guided by an experienced auction firm, publishes notice of the sale and begins an aggressive marketing campaign targeting qualified buyers across relevant industries and geographies.

- Due diligence window: Potential buyers are given access to asset lists, condition reports, facility access for inspection, and financial disclosures. This period typically runs two to four weeks for industrial assets.

- Stalking horse bid submission (where applicable): A pre-qualified buyer submits the opening bid, establishing a floor price and setting the terms of competition. This step is most common in Section 363 bankruptcy sales.

- Active bidding: Qualified bidders compete, either in a live room, online, or both, with bid increments established in advance. Competition drives the price above the floor.

- Sale approval: In court-supervised proceedings, the bankruptcy judge approves the winning bid. Outside of bankruptcy, seller confirmation closes this phase.

- Closing: Funds transfer, titles clear, and the buyer takes possession according to the agreed timeline.

How auctions accelerate disposition matters greatly when carrying costs are running at $50,000 to $200,000 per month on a large industrial facility. Every week of delay represents real value erosion.

| Auction phase | Typical duration | Key action |

|---|---|---|

| Notice and marketing | 2 to 4 weeks | Targeted outreach, catalog preparation |

| Due diligence | 2 to 3 weeks | Buyer qualification, site access |

| Stalking horse / pre-bid | 1 to 2 weeks | Floor price established |

| Active bidding | 1 to 3 days | Competitive bidding process |

| Approval and closing | 1 to 3 weeks | Title transfer, funds settlement |

Section 363 timelines of 45 to 90 days total from notice to closing compare favorably to private sale processes that routinely stretch six months to a year, during which assets depreciate, facilities incur costs, and market conditions can shift unfavorably.

The auction lot strategies your team uses also have a significant impact on realized value. Breaking assets into well-structured lots increases competition by allowing smaller buyers to participate and prevents a single large buyer from acquiring everything at a bulk discount. Experienced auction firms manage lotting as a science, grouping complementary equipment to attract specific buyer categories while creating enough lots to generate volume competition.

Pro Tip: Require bidders to submit proof of funds or a financial qualification letter before granting full due diligence access. This filters out tire-kickers and ensures your bidder pool is composed of buyers who can actually close.

Auction strategy: credit bidding and maximizing lender recoveries

For secured lenders and private equity firms holding debt positions in distressed companies, credit bidding is one of the most powerful and underutilized tools in asset recovery. Understanding how to deploy it correctly can mean the difference between a full recovery and a substantial loss.

What is credit bidding? Under Section 363(k) of the U.S. Bankruptcy Code, a secured creditor has the right to bid its allowed secured claim rather than paying cash. In practical terms, a lender owed $20 million can bid up to $20 million toward purchasing the assets without transferring any new cash, effectively offsetting its debt against the purchase price.

Credit bidding allows secured lenders to maximize recoveries in 363 auctions, and the strategy becomes particularly powerful when a firm buys distressed debt at a significant discount and then bids the full face value at auction. Consider this scenario: a private equity firm acquires a secured claim of $15 million for $8 million, representing a 47% discount. At auction, that firm then credit bids the full $15 million face value. If the assets are worth $12 million, the firm has effectively acquired them for $8 million in actual cash outlay while outbidding cash bidders who would need to put up $12 million in real capital.

Comparing credit bidding and cash bidding:

| Factor | Credit bidding | Cash bidding |

|---|---|---|

| Capital required | Debt face value (reduced by discount) | Full cash outlay |

| Risk profile | Limited to debt acquisition cost | Full purchase price at risk |

| Competitive position | Can bid to full debt face value | Constrained by available capital |

| Strategic use | Lenders, distressed debt buyers | Strategic acquirers, trade buyers |

Common tactics for private equity participants in auction settings include:

- Debt acquisition: Purchase secured claims from fatigued or motivated lenders at discount, then exercise credit bid rights.

- Stalking horse positioning: Submit the opening bid with negotiated break-up fee protection, ensuring either you win the asset or receive fee compensation if outbid.

- Coalition building: Partner with other creditors to form a credit bid coalition with a larger combined claim, increasing bidding power.

- Information leverage: Use the extended due diligence period available to stalking horse bidders to complete thorough asset assessment before competitive bidders have full access.

The pitfalls are equally important to recognize. Courts have occasionally challenged or limited credit bid rights where the creditor’s claim is disputed. Moving quickly to resolve any claim objections before the auction notice period is critical. Additionally, auction absentee bidding arrangements can be useful for creditors who cannot attend the live event, but these require precise pre-set bid limits and trusted representatives.

Pro Tip: Always conduct an independent asset valuation before setting your credit bid ceiling. Overestimating asset value and winning at an inflated price is a recoverable error only if you intend to operate the business, not if your strategy requires resale.

Choosing the right auction model for manufacturing and industrial assets

Not every auction model produces the same results for every asset type or situation. Private equity firms and corporate decision-makers need a practical framework for selecting the model that aligns with their assets, their timeline, and their target buyer base.

Auction model options and their best-fit scenarios:

- Live on-site auction: Best for heavy manufacturing equipment, large machinery, and facilities where physical inspection drives buyer confidence. The atmosphere of competitive live bidding often produces strong results for tangible, moveable assets.

- Online timed auction: Ideal for surplus equipment, smaller lots, and assets with a national or international buyer base. Online formats eliminate geographic barriers and can run for days, giving buyers time to inspect remotely via detailed catalogs and video walkthroughs.

- Hybrid auction: Combines live on-site participation with simultaneous online bidding. This model has become the industry standard for large industrial plant sales because it maximizes buyer participation without requiring everyone to travel.

- Sealed-bid auction: Best suited for unique assets, sensitive transactions, or situations where all buyers should submit their best offer simultaneously. Less common for manufacturing equipment but appropriate for certain real estate or portfolio sales.

Time is the most important variable in this decision. Stalking horse structures provide a due diligence head start for the initial bidder but carry a risk of limited competition if the marketing period is too short. If you have more than 90 days available and believe the private market can yield a premium price, a structured private sale may outperform auction results. When urgency is the governing factor, a well-marketed auction almost always delivers better outcomes than a rushed private negotiation.

Key considerations when selecting your auction model include:

- Asset value and complexity: Higher-value, complex assets benefit from longer marketing periods and hybrid formats.

- Market demand: Strong secondary markets for the specific equipment type support aggressive timelines. Niche or specialized equipment may require longer exposure to find qualified buyers.

- Buyer geography: International buyer bases require online or hybrid formats with translated marketing materials and international payment capabilities.

- Lotting strategy: Detailed pre-sale lotting, with clear photographs, serial numbers, and condition disclosures, increases participation and reduces buyer hesitation.

Common pitfalls to avoid include under-marketing the sale, which shrinks the buyer pool and suppresses competitive tension; poor lotting that bundles high-value items with low-value items; and ignoring international buyers who often pay premiums for specific categories of U.S. manufacturing equipment. Plant liquidation frameworks that address all of these variables systematically produce consistently stronger recovery rates.

The surprising truth about auctions in distressed asset recovery

The conventional wisdom in private equity and special asset management circles holds that patience yields higher recovery. Wait for the right buyer. Avoid the stigma of auction. Protect the optics. That approach, repeated across thousands of distressed situations, has quietly destroyed more value than it has protected.

The data and experience tell a different story. Post-2020, the dynamics of industrial asset markets shifted fundamentally. Supply chain disruptions, manufacturing reshoring, and equipment shortages created a condition where qualified buyers were actively searching for available assets rather than waiting to be approached. Auctions, especially those with robust digital marketing and global reach, began capturing premiums that private sales had been expected to generate but frequently did not.

The maximizing asset recovery equation is not simply about price. It is about net proceeds after carrying costs, professional fees, and time-value of capital. A private sale that closes at 5% above auction estimate but takes eight additional months to complete often delivers a lower net recovery once carrying costs, lender interest, and opportunity cost are factored in. When you do the math on a facility running $100,000 per month in carrying costs, those eight months represent $800,000 in erosion. That figure exceeds the premium in nearly every scenario.

The stalking horse structure is frequently misread as a sign of weakness, a seller settling for the first offer. Practitioners know the opposite is true. A well-negotiated stalking horse bid with appropriate break-up fee protection actually creates competitive urgency. It signals to the market that a sale is happening, that a floor exists, and that any buyer who wants the asset must move decisively. That urgency generates the very competition that drives prices up, not down.

Decision-makers who have managed distressed industrial assets through multiple market cycles consistently report one lesson: the auction process, when executed by experienced specialists with deep industry networks and aggressive marketing programs, outperforms passive sales approaches more reliably than most internal financial models predict.

Next steps: connect with trusted auction specialists

Translating auction strategy into actual recovery requires experienced execution, not just theoretical knowledge. Maas Companies Inc. brings decades of international experience in selling industrial equipment and managing complex asset liquidation programs across manufacturing, processing, and commercial property sectors.

Whether your situation involves a single surplus equipment lot or a complete plant liquidation, the right strategy starts with a clear understanding of your assets, your timeline, and your target buyer market. The Maas services portfolio covers the full spectrum of auction and marketing solutions, from online timed sales to large-scale hybrid auctions with global reach. You can also review an active example of this expertise in practice through current auction projects currently being marketed. Connect with our team to discuss your specific recovery objectives and begin developing a plan that maximizes proceeds from your distressed assets.

Frequently asked questions

What are the typical timelines for a Section 363 auction?

Section 363 bankruptcy auctions usually take 45 to 90 days from notice to closing, enabling a fast, court-supervised sale with clear title transfer.

How does credit bidding work in asset recovery auctions?

Credit bidding lets secured lenders bid the full amount of their allowed claim rather than cash, often enabling recovery at full debt face value when the debt was acquired at a discount.

When should private sales be preferred over auctions?

If you have more than 90 days available and the market indicates a premium buyer exists, private sales may outperform auction results, but carrying costs must be factored into any net recovery comparison.

What are stalking horse bids and why are they important?

A stalking horse bid establishes the minimum acceptable price and creates competitive urgency in the auction, ensuring other buyers must beat a known floor rather than speculating on seller expectations.

What protections exist for initial bidders in auctions?

Break-up fees ranging from 1 to 3% of the purchase price protect stalking horse bidders if a competing bid wins, compensating them for the due diligence and commitment costs they incurred.

Recommended

- Auction strategies for small businesses: Maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Why companies auction machinery: maximize asset recovery | Blog | Insights on Asset Liquidation and Auction Trends

- Maximize Asset Recovery: Top Real Estate Liquidation Methods | Blog | Insights on Asset Liquidation and Auction Trends

- How Auctions Help Speed Up Industrial Asset Disposition | Blog | Insights on Asset Liquidation and Auction Trends

- How to price used industrial equipment for fair value – Blast Trader